California Capital Gains Tax Calculator

Use this California capital gains tax calculator to estimate potential tax on a property sale, including sale price, purchase price, adjusted basis, selling expenses, holding period, filing status, and possible 1031 exchange deferral. This tool provides an estimate for planning purposes only and should be reviewed with a CPA or tax advisor.

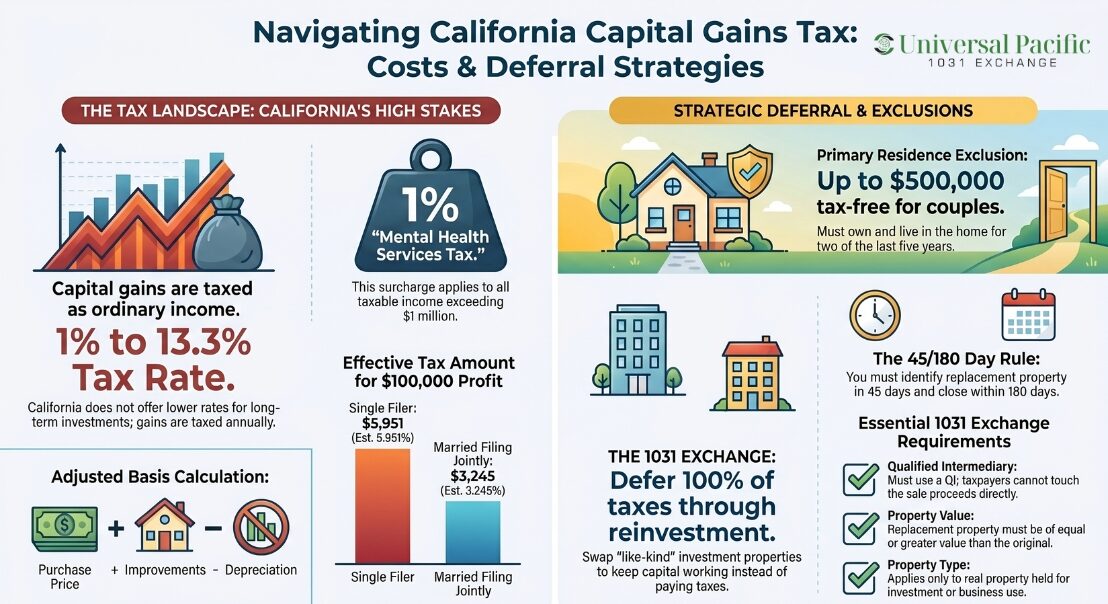

California taxes capital gains at the same rates as ordinary income, with a top marginal rate of 13.3%. Federal long-term capital gains are generally taxed at 0%, 15%, or 20% depending on taxable income and filing status. Real estate investors who held depreciable property may also owe depreciation recapture and, in some cases, the 3.8% Net Investment Income Tax. A properly structured 1031 exchange may allow federal capital gains tax and depreciation recapture to be deferred when the proceeds are reinvested into like-kind replacement property within the IRS deadlines.

Estimate California Capital Gains Tax on a Property Sale

This calculator helps estimate potential California and federal capital gains tax on real estate, investment property, commercial property, or a qualifying home sale. Enter your sale price, purchase price, selling expenses, improvements, depreciation, filing status, and estimated taxable income to see a planning estimate. Results are estimates only and should be reviewed with a CPA or tax advisor.

Estimate potential California and federal capital gains tax on a property sale. Results are estimates only and should be reviewed with a CPA or tax advisor.

This calculator is for educational and planning purposes only. It does not collect, store, or send any data — calculations run entirely in your browser. Federal and California tax rules change over time. Results are estimates and should not be relied on as legal, tax, or financial advice. Confirm any tax position with a CPA or tax advisor before reporting a sale.

How This California Capital Gains Tax Calculator Works

The calculator estimates capital gains tax on a property sale using the inputs you provide:

- It subtracts selling expenses from the sale price to estimate net sale price.

