How to Determine the FMV of Like kind Property You Received

If you are considering a 1031 exchange, you need to understand what it entails and the role fair market value (FMV) plays in ensuring your 1031 exchange meets the Internal Revenue Service (IRS) requirements. The FMV dictates your tax burden and can largely influence your property deals and estate planning.

One of the major reasons to be concerned with a home’s FMV is that the value of real estate assets regularly fluctuates due to factors like location, interest rates, inflation, government policies, and current market conditions. As a result, you need to go the extra mile to ascertain the fair market value of your asset before entering any deal, especially a 1031 like-kind exchange.

Universal Pacific 1031 Exchange is the firm to count on when conducting qualified and successful 1031 like-kind exchanges. We have several licensed CPA professionals with decades of experience that can help you handle your 1031 exchange transactions successfully. Contact us today to have us serve as your Qualified Intermediary and rest assured that we will offer you the best deal with fully deferred capital gains tax.

This article will walk you through all you need to know about the FMV of property received and the various methods to calculate FMV. Let’s get started!

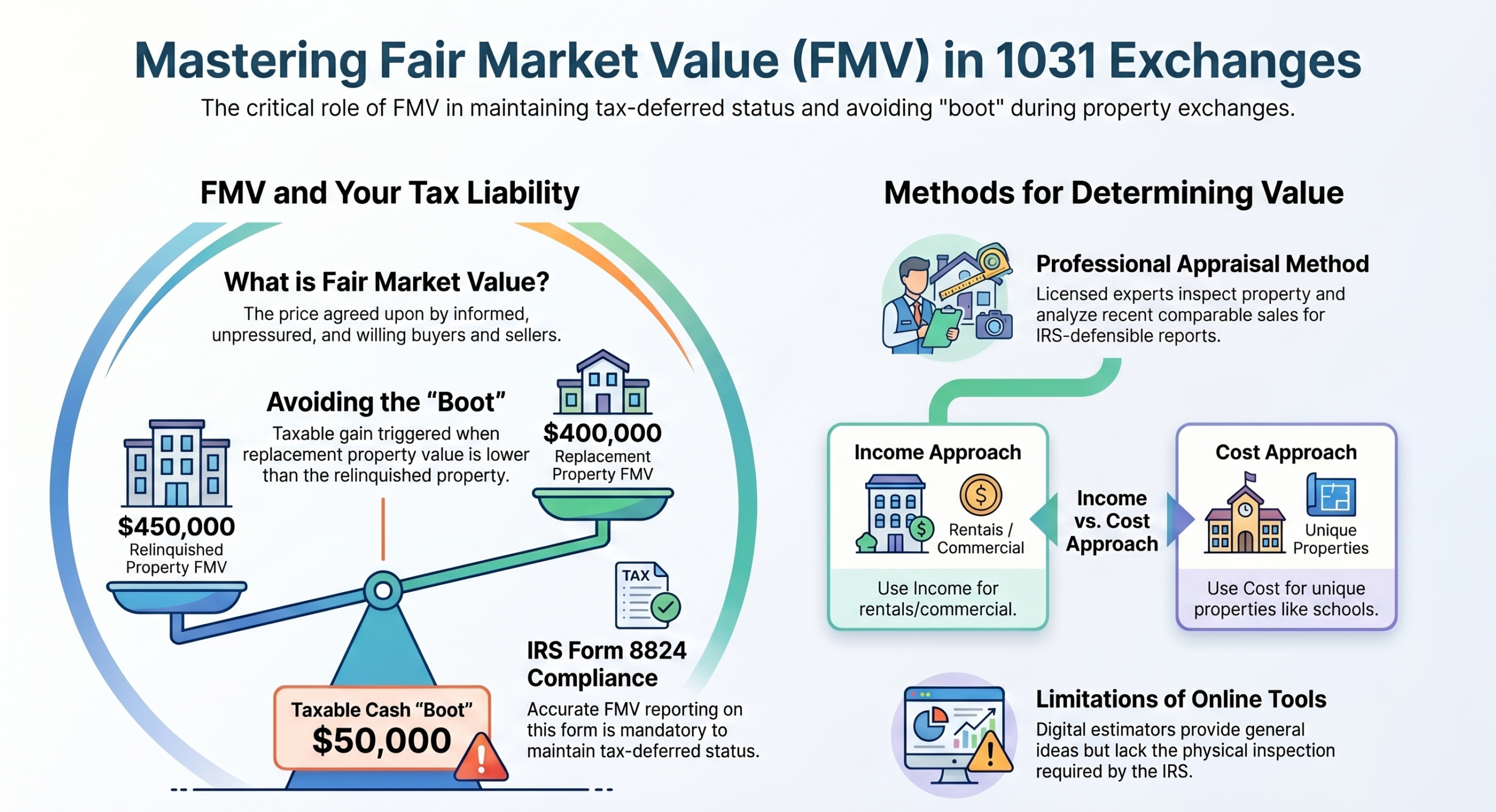

What Is Fair Market Value (FMV)?

