Are Real Estate Commissions Tax Deductible?

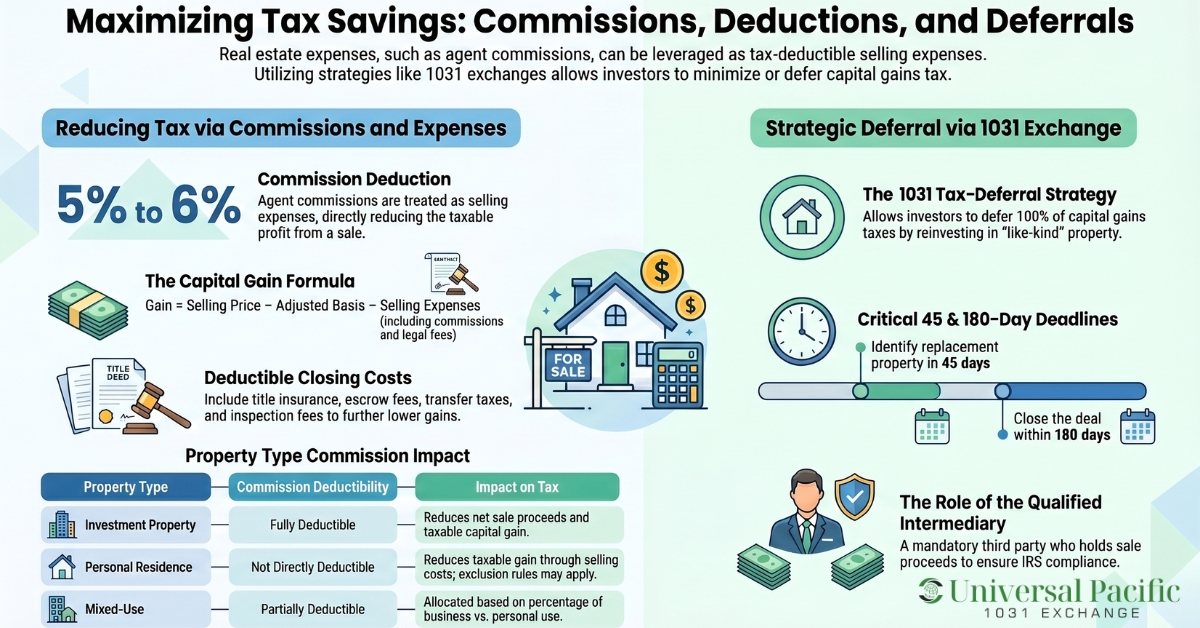

Short answer: Yes — real estate commissions are deductible from capital gains tax. The IRS treats agent fees as a selling expense, which reduces your net proceeds and lowers the taxable gain. You don’t subtract commissions from the gain itself; you subtract them from the sale price before calculating the gain.

You can deduct real estate commissions from capital gains when selling properties through a proper calculation of the cost basis. These commissions are considered a part of the selling expenses and are typically 5% – 6% of the property’s sale price.

Generally, they are tax-deductible and are one of the many tax loopholes real estate investors capitalize on to reduce their capital gains taxes. However, if you want to go beyond reduction to outright deferral of capital gains taxes in your real estate transactions, consider hiring a Qualified Intermediary to initiate 1031 exchanges for you.

Universal Pacific 1031 Exchange has over 35 years of professional experience in helping clients save their taxable income. Our experienced Qualified Intermediaries will hold your hands and guide you through the entire 1031 exchange process necessary to defer capital gains taxes in an IRS-compliant manner. Schedule a free consultation with us and let’s discuss how you can start your 1031 exchange.

This guide shows you how to deduct real estate commissions, how tax basis works, and how to achieve significant tax savings through 1031 exchanges. It also discusses how to calculate capital gains and common mistakes to avoid during such calculations.

What Are Real Estate Commissions?