- It estimates adjusted basis using original purchase price, capital improvements, and depreciation taken.

- It calculates estimated capital gain from net sale price minus adjusted basis, reduced by capital losses if entered.

- It applies the Section 121 exclusion only when the property type is marked as primary residence (with optional nonqualified-use allocation under Section 121(b)(5)).

- It estimates California tax because California generally taxes capital gains as ordinary income, with an additional 1% Mental Health Services Tax above $1 million of total income.

- It estimates federal capital gains tax (long-term rates 0%, 15%, or 20% depending on income and filing status), depreciation-related tax impact (up to 25% on the unrecaptured Section 1250 gain portion), and NIIT (3.8% on net investment income above the IRS threshold).

- It shows after-tax proceeds and a conditional 1031 exchange deferral note for investment or business-use real estate.

- Results are estimates for planning purposes only and should be reviewed with a CPA or tax advisor.

Our expert Qualified Intermediary at Universal Pacific 1031 Exchange is always available to help you defer capital gains tax through a properly structured 1031 exchange. We’ve facilitated thousands of successful tax-deferred exchanges in over 35 years, and we have the required experience to guide you through the 1031 exchange process with ease. Book a free consultation with us now to begin your exchange!

This comprehensive guide covers the meaning of capital gains tax, the California capital gains tax rates, and how Universal Pacific 1031 Exchange can help you defer capital gains tax through a successful 1031 exchange.

How Does California Tax Capital Gains on Real Estate?

Capital gains tax refers to the tax you pay on the profit you earn when you sell an asset. It applies to various assets, including real estate, stocks, bonds, and other kinds of investments. In most cases, this also applies to appreciated assets, where the value has increased over time, even if those gains were previously unrealized gains before the sale. In real estate, you calculate capital gain as the difference between the selling price of a property and the adjusted basis of that property.

The adjusted basis is calculated as the original purchase price plus improvements minus depreciation. The calculation of capital gains taxes depends on how long the property was held, and the holding period starts counting from the day you acquired the property to the day you sold it.

Based on the holding period, there are two types of capital gains: short-term capital gains and long-term gains. Short-term capital gains apply to assets held for less than a year before they are sold. Short-term gains are taxed at the seller’s ordinary income tax rate.

On the other hand, long-term capital gains apply to properties held for more than a year before being sold. Long-term capital gain tax rates are usually lower than short-term tax rates at the federal level under federal law, but are taxed at the same rates as short-term capital gains in California. This means your gains are effectively treated as ordinary income annually, regardless of how long the asset was held.

For additional information on capital gains taxes, reach out to Finance Strategists, who will connect you to an expert in the matter and answer any inquiries you might have.

California Capital Gains Tax Rates Used in This Calculator

According to the Franchise Tax Board of the State of California (FTB), there is no difference between short and long-term capital gains taxes. Your capital gains in California are subject to the same California regular state income tax rates, depending on your adjusted gross income and applicable income thresholds. This tax structure can push taxpayers into a higher or lower tax bracket depending on total earnings for the year. This basically ranges from 1% to 12.3% for most taxpayers and up to 13.3% for high-income earners, including the 1% Mental Health Services Tax on income above $1 million.

California significantly differs from the federal capital gains tax rules in certain ways. For instance, as previously mentioned, all capital gains are taxed as ordinary income. Additionally, there are no reduced rates for long-term investments, and the same tax brackets apply to wages, salaries, and business income.

As specified by the FTB, the California capital gains tax rates for different income brackets are as follows:

- 1% tax for taxable income of $0 to $10,099 for single filers, and $0 to $20,198 for married filing jointly.

- 2% tax for taxable income of $10,100 to $23,942 for single filers, and $20,199 to $47,884 for married filing jointly.

- 4% tax for taxable income of $23,943 to $37,788 for single filers, and $47,885 to $75,576 for married filing jointly.

