1031 Exchange Process

The 1031 exchange involves a series of steps that savvy real estate investors must follow diligently to complete a successful tax-deferred exchange. If you fail to follow the steps correctly, your exchange may be disqualified, and you’ll incur immediate capital gains tax bills. Therefore, understanding the 1031 exchange process will not only make your exchange safer and easier but also help you comply with the IRS requirements and deadlines.

Universal Pacific 1031 Exchange has 35+ years of experience in facilitating successful exchanges across the 50 US states. We have helped thousands of property owners and real estate investors complete smooth and compliant exchanges while protecting their investment capital and deferring capital gains taxes. Contact us today to start an exchange.

This article will provide a simple and complete step-by-step guide to the 1031 exchange process, common mistakes you should avoid, the role of a QI in the process, and pro tips for a smooth and successful exchange.

What Is a 1031 Exchange and How Does It Work?

A 1031 exchange is a tax-deferral strategy that allows real estate investors to defer capital gains tax when they sell an investment property. To qualify, you must reinvest all the sale proceeds into a similar property while following some specific rules defined by the Internal Revenue Service (IRS).

According to the IRS Statistics of Income, over 100,000 taxpayers file Form 8824 each year to report like-kind exchanges, with nearly 200,000 filings recorded in a single tax year. This demonstrates that the strategy is not niche but a mainstream tax-deferral tool for investment property owners.

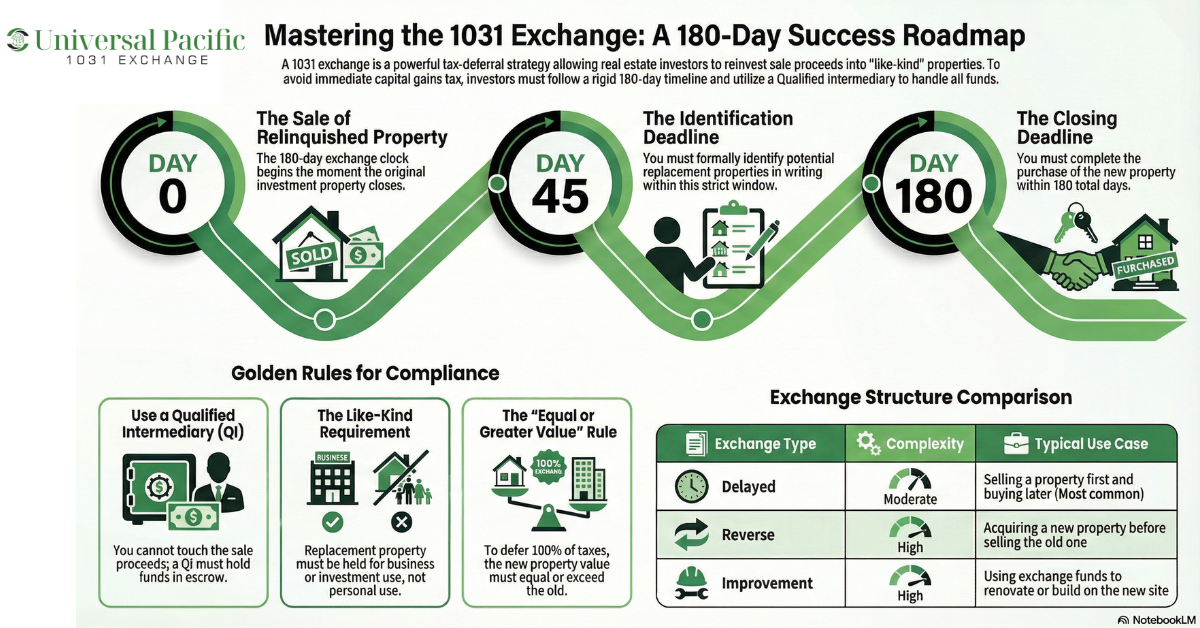

The process starts when you sell your existing property, called the relinquished property. From the date of sale, you have 45 days to identify potential replacement properties. You can identify multiple properties, but must follow certain rules, like the 200% rule, three-property rule, or 95% rule. While you don’t need to purchase all the properties you identify, you must close on at least one investment property.

After the 45 days, you have an additional 135 days to complete the purchase of the replacement property, making the total timeline for a 1031 exchange last 180 days. You must also follow other rules, such as the “equal or greater value” rule, using only like-kind properties used for business or investment purposes, and using a qualified intermediary. If you miss any of these requirements, your exchange won’t qualify, and you’ll owe capital gains tax immediately.

