Can You Buy Multiple Properties in a 1031 Exchange?

Yes, you can buy multiple properties in a 1031 exchange. Investing in multiple properties through a 1031 exchange is an effective way to grow your real estate portfolio while deferring capital gains taxes. However, you must follow the IRS rules for identifying multiple replacement properties, which include the three-property rule, the 200% rule, and the 95% rule. We understand that these rules can be confusing sometimes, that’s why we’ve put together this comprehensive guide to help you run a 1031 exchange with multiple properties successfully.

With 35+ years of hands-on experience, our experienced qualified intermediaries at Universal Pacific 1031 Exchange have the expertise and experience to facilitate 1031 exchanges involving multiple replacement properties without violating any IRS requirement. We’re committed to guiding you through every step of the exchange process to make sure you comply with all necessary regulations while having a smooth exchange. Schedule a free consultation with us today to get started.

In this guide, we’ll cover everything you need to know about buying multiple properties in a 1031 exchange, including the rules, benefits, and step-by-step instructions to facilitate a successful transaction.

Can You Buy Multiple Properties in a 1031 Exchange?

Yes, multiple properties can be bought in a 1031 exchange. When you sell your relinquished property, you have the option to reinvest the proceeds into one or more replacement properties to defer capital gains taxes. The IRS allows you to buy multiple replacement properties as long as the combined total fair market value of the replacement properties equals or exceeds the value of the relinquished property (minus transaction costs).

Apart from the fair market value rule, the exchange must also satisfy all other requirements of a compliant 1031 exchange. With the liberty to invest in as many properties as possible, you get to diversify your real estate portfolio, acquire properties in different locations, or invest in varying property types.

On the flip side, you can also exchange two relinquished properties for one property. We’ve provided a detailed guide on how it works in our blog on how to 1031 exchange multiple properties for one.

The Rules for Buying Multiple Properties in a 1031 Exchange

Selling one investment property to buy multiple properties in a 1031 exchange is a strategic way to diversify and grow your investment portfolio. However, the 1031 exchange process can be complex and requires that you strictly follow IRS rules, especially concerning fair market value, identification, and timing. That’s why you need to understand these key rules to be sure your transactions are smooth and eligible.

1. Equal or Greater Value Rule

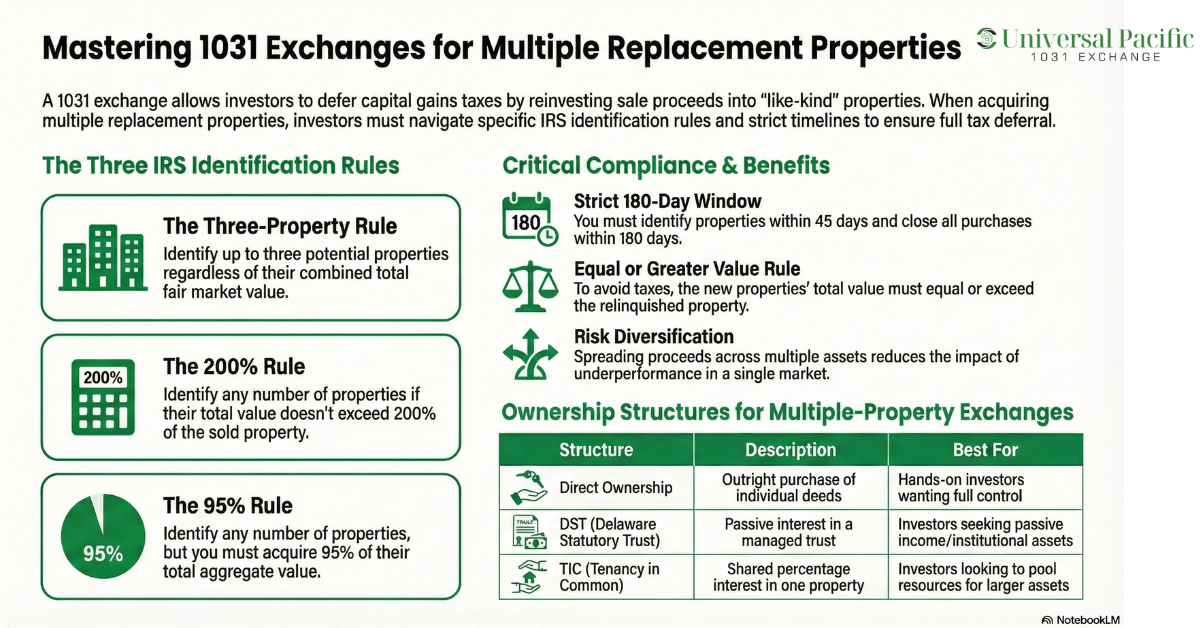

To defer capital gains tax completely, the total fair market value of the replacement properties must equal or be greater than the value of the relinquished property, adjusted for any transaction costs such as closing fees or commissions. If the sale proceeds are greater than the aggregate value of the replacement properties, the difference is treated as boot in a 1031 exchange, which is subject to tax. This rule applies not only to the purchase price but also to the debt.