- 6% tax for taxable income of $37,789 to $52,455 for single filers, and $75,577 to $104,910 for married filing jointly.

- 8% tax for taxable income of $52,456 to $66,625 for single filers, and $104,911 to $133,250 for married filing jointly.

- 9.3% tax for taxable income of $66,626 to $340,375 for single filers, and $133,251 to $680,750 for married filing jointly.

- 10.3% tax for taxable income of $340,376 to $408,450 for single filers, and $680,751 to $816,900 for married filing jointly.

- 11.3% tax for taxable income of $408,451 to $680,750 for single filers, and $816,901 to $1,361,500 for married filing jointly.

- 12.3% tax for taxable income of $680,751 to $1,000,000 for single filers.

- An additional 1% tax (Mental Health Services Tax) on income over $1 million, making the effective top rate 13.3% for incomes over $1 million (single and married filing).

Example Calculating Capital Gains Tax

Suppose you sell an investment property in California with a profit of $100,000, after holding the property for two years. This profit directly impacts your overall tax bill, as it is added to your total income and taxed based on your applicable bracket.

To calculate California capital gains taxes:

Using the California online tax calculator provided by the FTB, with a total taxable income of $100,000, your California capital gains tax will be:

- $5,951 if you’re a single filer, at 5.951%

- $3,245 for a married couple filing jointly, at 3.245%

- $5,951 for a married couple filing separately, at 5.951%

Exemptions and Deductions on California Capital Gains Tax

As a real estate investor in California, you should be aware of the several exemptions and deductions that you can take advantage of to reduce your taxable income. These exemptions and deductions are defined in federal and state tax rules. Review the eligibility criteria with your CPA or tax advisor before claiming them on a return. Such exemptions and deductions include:

1. Primary Residence Exclusion

This is the most significant exemption for people selling their homes in California. Under the Primary Residence Exclusion, when you sell your primary residence, you can exclude up to $250,000 of capital gains for single filers, and up to $500,000 for married couples filing jointly.

To qualify for the primary residence exclusion, you must fulfill both the ownership test and the use test.

- The ownership test implies that you must have owned the home for at least two years within the five years preceding the sale of the primary residence.

- The use test requires that you have lived in the property as your main residence for at least two years out of the five years immediately before the sale of the home.

Note that you can meet the ownership and use tests during different 2-year periods as long as it’s within the 5-year period ending on the date of the sale. You do not qualify for the exclusion if you had previously excluded the gain from the sale of another primary residence within the two-year period preceding the sale of your home.

2. Adjustments to Basis: Improvements and Depreciation

The adjusted basis of your property is one of the most important factors in determining the capital gain of the sale and ultimately your net earnings. You can deduct certain costs and improvements to adjust the basis, thereby reducing the taxable gain.

To begin with, you can deduct the costs that are directly associated with the sale of the home from the selling price, giving you the net proceeds. Such costs include legal fees, real estate commissions, inspection fees, and Qualified Intermediary fees. You can also deduct the costs of major improvements that enhanced the value of the property.

Examples of such improvement costs include upgrading the HVAC system, installing a new roof, or adding new rooms. Additionally, if the property was used for rental purposes or business, you can subtract the real estate depreciation claimed during the period of ownership, which must be subtracted from the basis. Properly tracking basis adjustments is an important part of tax planning.

3. Loss Carryforward

If you incur capital losses, you can use them to offset capital gains. You can carry the remaining losses forward to future tax years if your capital losses exceed your capital gains. If the losses exceed the gains in a given year, you can deduct the excess loss against other income, up to $1,500 for people filing separately and up to $3,000 for married couples filing jointly.

4. A 1031 Exchange

The 1031 exchange was named after Section 1031 of the Internal Revenue Code. With a 1031 exchange, you can defer capital gains taxes by reinvesting all the sale proceeds of a relinquished property into a like-kind replacement property. That way, you get to pay capital gains taxes when you sell the new property instead of paying the taxes at the time of the sale of the old property. This strategy allows you to continue deferring capital gains taxes through subsequent exchanges as long as you adhere to the rules guiding the 1031 exchange.