At Universal Pacific 1031 Exchange, we combine 35+ years of nationwide experience with a personalized, full-service approach. Unlike many firms, we coordinate directly with your real estate agent, escrow officer, and tax advisor, helping keep your exchange organized, timely, and aligned with applicable IRS requirements.

Case Study: How a 1031 Exchange Saved $120,000 in Capital Gains Taxes

In 2023, one of our clients sold a commercial office building valued at $800,000. By reinvesting the full proceeds into a mixed-use retail property through a delayed 1031 exchange, they deferred $120,000 in federal and state capital gains taxes.

The exchange was completed within 180 days, and the client was able to secure a property with higher rental income, improving cash flow by 15% annually. This demonstrates how careful planning and the use of a qualified intermediary can maximize the financial benefits of a 1031 exchange.

How Does A 1031 Exchange Work?

Completing a successful 1031 exchange involves a series of steps that you must follow carefully while also complying with the rules and requirements to maintain tax benefits. Below are the steps involved.

Step 1: Decide to Sell Your Current Property

The process begins when you choose to sell your current property that has been held for investment or business purposes. This could be a commercial building, apartment building, or other real estate property that produces cash flow. Many investors pursue an exchange to avoid a big tax bill they would otherwise pay after the sale, especially as part of long-term retirement planning.

Step 2: Engage Key Professionals Early

Before listing the property, assemble your team. This is typically a real estate agent, financial advisor, tax preparation specialist, and a Qualified Intermediary (QI). Your financial institution may also be involved if financing is needed for the new investment property. Early planning helps determine how many properties you can acquire and ensures the exchange property meets IRS rules.

Step 3: List and Sell the Relinquished Property

Your real estate agent markets the business property and secures a buyer. Once the relinquished property closes, the exchange timeline officially begins. You cannot take possession of the sale proceeds. They must go directly to the Qualified Intermediary, or the exchange will be disqualified, and you will have to pay tax.

Step 4: Funds Held by the Qualified Intermediary

The QI holds the proceeds in a secure account to prevent you from having constructive receipt of the money. This neutral third party facilitates the exchange and documents that the exchange occurred according to IRS requirements.

Step 5: Identify Replacement Property Within 45 Days

Within 45 days of the closing, you must formally identify potential replacement options in writing. You may identify one property or multiple options, depending on strategy and value rules. Investors often evaluate several new property choices, such as another commercial building or apartment building, to ensure strong future cash flow.

Step 6: Ensure the Property Is Like-Kind

The new property must be like-kind to the one sold, meaning both are held for business or investment use. For example, exchanging a rental property for a retail center qualifies, but exchanging into personal property does not. Partnership interests generally do not qualify as replacement property.

Step 7: Acquire the New Investment Property Within 180 Days

You must close on the new property within 180 days of the original sale, or by your tax filing deadline, whichever comes first. The Qualified Intermediary transfers the held funds to complete the purchase of the exchange property.

Step 8: Complete the Exchange and Continue Investment Use

After acquisition, the property must continue to be held for investment or business purposes. Selling too quickly or converting it to personal use could jeopardize the tax deferral. Many investors integrate the new property into long-term retirement planning strategies to grow wealth while deferring taxes.

Delays in financing through a financial institution can put the timeline in jeopardy, and the replacement property should be equal to or greater in value to avoid taxable differences. Speaking with a financial advisor in advance enables you to reinvest in a more lucrative real estate venture with improved cash flow.

Our 5-Step 1031 Exchange Framework

- Plan & Prepare – Evaluate your investment goals, assemble your team, and ensure financing is secured.

- Sell & Secure Funds – List the relinquished property and transfer proceeds to a Qualified Intermediary.

- Identify Replacement Properties – Within 45 days, list one or more like-kind options following IRS rules.

- Acquire & Close – Complete the purchase within 180 days while ensuring proper debt replacement and documentation.

- Integrate & Optimize – Hold the property for investment use, report the exchange via Form 8824, and plan for future portfolio growth.

What Are the Common Uses and Benefits of a 1031 Exchange?

A 1031 exchange, authorized under the Internal Revenue Code, allows investors to defer capital gains tax when they sell one investment real estate asset and purchase replacement property of the same nature. By reinvesting the full exchange funds instead of paying immediate tax liabilities, investors preserve more equity to grow their portfolios. This strategy applies only to property held for business or investment purposes, not a primary residence.