Real estate commissions are the service fees you pay to brokers or real estate agents who help you buy or sell real property. The commissions are usually calculated as a percentage of the final sale price of the real estate.

They are part of what makes up the selling expenses of a deal, and are often split between the listing agent and the buyer’s agent. For example, if the total commission is 6%, the agents might divide it equally, with each agent receiving 3%.

Real estate commission rates have traditionally fallen between 5% to 6%. However, following the National Association of Realtors settlement in 2023, commission structures have shifted significantly. Buyer agent commissions are no longer automatically offered through the MLS by sellers, and rates are increasingly negotiable. The exact percentage depends on the location, type of property, prevailing market conditions, and individual agreement between the parties.

For example, you may find more flexible commission rates in a competitive market, as agents and brokers are willing to negotiate lower rates due to competition. Additionally, higher-value properties might have slightly lower percentage rates due to the larger base amount.

How Do Real Estate Commissions Work?

One of the first steps to selling a property is to contact a real estate agent to market it. To do this, you will reach a listing agreement with the agent, specifying the commission rate and other essential terms. Once agreed, they may list it on multiple listing services or advertise it both offline and online.

When a buyer indicates interest and makes an offer for the property, the buyer’s agent negotiates with the listing agent. Basically, the buyer’s agent represents the buyer in the negotiation, while the listing agent represents the seller.

If they reach an agreement, the seller pays the agreed commission, which is typically deducted from the sale proceeds. When the deal is closed, both agents share the commission according to their agreement.

An Example Calculation of Real Estate Commissions

Suppose you sell an office complex for $500,000 at an agreed commission rate of 6%. The total commission amount will be $500,000 x 6%, which equals $30,000. Assume both agents agreed on a 50-50 split. Then, each agent gets $15,000 in commissions.

How Real Estate Commissions Affect Capital Gains Tax

When you sell an investment property, the real estate commission you pay to agents can actually help reduce your capital gains tax. This is because the commission is treated as a selling cost. Instead of being taxed on the full sale price, you are taxed on your profit after subtracting certain expenses, including the commission.

Capital gains are calculated by taking the selling price of the property and subtracting your adjusted basis and selling costs. Your adjusted basis is usually what you paid for the property, plus the cost of improvements, and minus any depreciation taken over time. When you include the real estate commission as part of your selling costs, it reduces the total profit (or gain) you made from the sale. A lower gain means less income is subject to capital gains tax.

For example, imagine you sell a property for ₦50,000,000 and pay a 5% commission, which is ₦2,500,000. If your adjusted basis in the property is ₦30,000,000, your gain without considering the commission would be ₦20,000,000. However, after subtracting the commission, your net sale proceeds drop to ₦47,500,000, making your actual gain ₦17,500,000. This smaller gain means you will owe less tax.

In simple terms, real estate commissions lower your taxable profit because they increase your total selling expenses. By reducing the amount of gain you report, they can help decrease the capital gains tax you owe.

Can You Deduct Real Estate Commissions from Capital Gains?

Yes, you can deduct real estate commissions from capital gains when you sell a property. They are considered part of the tax-deductible selling expenses that you can subtract from the selling price to calculate the net capital gains from the sale.

Other kinds of selling expenses, according to IRS Publication 523, include advertising fees, repair costs, legal fees paid by the seller for drafting and negotiating the sales contract, and loan charges also paid by the seller.

In addition to these, IRS Publication 551 allows taxpayers to deduct another class of expenses, known as closing fees, during capital gains calculation, further reducing their taxable income. These closing costs include legal fees paid by the buyer for title examination and due diligence, escrow fees, transfer taxes, inspection fees, and Qualified Intermediary fees.

Others include title insurance, transfer fees, recording fees, survey fees, and the cost of installing utility services. Closing fees are generally added to the cost basis of a property and may be paid by the buyer, the seller, or both. For instance, each party will pay their respective fees.