2. Identification Rules

You must identify the potential replacement properties within 45 days of selling the old property. This identification must be submitted in writing to your Qualified Intermediary (QI). The IRS provides three methods for determining how many properties you can buy in a 1031 exchange:

- Three-Property Rule – You can identify up to three properties, regardless of their total market value. This means that the combined value of the properties can exceed the value of the relinquished property.

- 200% Rule – The 1031 exchange 200% rule allows you to identify more than three properties, provided their combined value does not exceed 200% of the relinquished property’s value. For example, if the relinquished property was sold for $1 million, you could identify properties worth up to $2 million in total.

- 95% Rule – You can identify any number of properties, even if their total value exceeds 200%, but you must acquire at least 95% of the aggregate value of the identified properties.

3. Timeline for Acquiring the Replacement Properties

You must complete the purchase of all identified replacement properties within the 180-day timeline for a 1031 exchange. This timeline includes the initial 45-day identification period, leaving only 135 days to finalize purchases. The timeline is strict and cannot be extended, so you need to work closely with your QI, lenders, and attorneys to be sure that all transactions are completed within this timeframe.

4. Other 1031 Exchange Requirements

While the above rules are the most specific to 1031 exchange with multiple properties, you must still adhere to all the other general requirements for a tax-deferred exchange. The additional rules include the following:

Like-Kind Requirement

For a 1031 exchange, the relinquished property and the replacement properties must be “like-kind.” According to the IRS, like-kind means both properties are of the same nature of character, regardless of any difference in quality or grade. The key requirement is that real property is exchanged for other real property located in the United States. This means that properties outside the U.S. cannot be exchanged for domestic properties.

Investment or Business Use

All replacement properties must be held for investment or business purposes. This rule excludes properties intended for personal use, such as a primary residence. However, you can convert a 1031 exchange rental to a primary residence after meeting the IRS’s “safe harbor” guidelines.

Use of a Qualified Intermediary

Moreover, remember that you need a qualified intermediary to hold and manage the proceeds from the sale of the relinquished property. The QI also facilitates the documentation required for compliance. Their role is especially critical when multiple replacement properties are involved. Therefore, you must learn how to find a qualified intermediary experienced enough to make your exchange successful.

Real-World Examples of Buying Multiple Properties in a 1031 Exchange

Below are practical examples showing how investors can use a 1031 exchange to purchase multiple replacement properties while staying within IRS rules. These scenarios highlight common strategies used to diversify income, reduce risk, and maintain full tax deferral.

Example 1: Selling One $1M Property → Buying Three $530K Properties

An investor sells an office complex for $1 million and identifies three apartment buildings valued at $530,000 each. The exchange remains fully tax-deferred when the investor buys the three identified replacement properties because their total value exceeds the relinquished property value of $1M, thus satisfying the three property rule.

Example 2: Using the 200% Rule to Identify Multiple Options

An investor sells a property for $800,000 and uses the 200% Rule to identify five replacement properties with a combined value of $1.6 million. The investor ends up purchasing only two of those properties with an aggregate value of $1.35 million. The transaction qualifies for tax deferral since the total value of identified properties did not exceed 200% ($1.6M) and the purchased replacement properties exceeded the relinquished property value.

Example 3: Mixing Direct Rentals and a DST

An investor sells a commercial property and reinvests part of the proceeds into direct rental properties while placing the remaining funds into a Delaware Statutory Trust (DST). This strategy allows for both active management through direct ownership and passive income through the DST. As long as all replacement assets qualify as like-kind investment properties, the exchange remains valid.

Benefits of Buying Multiple Properties in a 1031 Exchange

With proper planning and experienced guidance, investing in multiple replacement properties can be a powerful tool for maximizing the benefits of a 1031 exchange.

First, buying multiple properties allows you to spread risk across various assets, locations, or property types. Instead of reinvesting all proceeds into only one high-value investment property, you can purchase several smaller properties, reducing the potential impact of underperformance in any single asset.

Secondly, investing in multiple properties can create multiple streams of rental income, which can lead to higher overall returns. This investment strategy can be particularly beneficial if you’re transitioning from a single, non-income-producing property (such as land) to several income-generating properties (like apartment buildings or commercial rentals).

Furthermore, purchasing multiple properties enables you to access different markets and invest in various geographic locations, reducing the risk associated with market fluctuations in a single region. Additionally, you can mix property types, such as combining residential, commercial, and industrial properties, to capitalize on different market opportunities.

Moreover, owning multiple properties can make it easier to liquidate individual assets if needed without disrupting your entire portfolio. For instance, if you need to raise capital or adjust your investments, selling one property out of a portfolio of several is often simpler than selling a high-value single replacement property.

In addition to deferring capital gains taxes through the 1031 exchange, acquiring multiple properties can offer additional tax benefits. For example, depreciation deductions can be spread across multiple properties. Property-specific expenses can also be deducted, potentially lowering your overall taxable income.