Fair market value is the price at which an informed and unpressured seller would sell a property to an informed, unpressured, and willing buyer. That means it’s the standard or fair price any right-thinking person with reasonable knowledge would pay for an asset, given prevailing market conditions.

Determining the fair market value of inherited properties and other kinds of real assets offers numerous benefits. Predominantly, it will help you avoid boot and other tax liabilities. Boot in 1031 exchange is the taxable gain from the transaction that was not reinvested in purchasing the replacement property. Some key factors that determine the fair market value of any property include:

- Market Conditions: Supply and demand, interest rates, seasonal variations, changes in government policies, etc., can affect a property’s fair market value.

- Comparable Sales: The latest sale of similar properties (based on size and other physical features) in the same area will contribute in determining the appraised value of a real asset from the standpoint of a willing buyer.

- Location: Location factors like accessibility, proximity to infrastructure, entertainment, and recreation can also significantly affect a home’s fair market value.

- Property’s Physical Condition: Every willing buyer will inspect a home’s physical conditions before determining how much to commit. This includes the size, quality, and design layout of the asset.

- Appraisals: Real estate assessors can also inspect the property and provide their expert opinion on its value.

FMV in Specific Contexts – How Does It Work

Fair market value works differently depending on the context. Here are three of the most common case scenarios where it applies:

- 1031 Exchange and Investment Property: When swapping a property for another, the replacement property must be of like-kind and equal or similar market value to the relinquished property. Fair market value is the yardstick for measuring the value of both properties, and accurate assessment reduces further Internal Revenue Service (IRS) scrutiny. You just need to ensure that you do not receive excess cash or accept non-like-kind assets that can trigger a taxable event.

- Estate Planning and Inheritance: When someone dies, the fair market value of their assets on the day of death becomes the stepped-up value. This means the heirs will inherit the property at the current market value and not the initial purchase price. This stepped-up basis reduces capital gain taxes when the beneficiary eventually decides to sell the property. A proper fair market value assessment will ensure a fair distribution of assets among the beneficiaries. It also eases the process of tax calculation and ensures the estate pays the correct amount of taxes.

- Gifts and Donations: For every gift or donation you make, the fair market value remains a benchmark for determining potential gift tax implications. You can easily deduct the fair market value of your donation on your tax return. Thus, the property must be subject to appraisals and documentation. According to the Internal Revenue Service, there are annual and lifetime gift tax exclusions. Anything that exceeds these limits will be subject to a gift tax. With the fair market value, you can ascertain if the property exceeds these limits.

FMV and Its Impact on the 1031 Exchange

In real estate, fair market value is more than just a number; it is crucial for calculating the tax liabilities in a 1031 exchange. An investor looking to avoid costly tax mistakes and maximize returns should understand how fair market value works and its impact on different real estate transactions.

Tax Implications of FMV

Exchanging a non-like-kind property or receiving extra cash in a tax-deferred real estate transaction, such as a 1031 exchange, will trigger an immediate taxable event known as “boot.” For example, suppose the fair market value of a property is $1,000,000, and the replacement property is worth $800,000. To balance the deal, you will receive $200,000 in cash from the willing seller.

In that case, your boot is $200,000. Boot cannot be deferred. You’d have to pay immediate tax on the $200,000 while any capital gain on the $800,000 remains deferred. The only way to avoid this is to spend the $200,000 on renovating or repairing the new property.

Importance of Accurate FMV

The role of fair market value for tax purposes cannot be overemphasized. From gift and estate tax to capital gains calculations, generating an accurate fair market value of your real estate assets will give you a solid defense during any IRS audit. It would also help you to create and maintain records of your appraisals and other valuation methods that will reduce the risk of penalties in the future.

Hence, your best bet is to rely on a professional appraiser’s expertise to determine your home’s market value. Because once the Internal Revenue Service suspects any foul play in your asset’s valuation, they will conclude you have an incorrect capital gain amount, causing you to pay more interest and taxes.

Importance of Determining FMV in Like-Kind Exchanges

FMV plays several roles in like-kind exchanges, without which you may be at risk of having your transaction disqualified.