Many investors use exchanges to diversify their holdings, such as moving from a single apartment building into multiple properties or exchanging vacant land for income-producing assets. Others may consolidate several smaller properties into one larger asset to simplify management. This is because qualifying properties must be of the same nature.

A 1031 exchange also supports long-term estate planning by allowing investors to defer taxes indefinitely while repositioning assets over time. Preserving capital in this way can strengthen cash flow, expand ownership opportunities, and enable strategic upgrades without reducing purchasing power due to immediate tax payments.

What Are the Different Types of 1031 Exchanges?

A 1031 Exchange, named after Section 1031 of the U.S. Internal Revenue Code, allows investors to defer capital gains taxes by reinvesting proceeds from the sale of one investment property into another like-kind property. A clear grasp of the various exchange structures is essential, as each type follows specific timing rules, ownership requirements, and strategic advantages depending on the investor’s situation.

Delayed Exchange

The delayed exchange is the most common type and occurs when an investor sells the relinquished property first and then acquires a replacement property later. The 45-day identification period and the 180-day closing period run concurrently, starting from the sale of the relinquished property. During the identification window, the IRS allows investors to identify up to three potential replacement properties without regard to their value, provided they meet the like-kind requirement under Section 1031 of the U.S. Internal Revenue Code.

Simultaneous Exchange

In a simultaneous exchange, the sale of the old property and the purchase of the new one happen on the same day. Although rare today due to logistical challenges, this method eliminates the need for holding exchange funds over time. Even so, a Qualified Intermediary is typically used to ensure compliance, and that party cannot be a relative, attorney, banker, employee, accountant, or real estate agent of the exchanger.

Reverse Exchange

A reverse exchange allows an investor to purchase the replacement property before selling the relinquished property. This option is useful when an attractive property becomes available, but the current asset has not yet sold. Since the investor cannot hold both titles simultaneously under exchange rules, a special entity temporarily holds one property until the sale is completed within the required timeframe.

Improvement Exchange

An improvement exchange, also called a build-to-suit exchange, allows investors to use exchange funds to construct or renovate the replacement property. All improvements must be completed and the property acquired within the 180-day closing period to count toward the exchange value. This type is often used for new construction projects or when upgrading a property to better meet investment goals.

Multiple-Property Exchange

A 1031 exchange can involve selling one property and acquiring several replacement properties, or vice versa. This approach enables diversification across asset types, locations, or risk levels. Some investors also use structures such as Delaware Statutory Trusts (DSTs) or Tenant-in-Common (TIC) arrangements, which allow fractional ownership of larger properties while still qualifying as like-kind real estate.

Exchanges Involving New Construction

New construction can qualify if the property is completed and received by the investor within the exchange timeline. Investors often use improvement exchanges for this purpose, ensuring that the finished asset is conveyed before the deadline.

All exchange properties must be like-kind, meaning they are of the same nature or character as investment real estate, even if they differ in quality or type. The IRS generally treats residential, commercial, and industrial properties as like-kind to one another. If an investor cannot locate a suitable property in time, some consider DST interests as a backup option to meet the identification requirement.

The main advantages include deferring federal and state capital gains taxes, depreciation recapture, and the net investment income tax. However, real estate transactions carry liquidity risks, as properties can require significant time to sell without triggering taxes. Investors must also report the transaction by filing IRS Form 8824 with their tax return for the year the exchange occurs.

Choosing the Right 1031 Exchange Type: Pros and Cons

- Delayed Exchange – Most flexible, moderate risk, but requires careful timeline management.

- Simultaneous Exchange – Simple and low-risk, but rarely practical due to timing constraints.

- Reverse Exchange – Secures property before selling, but with higher complexity and cost.

- Improvement Exchange – Great for value-add strategies, but requires construction management within tight deadlines.

By weighing timing, complexity, and investment goals, investors can select the exchange type that fits their strategy.

Comparison of 1031 Exchange Types

| Exchange Type | Timeline | Complexity | Typical Use Cases | Risk Level |

| Delayed Exchange | 45-day identification, 180-day completion | Moderate | Most common: selling a property first and buying later | Low to Moderate |

| Simultaneous Exchange | Exchange happens on the same day | Low to Moderate | Quick swaps when both properties are ready | Low |

| Reverse Exchange | Acquire new property first, sell later | High | When the replacement property must be secured before selling | High |

| Improvement Exchange | Must complete improvements within 180 days | High | Renovating or improving the replacement property before finalizing | Moderate to High |

What Are the Common Mistakes in the 1031 Exchange Process and How Can You Avoid Them?