Benefits of a 1031 Exchange

The primary benefit of the 1031 exchange is the ability to defer capital gains tax, allowing investors to grow tax deferred while reinvesting into new properties. The money you would have paid as capital gains tax becomes additional capital for reinvestment into the replacement property. In addition, a 1031 exchange also helps you strategically position your real properties for better market conditions and enhances investment returns.

For instance, you can exchange an empty land in a remote, less competitive area for an income-generating office complex in a developed area. The strategy also helps you diversify your assets. For example, if you have a portfolio of five rental apartments, you can swap one of them for a shopping complex, which adds a new source of potential income to your investment.

However, there are a few potential drawbacks you need to be aware of. To maximize the tax-deferral benefits, you must follow all the rules. Violating any of these rules may disqualify you from tax-deferral, and you’ll be liable to tax immediately. Additionally, the time constraints may result in pressure that may affect the smooth running of your exchange. Moreover, the complexities of the exchange can be challenging for new investors.

The best way to avoid all these drawbacks is to work with our expert, Qualified Intermediary at Universal Pacific 1031 Exchange. We act as your qualified intermediary, prepare exchange documents, hold exchange proceeds, and coordinate with your CPA, attorney, title, and escrow team throughout the 45-day identification and 180-day exchange windows.

Eligibility Criteria for a 1031 Exchange

To qualify for tax-deferral through a 1031 exchange, both the relinquished and the replacement properties must be like-kind, according to the IRS. Secondly, both investments must be held for investment or business purposes. Therefore, personal use properties do not qualify.

According to the Tax Cuts and Jobs Act, capital gains tax deferral under Section 1031 applies only to exchanges involving real property and not personal or intangible property. However, your exchange of personal or intangible property may still qualify if you sold the relinquished property on or before December 31, 2017, or received the replacement property on or before that date.

Another important requirement you need to be aware of is the timeline for a 1031 exchange. According to the IRS, you have a strict timeline of 180 days to complete a 1031 exchange. You must identify the replacement property within 45 days after the sale of the relinquished property. Then, you must acquire the replacement property and complete the purchase within the remaining 135 days.

If you miss any of these deadlines, the IRS may disqualify your exchange, and you would have to pay immediate capital gains taxes. Furthermore, you must reinvest all sales proceeds of the relinquished property to qualify. Any portion of the sales proceeds that is not reinvested is known as boot in a 1031 exchange, and this portion is subject to tax.

Moreover, you’re not allowed to receive the sale proceeds of the relinquished property or have constructive receipt of the funds as a taxpayer. You must use the services of a Qualified Intermediary, also known as an exchange accommodator. The QI holds the proceeds from the sale of the relinquished property and uses them to acquire the replacement property.

Remember to follow the 1031 exchange identification rules while identifying your potential replacement properties. The fair market value of the replacement property must be equal to or greater in value than the relinquished property. You can identify up to three replacement properties provided that you adhere to the three-property rule, the 200% rule, and the 95% rule.

Strategies for Minimizing Capital Gains Tax in California

There are a number of strategic steps you can take to reduce your capital gains tax liability and boost your investment portfolio. However, you must have a proper understanding of how these strategies work to avoid legal mistakes that may prove costly eventually.

To begin with, invest in retirement accounts with tax advantages, such as IRAs and 401(k)s. You would not have to pay tax on capital gains in this type of account until you withdraw. You can even withdraw tax-free with Roth IRAs under specified conditions.

Another strategy is to hold your investments for more than one year to qualify for long-term capital gains tax rates, which are typically lower than short-term rates. Additionally, invest in qualified Opportunity Zones. Investments held for certain periods can qualify for additional tax benefits.