One of the most important aspects of determining FMV is that it demonstrates IRS compliance by showing that the properties exchanged are of ‘like-kind’ or equal or greater value in line with the requisite IRC rules. This is important because, from a tax perspective, there are always snares waiting for you that the IRS can leverage to come after you.

Determining fair market value will help you avoid the potential pitfalls and penalties associated with overvaluing and undervaluing real estate assets. Remember, you can always consult a reputable, qualified intermediary to manage the exchange, structure the exchange costs, and ensure compliance with IRS rules and requirements.

Furthermore, fair market value allows you to compare the worth of the relinquished and replacement properties to ensure that the exchange is fair to both the buyer and seller. Hence, both parties involved can rest assured that the transaction reflects the current reality of the real estate market regarding the property.

When the deal goes through, you can also use the property’s FMV to calculate the deferred capital gains. And in the case of any boot, an accurate fair market value will help you ascertain the taxable portion of the exchange and pay the correct taxes. Without this, you are at risk of overpaying or underpaying taxes.

But it doesn’t stop there, as you can also leverage it to claim depreciation deductions on the replacement property. A correct fair market value is your tool for maximizing your tax benefits and ensuring that the depreciation schedule reflects the property’s value.

Another benefit of FMV for investors, especially new entrants, is its reliability in making informed investment decisions. This is important because most real estate agents are cunning and can hide relevant facts just to convince you to make a deal that is not in your best interest. Knowing the true worth of your real estate asset will help you make decisions that will give you great returns on investments.

Additionally, it reveals your property’s strengths and weaknesses even if you’re not ready to sell it. That way, you can identify the potential losses or gains and mitigate the risk before executing a real estate transaction.

You can also leverage your fair market valuation documentation as collateral for accessing favorable loans and a yardstick for good insurance packages. Before selling an insurance policy to clients, an insurance company may send its appraiser to ascertain the worth and condition of the building and the potential risk of covering it.

An independent appraisal will help you iron out discrepancies in case the insurance company undervalues your property or exaggerates the risk. Knowing your fair market value will also help in the proper distribution of assets to beneficiaries and the calculation of estate tax.

How to Determine the FMV of Property Received?

While there are several methods one can use to determine the fair market value of a property, these are the most common methods adopted by most real estate investors.

1. Appraisal Method

This is one of the most recognized ways of ascertaining the fair market value of property received in an open market. In this method, licensed and experienced appraisers conduct appraisals on properties to decide the market valuation of real property and ensure that the process adheres to applicable legal requirements.

They inspect the property, check the recent sales of similar properties within the vicinity, and use their findings to generate the FMV. All the findings will be compiled in an appraisal report, including their research method and the property’s fair market value. Usually, lenders or real estate agents review and verify the appraisal report for accuracy.

At times, the IRS disputes appraisals because they are generated by appraisers who don’t understand the nitty-gritty of like-kind exchanges. So, how can you ensure that an appraiser is qualified to determine FMV in a 1031 exchange?

The first step is to evaluate their credentials and experience. They should have the requisite certifications and training needed to carry out such appraisals. While it’s human to allow inexperienced appraisers to use your property as their first major break, the direct consequence of their mistakes will be significant tax liabilities.

So, you need to weigh your options properly. For the experienced ones, you may request to see the past jobs they’ve done to know how closely they relate to your property. Whatever you find, don’t make the decision alone; speak with your Qualified Intermediary.

However, the best course of action is to rely on reputable 1031 exchange firms, such as Universal Pacific 1031 Exchange, to refer a trustworthy appraiser. You can’t go wrong with this because you’d be sure they are sending an expert who is well-versed in how like-kind exchanges work.

2. Income Approach

This is a lesser-used technique where investors analyze generated income and other related factors to estimate the fair market value of real property under market conditions. It’s the ratio of net operating income (NOI) to the capitalization rate.

When applying this method, an investor must consider vacancy, operating efficiency, and property conditions that might influence future gain or loss. This method is often used for rental or commercial properties.

3. Cost Approach

Another strategy for determining the FMV of inherited properties is the cost approach. According to this method, the value of a property is the sum of the production costs and land value minus accrued depreciation. It assumes that a property’s fair market value is equal to the cost of building a similar real estate property from scratch. The cost approach often applies to unique properties like schools, churches, or other new properties with unique features, where comparable sales may be limited.

4. Special Considerations

It is important to note that there are some special circumstances to consider when calculating fair market value. For example, there is a reverse 1031 exchange, where you acquire the replacement property before selling the relinquished property.