Although the 1031 exchange offers various benefits, investment property owners can lose out on those benefits if they don’t identify and avoid some common mistakes that may disqualify their transactions. Here are some of the most common errors you should watch out for:

- Missing the Identification Deadline – Remember that you have only 45 days from the sale of your old property to identify potential replacement properties in writing. Missing this deadline results in a failed exchange, and the sale becomes taxable. To avoid missing the deadline, you need to plan, work with a Qualified Intermediary (QI), and be sure the identification is submitted on time.

- Misunderstanding the Rules for Identifying Properties – The IRS provides specific rules for identifying replacement properties, such as the Three-Property Rule, the 200% Rule, and the 95% Rule. Misinterpreting these guidelines or listing properties that do not meet the criteria can invalidate the exchange. Carefully review these rules or seek professional advice to ensure compliance.

- Missing the 180-Day Closing Deadline – The entire exchange must be completed within 180 days from the sale of the relinquished property. This includes the 45-day identification period. Delays in closing the replacement property, whether due to financing, inspections, or other issues, can cause the exchange to fail. The solution is to stay organized and work closely with all parties involved to meet this deadline.

- Taking Possession of Sale Proceeds – If you take possession of the proceeds from the sale of the relinquished property, even temporarily, the exchange will be disqualified. Funds must be handled exclusively by a QI. To avoid this mistake, work with a reputable QI to designed to keep the funds safely segregated and the transaction remains compliant with IRS rules.

- Not Replacing Debt Properly – If there is debt on the relinquished property, such as a mortgage, the replacement property must have an equal or greater amount of debt, or you must contribute additional cash to make up the difference. Failing to meet this requirement results in taxable “boot,” which is the portion of the proceeds not reinvested.

- Attempting a DIY Exchange – Some investment property owners attempt to handle a 1031 exchange without professional help, which increases the risk of errors. The process involves complex legal and tax regulations that require some expertise. You need to hire an experienced Qualified Intermediary, tax advisor, and real estate attorney to see to it that everything is done correctly.

- Failing to Properly Report the Exchange – Even if the exchange process is completed successfully, failing to file IRS Form 8824 with your tax return can create issues. This form provides the IRS with detailed information about the transaction. Incomplete or inaccurate reporting can result in penalties or audits.

How Much Does a 1031 Exchange Cost?

On average, a 1031 exchange costs between $600 to $1200. However, it may cost more or less depending on how complex the exchange is, the professionals involved, and other factors. As an investor, you must understand these costs to help you budget effectively for a smooth and compliant exchange. The overall 1031 exchange costs include the qualified intermediary fee, title and escrow fees, closing costs, legal and tax advisor fees, inspection costs, and other applicable real estate transaction costs.

What Is the Role of a Qualified Intermediary in the 1031 Exchange Process?

The IRS requires the use of a Qualified Intermediary (QI), also known as an Accommodator or Facilitator, to ensure that the exchange process is timely and seamless. The QI holds the proceeds from the sale of the relinquished property in a secure escrow account, preventing the taxpayer from directly accessing the funds.

During the identification period, the QI assists the investor in formally identifying potential replacement properties within the given timeline. They also assist in preparing the necessary exchange documents, terms and conditions of the transactions, and coordinating with the closing agents. Once a replacement property is selected, the QI coordinates with the relevant parties to acquire the investment property within the exchange timeline.

“A qualified intermediary is not just a middleman; they are the gatekeepers of IRS compliance,” says Michael Bergman, CPA. “We’ve found that using an experienced QI reduces mistakes and ensures investors retain the maximum tax benefits.”

Another important role of a QI is to make sure that all the exchange steps adhere to IRS regulations and guidelines. This includes verifying that the properties qualify as like-kind, adhering to the 45-day identification and 180-day exchange timelines, and proper documentation. Throughout the process, the QI serves as a knowledgeable resource for the investor. They offer guidance, answer arising questions, and address concerns related to the exchange process.

What Are the Tax Implications of a 1031 Exchange?

By deferring capital gains taxes, investors can retain all of their investment proceeds, allowing for greater purchasing power in acquiring replacement properties. However, a 1031 exchange does not eliminate capital gains tax; it defers it. So, you’ll still have to pay the appropriate taxes when you sell the properties you acquired as replacement properties.

The investor’s cost basis in the replacement property is adjusted based on the gain deferred from the relinquished property. To calculate the basis in the replacement property, investors must carry over their adjusted basis from the relinquished property and add any additional cash paid for the replacement property.