Moreover, you can take advantage of the 1031 exchange to defer capital gains tax. To qualify using this strategy, you swap one investment property for another replacement property of like-kind. Be careful to complete the transactions within the stipulated timeline and follow all other rules specified by the IRS for a 1031 exchange.

Capital Gains Filing and Reporting Requirements

To stay compliant when you sell a property in California, you’ll have to report capital gains on both your federal and state tax returns. The first step is to calculate the capital gains or losses to get accurate figures. We’ve provided a summarized step-by-step guide below.

- Determine the sale price of the property.

- Deduct the expenses incurred during the sales, such as legal fees and commissions

- Calculate the adjusted basis by adding the improvements to the original purchase price and then subtracting the depreciation

- Subtract the adjusted basis from the net proceeds to determine the capital gain.

For federal tax reporting, report capital gains on IRS Form 8949, “Sales and Other Dispositions of Capital Assets.” You should include details such as the date of acquisition, date of sale, sale price, cost basis, and any adjustments. Then, summarize the totals from Form 8949 on Schedule D (Form 1040).

For California capital gains tax reporting, fill out the California Schedule D (540), “California Capital Gain or Loss Adjustment.” Note that you do not have to complete this schedule if all of your California gains are the same as your federal gains.

You also need to make sure that your tax reports are filed on time. Federal tax return for capital gains is typically due by April 15 of the following year. The California state capital gains tax return is also due by April 15 of the following year. For instance, for the tax year 2024, the deadline will be April 15, 2025.

Tips for Ensuring Accurate Filing of Capital Gains Tax

Since filing capital gains tax returns inaccurately may attract legal and tax consequences, you need to learn how to do it the right way. Here, we’ve provided you with some pro tips on how to ensure accurate filing of capital gains tax.

- Keep detailed records of the purchase price, improvements, selling expenses, and any depreciation claimed. It’s also important to save documents such as closing statements, receipts for improvements, and real estate commissions for future reference.

- Make sure you use the correct federal and state forms to report your capital gains accurately.

- Even if you didn’t make any gains, it’s best to include all sales and exchanges of capital assets.

- Be aware of the differences between the federal tax rates and those of California so you can calculate accurately and avoid errors.

- If your tax situation is complex, it might be better to hire a tax professional. For 1031 exchanges, you can consult our expert QI at Universal Pacific 1031 Exchange to guide you.

Have Questions about California Capital Gains Tax on Real Estate?

Your California real estate capital gains tax is an important part of your tax returns. That’s why you should learn how to calculate, defer, and report it accurately. Failure to adhere to the state tax rules may put you in trouble, disqualify you from tax benefits, and increase your tax liability.

If you’re looking to defer capital gains taxes through a 1031 exchange, Universal Pacific 1031 Exchange is the qualified intermediary services for investors in California and nationwide. With over 35 years of experience in facilitating successful tax-deferred exchanges, we can serve as your qualified intermediary, hold exchange proceeds in a segregated trust account, and coordinate the documents and deadlines. Book a free consultation with us to start an exchange.

Accuracy & Sources Disclaimer

The information in this article is sourced from official government publications and is accurate to the best of our knowledge as of the last update on March 18, 2026. All claims can be independently verified through the sources listed below:

Federal Sources:

- IRS Topic No. 409 — Capital Gains and Losses

- IRS Topic No. 701 — Sale of Your Home

- IRS Publication 523 — Selling Your Home

- IRS Publication 544 — Sales and Other Dispositions of Assets

- IRS Net Investment Income Tax (NIIT)

- IRS Like-Kind Exchanges Under IRC Section 1031

- IRS Like-Kind Exchanges — Real Estate Tax Tips

- 26 U.S.C. § 1031 — Internal Revenue Code, Section 1031

- IRS Form 8949 — Sales and Other Dispositions of Capital Assets

- IRS Schedule D (Form 1040) — Capital Gains and Losses

- IRS Opportunity Zones

- IRS Tax Cuts and Jobs Act — Business Comparison

California State Sources:

- California FTB — Capital Gains and Losses

- California FTB — 2025 Tax Rate Schedules

- California FTB — Online Tax Calculator

- California FTB — Schedule D (540)

- California FTB — Real Estate Withholding

- Mental Health Services Act (MHSA)

Tax laws are subject to change at both the federal and state levels. This content is for informational purposes only and does not constitute tax, legal, or investment advice.