However, in the case of transfer taxes, the state’s law will determine the outcome. In most states, the seller pays, while in a few states, such as Delaware, it’s split between both parties. Among these fees and expenses, commissions are usually the highest, ranging between 5% to 6% of the sales price.

Comparison of Tax Treatment: Personal Residence vs Investment Property Commissions

| Property Type | Are Commissions Tax Deductible | Effect on Adjusted Basis | Notes/Exceptions |

| Personal Residence | Not directly deductible | Does not change basis, but reduces taxable gain through selling costs | May still reduce capital gains when calculating profit; primary home exclusion rules may apply |

| Investment Property | Yes, as a selling expense | Does not change basis, but reduces net sale proceeds (and gain) | Fully counted as a cost of sale, lowering taxable capital gain |

| Rental Property | Yes, as a selling expense | Same as investment property | Depreciation recapture may still apply, which can increase the taxable amount |

| Mixed-Use Property | Partially deductible | Allocated based on business vs personal use | Must split commission between personal and investment portions |

How to Deduct Real Estate Commissions from Capital Gains

There are a few simple steps to take when deducting real estate commissions from capital gains. However, these involve financial calculations that could result in inaccurate figures and tax reports if done incorrectly. The steps are as follows:

- Start by deducting the real estate cost basis of the property, which is the original cost of the property that the seller paid when they initially purchased it.

- Next, calculate the adjusted basis of the property. The adjusted basis is the total of the cost basis, deductible closing costs, and any improvements that have increased the property’s value, such as renovations or additions. Then subtract the depreciation from the total.

- Determine the listing price of the property. Instead of fixing any price that comes to mind, it’s wise to hire an appraiser to do a proper appraisal on the property to first determine its fair market value (FMV). Use this appraisal and any other considerations to determine the selling price.

- Calculate the real estate commissions you are to pay, depending on the agreed percentage. For instance, if the rate is 6% for a property sold at $200,000, the commission will be $12,000.

- Deduct the commissions and other selling expenses, such as legal fees, inspection fees, and advertising costs, from the selling price to calculate the proceeds realized from the sale. Subtract the adjusted basis from the proceeds realized to get the actual capital gain.

What Qualifies as Capital Gains in Real Estate?

In real estate, capital gains are the profit you make from selling a property. This is the amount realized after all expenses incurred during your initial purchase of the property and eventual sale have been deducted.

As a real estate investor, it’s important to know how to calculate capital gains, as it directly affects your real estate capital gains tax. Generally, capital gains are a function of your property’s adjusted basis, selling price, selling expenses, and the real estate depreciation.

Adjusted Basis is calculated as follows:

Adjusted Basis = Original Purchase Price + Improvement Cost + Closing Costs – Depreciation

On the other hand,

Your Capital Gain is: Selling Price – Adjusted Basis – Selling Expenses

What Are Capital Gains Tax Rates in California?

The capital gains tax rate in California is 1% to 13.3%, depending on your income. The State of California treats all capital gains as ordinary income. Basically, the higher you earn, the more tax you pay. Those earning less than $11,079 per annum pay only 1%, while those who earn above $1 million pay 13.3%. These brackets are based on the 2025 California tax rate schedules published by the Franchise Tax Board.

In between these two ranges are eight other categories of taxes. As a resident or property owner in California, you will pay the ordinary income tax and also pay the federal capital gains tax. The federal capital gains tax rate depends on how long you’ve owned the property and how much profit you made.

If you hold the property for one year or less before selling it, it’s considered short-term capital gains. On the other hand, holding the property for more than one year qualifies the sales profit as long-term capital gains. Federal short-term capital gains tax rates have seven brackets, depending on your exact income. It ranges from 10% – 37%, payable under your federal income tax.

The long-term capital gains tax is a standalone tax, and it ranges from 0% – 20%, depending on your taxable income and filing status. The tax is further divided into three categories, depending on the exact amount you earned and whether you’re filing as a couple or an individual. In addition to this and the California ordinary income tax, real estate investors may also owe the 3.8% Net Investment Income Tax (NIIT) if their modified adjusted gross income exceeds $200,000 for single filers or $250,000 for married couples filing jointly.