A 1031 exchange can also have implications for estate planning. When an investor passes away while holding a replacement property acquired through a 1031 exchange, their heirs receive a stepped-up basis. This means that the basis of the investment property is adjusted to its fair market value at the time of the investor’s death.

What Are the Top 7 Tips for a Smooth 1031 Exchange Process?

With the right information and professional guidance, you can run a 1031 exchange without mistakes that may deprive you of the benefits, especially if you’re a beginner investor. Here, we’ve provided you with some pro tips to make the process easier for you.

- Plan – Start planning your 1031 exchange well before selling your property. Research replacement property options, secure financing if needed, and assemble your team of professionals early. Having a clear strategy will help you avoid the time pressures associated with the 45-day and 180-day deadlines.

- Work with an experienced, qualified intermediary – Since a QI plays various important roles in the process, their expertise and experience will determine if your exchange will be successful or full of errors. That’s why you must choose a QI with a proven track record of success in running the type of exchanges you want to conduct.

- Identify multiple replacement properties – When identifying replacement properties, consider listing more than one option so that you have alternatives if your top choice falls through. However, make sure you adhere to the rules involved in a 1031 exchange with multiple properties.

- Choose like-kind properties wisely – Confirm that the replacement property meets the like-kind requirement and aligns with your investment goals. Conduct thorough due diligence on potential replacement properties, including their condition, income potential, and market value, to avoid surprises after closing.

- Secure financing early – If you require financing for your replacement property, begin the process as soon as possible. Delays in securing a loan can jeopardize your ability to close within the 180-day window. Work with lenders experienced in 1031 exchanges to streamline the process.

- Maintain proper documentation – Keep detailed records of every step in the exchange, including sale agreements, identification documents, QI correspondence, and closing statements. These records will be essential for filing IRS Form 8824 and proving compliance in case of an audit.

- Consult with professionals – Engage experienced professionals, such as a real estate attorney, tax advisor, and QI, to guide you through the process. They can help you handle complex IRS rules, avoid pitfalls, and optimize the exchange for your financial goals.

In our experience, investors who begin planning 90–120 days before selling the relinquished property consistently avoid common pitfalls. We have seen clients miss deadlines simply because they waited to secure financing or finalize their QI. Our recommendation is to start early, communicate constantly, and document everything.

Ready to Start an Exchange?

A successful 1031 exchange must be carried out the right way to guarantee the deferral of capital gains tax and maximize other benefits that come with the exchange. From determining whether the strategy is suitable for you, to completing the exchange and filing a report with the IRS, each step of the way is as important as the next one. The best way to make sure you don’t miss your way in this process is to work with an experienced qualified intermediary and other seasoned real estate and tax professionals who will provide valuable assistance and guidance throughout the process.

At Universal Pacific 1031 Exchange, we help both new and experienced real estate investors navigate even the most complex of 1031 exchanges. Our team is skilled in guiding you through every step of the process with ease. We also work closely with your real estate agent, escrow officer, and tax advisor to keep the process smooth from beginning to end. Looking to start an exchange? Book a call today.

Frequently Asked Questions

In this section, we have provided answers to commonly asked questions about the 1031 exchange process.

What Types of Properties Qualify for a 1031 Exchange?

Only like-kind properties held for business or investment purposes qualify for a 1031 exchange. Personal residences, vacation homes, and inventory generally do not qualify.

How Long Do I Have to Complete a 1031 Exchange?

You must identify replacement property within 45 days of selling your original property and complete the exchange within 180 days. These deadlines are strict, and missing them can disqualify the exchange.

Can I Do Multiple 1031 Exchanges Consecutively?

Yes, investors can perform back-to-back 1031 exchanges, reinvesting proceeds from one property into another repeatedly. However, each exchange must follow the same timing and IRS rules.

What Happens if I Receive Boot a During an Exchange?

Any boot (non-like-kind property or cash received) is taxable to the extent it is not reinvested in a like-kind property. Receiving boot reduces the tax-deferral benefits of the 1031 exchange.

Is a 1031 Exchange Available for Primary Residences?

No, primary residences do not qualify for a 1031 exchange because they are not considered investment or business property. Only properties held for business, investment, or rental purposes are eligible.

Disclaimer: This content is for informational purposes only and does not constitute legal or tax advice. Please consult your tax advisor or legal professional before undertaking a 1031 exchange.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.