Another example is the improvement 1031 exchange, where you exchange funds to improve the replacement property instead of selling it off. Any fair market value calculation you make in these cases must account for the timing of property acquisition and improvements.

5. Using Online Tools and Resources

Online estimators are one of the most popular digital tools for providing a general estimate of an asset’s value. They employ Automated Valuation Models (AVMs) that estimate FMV based on a property’s size, location, and features.

The AVM uses a combination of mathematical modeling and the property’s database to determine the fair market value of an investment property. Although they are fast, it’s not advisable to use them as the sole source of calculating FMV. You need an appraiser to inspect the place physically and work with tangible data.

Another common practice is to leverage public records and real estate data, such as comparable sales and market trends, to predict the value of an asset. Public record companies often do this, providing the information to investors, real estate brokers, and realtors who, in turn, use it to determine the fair market value of their assets.

While this is widely used for convenience, you should combine these records with other asset valuation methods to get accurate results. Always remember that market conditions change often, so you can’t afford to make mistakes by relying on unvetted valuations.

FMV in a Like-Kind Exchange Calculation Example

Let’s assume Chloe has a rental property in Los Angeles valued at $300,000. One year later, she decided to sell it to procure a similar asset in San Francisco. After hiring appraisers, she discovered the FMV of her asset is now $450,000.

To execute a like-kind exchange, Chloe needs an asset within the FMV range of her LA property. So she employed the services of a QI to sell the asset and find a replacement immediately within the timeline set by the IRS.

The QI sold Chloe’s property for $450,000 and found a similar rental property in San Francisco for $400,000. With Chloe’s approval, the QI bought the property and is left with a balance of $50,000. This balance is known as boot.

How much profit did Chloe make?

Chloe bought the old property for $300,000 and sold it for $450,000, giving her a total profit of $150,000.

Will Chloe pay any tax on her profit?

Because it’s a 1031 like-kind exchange, every profit on the sale proceeds will be deferred except the boot. That means out of the $150,000 profit, only $50,000 is taxable. So, Chloe has two options:

- Take the boot from the QI and pay an immediate capital gain tax on it.

- Ask the QI to use the boot to make necessary repairs on the new property.

IRS Guidelines: How to Report FMV in a 1031 Exchange

For every 1031 exchange, it’s crucial to accurately report the FMV of the properties involved on IRS Form 8824. This form is essential for complying with IRS regulations and ensuring the tax-deferred status of your exchange.

- In Part I of the form, provide details about the properties exchanged, including descriptions and dates of the transactions. You will also back it up with a qualified appraisal.

- In Part II, indicate the FMV of the like-kind properties you received and the relinquished properties you transferred. Ensure that the values are accurate to avoid potential tax liabilities.

- Complete the form carefully, including the value on the date of acquisition, as it will be used to calculate any gain that might be taxable in the exchange.

In addition to FMV, there are several other important terms and considerations you need to pay attention to when filling out IRS Form 8824. They include realized gain or loss, ordinary income, net liabilities assumed, taxable installment sale income, and tax-exempt organization.

Accurate FMV reporting is important so you do not attract penalties or invalidate the tax-deferred status of your 1031 exchange. Therefore, ensure you obtain professional appraisals and maintain thorough records to support your FMV valuations.

Are There any Regional Trends that Investors Should Consider When Evaluating FMV?

Yes, FMVs are significantly affected by several regional trends, especially natural disasters. Properties located in regions highly prone to wildfires, tsunamis, hurricanes, earthquakes, and other kinds of natural disasters generally have lower market value, irrespective of how exquisite they are in design and construction.

In the same vein, economic developments, population growth, and an increase in employment opportunities are positive indicators for increased FMV. So all these, including the prevalent tax policies, are factors that appraisers consider when they determine the fair market value of properties.

For instance, Phoenix, Arizona, is experiencing a favorable population growth of over 0.75% every year. Since the real estate market in the city is trying to catch up with the growth, the result is more housing demand than supply. Hence, when you want to sell your home, the fair market value in Phoenix should be significantly higher than it was the previous year.

What Happens If FMV Is Disputed in a 1031 Exchange?

When the FMV in a 1031 exchange is disputed, it can lead to complications and even jeopardize the property’s tax-deferred status. If the buyer and seller disagree on the FMV of either the relinquished or replacement property, the first thing to do is to attempt negotiation.

Both parties will present relevant documents to support their valuation claims. If this doesn’t work, they can try a mediation or arbitration session to find a neutral solution. This method is reliable but not always effective.