Common Structures for Exchanging Into Multiple Properties

When buying multiple replacement properties in a 1031 exchange, you can choose from different ownership structures. Each option offers varying levels of control, management responsibility, and flexibility. The structures include:

1. Direct Ownership

With direct ownership, you purchase and own each replacement property outright. This structure gives you full control over management decisions, leasing, and future sales. It is best for investors who want hands-on involvement and long-term control of their assets.

2. Fractional Ownership Options

On the other hand, fractional ownership, also known as partial ownership, allows you to invest in larger or multiple properties by owning a shared interest rather than purchasing each property on your own. That way, you can reduce management responsibilities and diversify across different asset types. Examples of partial ownership structures in a 1031 exchange include:

- Tenant-in-Common (TIC): TIC ownership allows multiple investors to own a percentage interest in a single property. Each owner holds a separate deed and can exchange their interest through a 1031 exchange.

- Delaware Statutory Trusts (DSTs): With a DST, you can invest in institutional-grade real estate as a passive owner. The trust owns the property, and investors hold beneficial interests that qualify for 1031 exchanges. DSTs are ideal for investors looking for how to diversify in a 1031 exchange and maintain passive income without day-to-day management.

How To Buy Multiple Replacement Properties in a 1031 Exchange?

To successfully purchase multiple replacement properties in a 1031 exchange, you need careful planning, alignment with applicable IRS rules, and collaboration with qualified professionals. Here, we’ve provided a summary of the list of steps you need to take to make the process smooth.

- After confirming that you want to buy multiple properties, choose an experienced qualified intermediary early to guide you through the process.

- Sell your relinquished property, making sure the proceeds are transferred directly to your QI.

- Identify the potential replacement properties. Remember you can identify more than three properties, but make sure you follow the 1031 exchange identification rules as discussed earlier. Schedule inspections, appraisals, and environmental assessments to verify that the properties meet your investment criteria.

- Submit the properties identified in writing to your QI within 45 days of the sale.

- Work with your QI to allocate the sale proceeds across the replacement properties. Make sure the total value of the replacement properties equals or exceeds the value of the relinquished property, accounting for debt replacement if applicable.

- Complete the purchase of all identified replacement properties within the 180-day deadline. Make sure you document all transactions properly for reference.

- File Form 8824 with your federal tax return for the year of the exchange. You can refer to our blog on how to file a 1031 exchange to avoid mistakes that may attract tax consequences.

- Maintain accurate records, including identification notices, contracts, closing statements, and QI communications, to support your compliance with IRS regulations.

How to Maximize the Benefits of a Multiple Property 1031 Exchange

One of the things you can do to make the most of a 1031 exchange with multiple properties is to invest in properties that can provide a steady rental income. For example, buying multiple rental homes or commercial spaces can give you several sources of income, helping you earn more over time.

Before buying, research the areas where you want to invest. Knowing the market helps you make better decisions and avoid bad investments. You also need to use the IRS identification rules wisely. Analyze the three property rule, 200% rule, and 95% rule, and choose the one that’s most suitable for you. Moreover, buying properties that need some work can be a smart move. Look for properties you can improve to increase potential rental income or value.

Plan ahead to avoid missing deadlines. Work closely with professionals like your Qualified Intermediary (QI) and real estate agents to make sure everything stays on track. Apart from a QI, you also need help from other professionals, such as a tax advisor, who can help you use these benefits to save money.

Need a Qualified Intermediary for a Multiple-Property 1031 Exchange?

By reinvesting your relinquished property sale proceeds into up to three properties or more, you can expand your portfolio, create steady income streams, and reduce investment risk. Remember that you have to follow IRS rules, work closely with a qualified intermediary, and choose the right properties to fully maximize the benefits of this tax-deferred strategy.

As the best qualified intermediary in Los Angeles, California, and nationwide, Universal Pacific 1031 Exchange has all it takes to make your exchange stress-free and successful. Our experts are here to guide you through every step, ensuring you maximize your tax deferral benefits while achieving your investment goals. Reach out to us today to start an exchange and receive professional guidance throughout the exchange period.

FAQs

As experienced qualified intermediaries with 35+ years of experience, we’ve provided practical answers to some of the common questions people ask about buying multiple properties in a 1031 exchange.

Can I Combine Personal Funds With 1031 Proceeds?

Yes, you can add personal funds to complete the purchase of your replacement properties. Adding cash does not disqualify the exchange, but taking cash out of the proceeds may trigger taxable boot.

Do All Replacement Properties Have to Close On the Same Day?

No, replacement properties can close on different dates. However, all closings must occur within the 180-day exchange period.

Can I Buy Properties in Different States?

Yes, you can purchase replacement properties in different states because Section 1031 is a federal rule. As long as the properties are U.S.-based and held for investment or business use, they qualify as like-kind.

How Does Depreciation Transfer When Exchanging Into Multiple Properties?

Depreciation generally carries over from the relinquished property to the replacement properties. It is allocated among the new properties based on their purchase prices.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.