How 1031 Exchanges Impact Real Estate Commissions and Capital Gains

A 1031 exchange is a real estate tax-deferral strategy that allows real estate investors to defer capital gains taxes by reinvesting the proceeds from the sale of an investment property into another like-kind property. It is also known as a like-kind exchange and is named after Section 1031 of the Internal Revenue Code.

Deferring capital gains tax through a 1031 exchange is one of the best ways to postpone ordinary income and capital gains taxes, thereby reducing your overall tax bill and making more investment capital available. To successfully defer capital gains tax using a 1031 exchange, you must follow all the rules and timelines set by the IRS.

To begin with, you have 45 days from the sale of the relinquished property to identify the potential replacement properties. Then, you must acquire the replacement property and complete the exchange within a total of 180 days from the date of the sale.

Note that failing to meet the replacement property identification rules may disqualify your exchange from tax deferral and expose you to immediate tax liability. Another requirement you need to adhere to is to transact only properties held for business or investment purposes. On that note, personal residences do not qualify.

However, there are strict 1031 exchange provisions for primary residence that could qualify your personal home sale, provided that you convert it into a rental property. In addition to these rules, you must hire a Qualified Intermediary (QI) to run the exchange. Otherwise, the IRS will reject it.

One of the responsibilities of the qualified intermediary is to hold the sale proceeds of the relinquished property until it’s time to buy the replacement property. This arrangement helps you stay compliant, as the IRS prohibits an investor from taking constructive receipt of the sales proceeds in a 1031 exchange.

The QI may also help you to properly document your transactions and guide you on how and where to report 1031 exchanges on tax returns. Universal Pacific 1031 Exchange is the best Qualified Intermediary services provider in Los Angeles and California at large. Our experienced Qualified Intermediaries can help you complete a smooth, compliant exchange without the stress.

7 Most Common Mistakes in Calculating Capital Gain and How to Avoid Them

It’s important to make sure that you pay the correct amount in capital gains tax, conduct accurate tax reporting, and avoid legal consequences. One of the major hindrances to achieving this stems from the misconceptions investors have about capital gains. Here are some of them.

- Many investors misunderstand the formula and thus miscalculate the adjusted basis of their properties. Calculating the property’s basis without adding home improvements or closing costs may lead to a higher taxable gain. To avoid this, consult a tax advisor or a real estate attorney to help you make informed decisions and vet your calculations.

- Some investors also ignore depreciation recapture. You can defer depreciation recapture in a 1031 exchange since it’s transferred to the adjusted basis of the replacement property. But if you eventually sell the replacement property without a 1031 exchange, you’ll have to recapture the depreciation. At the federal level, depreciation recapture on real property is taxed at a maximum rate of 25% under Section 1250, regardless of your long-term capital gains bracket. At the state level, California taxes recaptured depreciation as ordinary income at rates up to 13.3%.

- Another common mistake is failure to consider the correct holding period for calculating capital gain. Remember that the tax rate for short-term and long-term capital gains may differ, depending on your jurisdiction.

- Some investors overlook the Primary Residence Exclusion. Under the Primary Residence Exclusion, you can exclude up to $250,000 ($500,000 for married couples filing jointly) of capital gains when you sell your main home. If you’re not aware of this tax exemption, you may end up paying much more tax than you should. To prevent this, seek guidance from a tax professional or an experienced qualified intermediary so you can find out the tax-deductible costs and exemptions applicable to your exchange.

- Another common error is not keeping detailed or accurate records. Failing to document your transactions or keep accurate records of important details, such as purchase and sale dates and prices, can lead to incorrect calculations of the holding period and other relevant parameters. The remedy is to treat every document as an essential piece of evidence for potential issues with the IRS. The documents to store securely include contracts and agreements, receipts, and other forms of proof of payments.