If the dispute persists, the buyer and seller can opt for a second appraisal from an independent professional. The second appraisal provides reliable evidence of the property’s value and will be a valid basis for further negotiation or legal proceedings.

A miscalculation will directly affect your 1031 exchange tax deferral. If the IRS finds that you gave an incorrect FMV report, they could invalidate the exchange and mandate you to pay immediate capital gains taxes. So, when next you disagree with an FMV estimate, you should:

- Seek advice from experienced tax advisors, real estate attorneys, or QIs to help you understand your rights and options and to guide you on how to proceed.

- Familiarize yourself with IRS regulations and guidelines regarding FMV in 1031 exchanges.

- Maintain records of all appraisals, market data, and communication related to the dispute.

- Understand your rights and options for resolving disputes, so you know when to engage in mediation or litigation

Need Expert Guidance in Your 1031 Exchange?

An accurate FMV is crucial to a successful 1031 exchange as it helps to make correct assessments of the replacement property and avoid financial losses. However, you should seek professional guidance from reputable Qualified Intermediaries because of the complex nature of such transactions. A QI will help you avoid common mistakes investors make during like-kind exchanges, and offer you relevant advice and support to get the best tax benefits from the deals.

At Universal Pacific 1031 Exchange, we can help you simplify the exchange process by offering expert advice and guidance on your property’s FMV and the actual 1031 exchange. Moreover, we have the most competitive QI fees for the quality of our services. Book a free consultation today to start your exchange.

FAQ

Below are common questions on how the FMV of a property is determined and their provided answers.

How Does Market Volatility Affect FMV During a 1031 Exchange?

The real estate market is quite dynamic, and the fair market value of properties in a region can spike or plunge in response to news or other factors. At times, property owners capitalize on this to adjust their proposed selling price if the deal isn’t closed yet. Hence, it’s important not to rely on an old appraisal of your property when you want to conduct a tax-like exchange.

The interval between the appraisal and exchange should not exceed a couple of months. If you have reasons to believe that certain factors must have affected the prices of real assets in your location since your last appraisal, hire another appraiser to determine the fair market value of your property again before taking any other action.

How Does the Location of Your Property Impact Its FMV in a 1031 Exchange?

The security status and the presence of certain social amenities in a location directly affect its public perception and, in turn, the FMV of every property there. For instance, properties located in regions with high crime rates are less desirable and have lower market values compared to their counterparts in other locations. If the situation doesn’t improve, the FMV will decline further and vice versa.

How Does a Qualified Intermediary (QI) Assist in Determining FMV for 1031 Exchanges?

Qualified Intermediaries don’t directly determine the fair market value (FMV) of properties. However, they play a strategic role in tax-like exchanges and real estate tax valuation. For a start, a QI understands the IRS requirements for a successful tax-like exchange and goes the extra mile to ensure the real estate tax valuation from your appraiser is 100% compliant with these requirements.

When the appraisal is completed, it’s the QI’s responsibility to ensure proper documentation and that the FMV is properly used in calculating the tax basis for your disposed property and the replacement one. They can also refer you to credible appraisers who will ensure that the appraisals won’t be disputed by either the IRS or the buyer.

What’s the FMV of Property Received?

The FMV of a property received is the worth of an inherited property as determined by an appraiser or through any other reliable means. It’s essentially how much a buyer would pay for the property under fair market conditions.

Can Market Value Be Higher or Lower Than Fair Market Value?

Yes, the actual market value may differ from the fair market value, but it should be reasonably close to it. The reason for the disparity is that the actual market value is affected by several sentiments, including emotions and real estate agents’ manipulations.

In fact, any individual or business has the right to attach any purchase price to their properties in the open market. However, the fair market value is the only valuation the IRS recognizes in cost basis calculations and other tax purposes.

How Is Fair Market Value Used in the Assessment of Municipal Property Taxes?

The State Internal Revenue Service relies on fair market value when ascertaining how much municipal property tax a person or business owes. The Municipal Assessor’s Office conducts the appraisal and calculates the ensuing tax on the property. However, if the owner believes the designated FMV is higher than what it’s truly worth, they can challenge the appraisal.

How Is Property Value Determined After an Accident or Total Loss?

To determine the new value of a property after an accident, you must make reference to its value before the accident. Typically, the IRS and insurance companies calculate the actual cash value of the property as follows: the pre-accident value – the cost of repair – depreciation. If the property was damaged beyond repair, the valuation from the insurance standpoint becomes the replacement cost – depreciation.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.