FAQ

This section answers commonly asked questions regarding California’s real estate capital gains tax.

Does California tax capital gains as ordinary income?

Yes. California treats capital gains as ordinary income and applies the same progressive rates (currently 1% to 12.3%, plus the 1% Mental Health Services Tax on income above $1 million). There is no preferential long-term capital gains rate at the state level. The federal side may apply preferential long-term rates depending on holding period, income, and filing status. Review your transaction with a CPA or tax advisor.

Can a 1031 exchange defer California capital gains tax?

A properly structured 1031 exchange may allow eligible investment or business-use real estate sellers to defer capital gains tax (both federal and California) when proceeds are reinvested into like-kind replacement property within IRS deadlines (45-day identification, 180-day completion). A qualified intermediary holds the exchange proceeds and coordinates the documents. 1031 exchanges generally do not apply to primary residence sales. Review the structure with your CPA or tax advisor before closing.

Can selling expenses reduce my taxable gain?

Yes. Selling expenses such as broker commissions, title charges, escrow fees, and legal fees may reduce the amount realized from the sale, which lowers the estimated capital gain. Capital improvements made during ownership may also increase the adjusted basis, further reducing taxable gain. Both are entered in the calculator. Discuss the specifics with your CPA or tax advisor.

Does the Section 121 exclusion apply to all property sales?

No. The Section 121 exclusion ($250,000 for single, $500,000 for married filing jointly) applies only to qualifying primary residence sales where the seller owned and used the home as a primary residence for at least two of the five years before sale. It does not apply to investment, commercial, or other property types. Depreciation allowed or allowable after May 6, 1997 generally remains taxable even when Section 121 applies, and nonqualified use periods may further reduce the excludable gain. Confirm eligibility with a CPA or tax advisor.

How do you calculate capital gains tax on a property sale in California?

The calculator subtracts selling expenses from the sale price to get net sale price, computes adjusted basis (original purchase price plus capital improvements, less depreciation taken), and produces the estimated capital gain. California tax is estimated by applying the marginal California rate to the taxable gain. Federal tax is estimated separately, and depreciation-related tax impact, NIIT, and the 1% Mental Health Services Tax (above $1 million) are added when applicable. Results are estimates only.

What inputs do I need to estimate California capital gains tax?

You can enter property type, filing status, sale price, original purchase price, selling expenses, capital improvements, depreciation taken, capital losses, holding period, estimated taxable income, California sale and residency status, and (for primary residence) Section 121 exclusion plus nonqualified-use periods. A manual California marginal rate override is also available. Sale price and original purchase price are the minimum to produce an estimate.

How does the California capital gains tax calculator work?

The calculator runs entirely in your browser. It does not collect, store, or send any data. You enter the property and sale details, click Calculate Estimate, and the calculator computes net sale price, adjusted basis, estimated capital gain, Section 121 exclusion (where applicable), and the estimated California tax, federal tax, depreciation-related tax impact, NIIT, total tax, and after-tax proceeds. Each output is labeled “Estimated” and should be reviewed with a CPA or tax advisor before relying on it for a tax position.

Is this calculator an exact tax estimate?

No. This calculator is for educational and planning purposes only. Federal and California tax brackets change over time, and AMT, installment sales, capital-loss carryforward, multi-state apportionment, and other special situations can change the result. The calculator does not determine final tax liability. Use the figures for planning and confirm the actual tax with a CPA or tax advisor before reporting a sale.