- Additionally, many people who intend to defer capital gains tax via a 1031 exchange fail to apply the rules appropriately. This mistake is costly; the consequence is that the validity of the exchange will be revoked, meaning that you will have to pay capital gains tax immediately. To enjoy the full tax benefits, pay extra attention to all the 1031 exchange requirements and strive to adhere to them.

Need Help Deferring Capital Gains Tax?

Many expenses involved in closing a real estate property sale, including real estate commissions, are tax-deductible. Understanding how to use these in your cost basis calculations will help you reduce your tax liabilities. They also play a role in ascertaining your true capital gains.

Notably, you can defer these taxes for as long as you want by leveraging 1031 exchanges. All you need is to stick to the IRS rules guiding such transactions and work with a reputable Qualified Intermediary.

Universal Pacific 1031 Exchange is an experienced provider of Qualified Intermediary services in Los Angeles and all other major cities in the US. We will help you structure your transaction to defer capital gains tax while ensuring that all deductibles, including real estate agent commissions, are duly accounted for. Book a free consultation now to start an exchange.

The information in this article is sourced from official government publications and is accurate to the best of our knowledge as of the last update on March 18, 2026. All claims can be independently verified through the sources listed below:

- IRS Publication 523 — Selling Your Home

- IRS Publication 551 — Basis of Assets

- IRS Topic No. 409 — Capital Gains and Losses

- IRS Topic No. 701 — Sale of Your Home

- IRS Net Investment Income Tax (NIIT)

- IRS Like-Kind Exchanges Under IRC Section 1031

- 26 U.S.C. § 1031 — Internal Revenue Code, Section 1031

- IRS Form 8949 — Sales and Other Dispositions of Capital Assets

- IRS Schedule D (Form 1040) — Capital Gains and Losses

- IRS Form 8824 — Like-Kind Exchanges

- California FTB — Capital Gains and Losses

- California FTB — 2025 Tax Rate Schedules

Tax laws are subject to change. This content is for informational purposes only and does not constitute tax, legal, or investment advice.

FAQs

Below are common questions about real estate commissions and their provided answers.

What Costs Can Be Deducted From Capital Gains Taxes?

Costs that can be deducted from capital gains taxes include title insurance, legal fees, survey fees, recording fees, capital improvements, advertising costs, home staging, and repair costs. These deductions are broadly classified under closing costs and selling expenses.

Can I Deduct Realtor Commission on My Taxes?

Yes, you can deduct realtor commission on your taxes because it is considered a selling cost. However, you cannot deduct it as a direct expense on your annual income tax return. It is usually deducted from the sales proceeds of a property when calculating the capital gain or loss, which reduces the capital gains tax you owe.

What Can You Deduct From Capital Gains When Selling a House?

During a property sale, a homeowner can deduct the adjusted basis of the property and all selling expenses incurred from the selling price. Selling expenses include money spent in the form of attorney fees, advertising costs, and repairs. Additionally, the primary residence exclusion can greatly reduce or even eliminate your taxable gain.

Are Real Estate Commissions Deductible From Capital Gains?

Yes, real estate commissions are deductible from capital gains as part of the selling expenses. Doing so will reduce your capital gains taxes.

What Closing Costs Are Tax-Deductible?

Tax-deductible closing costs include title insurance, legal and accounting fees, recording and transfer fees, appraisal and inspection fees, Qualified Intermediary fees, and escrow fees.

Are Real Estate Commissions Added To Basis?

Yes, real estate commissions can be added to a property’s cost basis if the buyer paid a part or all of it. However, if the home seller pays for it, the commission will be added to the selling expenses.

Do Realtor Fees Reduce Capital Gains?

Yes, realtor fees reduce capital gains. They are part of the tax-deductible selling expenses that must be subtracted for a more favorable capital gains tax.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.