Essential 1031 Exchange Requirements

A 1031 exchange follows very strict rules and guidelines as set by the IRS, and missing any of these rules can make the transaction taxable. Some major 1031 exchange requirements include engaging a Qualified Intermediary and meeting the IRS 45 and 180-day timeline.

In addition, you must ensure that both the exchanged properties are like-kind in nature, and reinvest the entire proceeds in the purchase of the new property. Working with a Qualified Intermediary is key to ensuring that the entire exchange fully complies with the IRS guidelines.

Universal Pacific 1031 Exchange has 35+ years of experience in assisting both new and experienced real estate investors navigate the complex 1031 exchange procedures. We ensure that your funds are handled correctly and facilitate your exchange with documentation and processes designed to support IRS compliance. Contact us today to get started.

This blog covers what a 1031 exchange means, the key requirements for facilitating an exchange, and the benefits of a tax-deferred exchange.

What Is a 1031 Exchange?

A 1031 exchange is a provision under Section 1031 of the Internal Revenue Code that allows investors and other taxpayers defer capital gains taxes when buying or selling real estate investment properties. Instead of paying immediate taxes in the year the property was sold, the investor can defer capital gains taxes by reinvesting the proceeds from the sale of the relinquished property in a new eligible property. According to a quote from Justice Antonin Scalia:

“If you sell an investment property and use the money to buy another property of the same type, you don’t have to pay taxes on the profit right away. It helps investors keep more money working for them while growing their real estate portfolio.”

The main purpose of the 1031 exchange provision was to encourage reinvestment. When someone sells an investment property, there is normally a gain if the property increased in value and was sold for more than it was bought for. This gain is normally taxable in the eyes of the Internal Revenue Service (IRS).

However, under Section 1031 of the Internal Revenue Code, taxpayers can postpone paying those capital gains taxes if they reinvest in another qualifying like-kind property. This tax deferral helps real estate investors grow their portfolios, move into higher-income-producing properties, or shift from one type of property to another without losing a large portion of their profits to taxes right away.

How Do You Qualify for a 1031 Exchange?

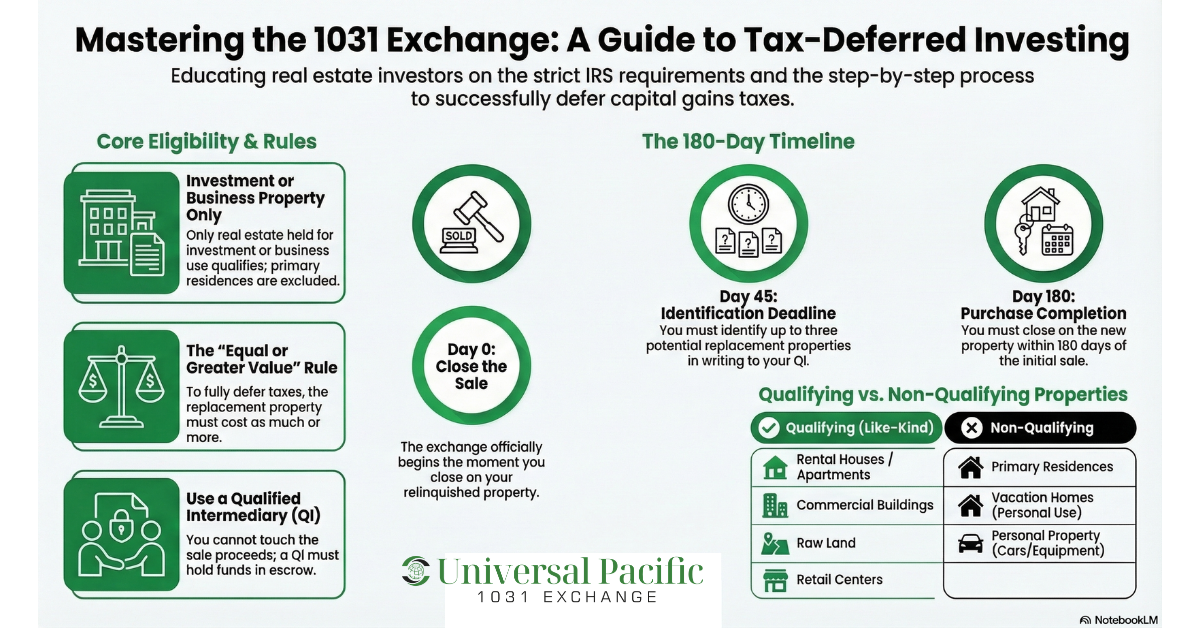

The first criterion to qualify for a 1031 exchange is that the property being sold must be an investment property or real property used for business, trade, or productive use. This basically constitutes like-kind and includes properties such as raw land, commercial buildings, condominiums, and retail centers.

Principal residences or property held mainly for personal use, such as vacation homes, second homes, and primary residences, do not qualify. The law applies to only real property, meaning that personal property, such as equipment or vehicles, is not eligible. The second requirement is that a Qualified Intermediary must be present to hold the sale proceeds and facilitate the exchange.

This is because the IRS forbids taxpayers from taking direct possession of exchange funds, and doing so could result in tax consequences. Adhering to the IRS’s strict timelines is also a critical requirement. The IRS requires that potential replacement properties be identified within 45 days after the sale of the relinquished property.

The properties must also be purchased within 180 days from the same sale date. These timelines run concurrently and are very strict. Additionally, to fully avoid a taxable event, the replacement property must be of equal or greater value than the relinquished property. Purchasing a lesser-value property can create a partial taxable gain. This happens because any difference in value, reduced debt, or cash received from the transaction may be treated as taxable income.

For a 1031 exchange to be considered valid, all the sale proceeds from the old property have to be reinvested into the new property. If you do not reinvest the full amount or buy a property that costs less than what you sold, the remaining fund, often referred to as “boot”, can become subject to capital gains taxes. This will also be the same outcome if you lower the amount of debt on the new property without adding additional cash to balance it out.

Let’s examine this real case study to further understand the importance of meeting all IRS requirements. In Christensen v. Commissioner, 142 F.3d 442 (9th Cir. 1998), the U.S. Court of Appeals for the Ninth Circuit upheld a ruling that a like-kind exchange failed because the taxpayer didn’t complete the exchange within the required tax filing period.

What Is the Process for a 1031 Exchange?

A 1031 exchange is much more complex than a simple sale and purchase. It is a structured transaction that follows strict IRS rules and requires that real estate investors stay compliant with these guidelines in order to execute a successful exchange. Below is a step-by-step framework on how a 1031 exchange is done.

Step 1: Hire a Qualified Intermediary Before You Sell

The first step in performing a like-kind exchange is to engage a QI. This must be done before you close on the property you are selling. The QI is a neutral third party who helps to prepare exchange documents and hold the sale proceeds. As previously mentioned, you cannot take control of the money from the sale of a relinquished property. Receiving the money directly automatically disqualifies the transaction and leads to a taxable sale. This step is one of the most important 1031 exchange requirements in the IRC Section 1031.

Step 2: Sell the Relinquished Property

The next step is to sell your old property. Before now, you must have confirmed that the property is held for investment or productive use in business. At the close of the sale, the proceeds are transferred to the Qualified Intermediary, who holds them in an escrow account until the replacement property is purchased.

Step 3: Identify Potential Replacement Property Within 45 Days

After the sale of the relinquished property, you have 45 days to identify potential replacement properties. This identification must be done in writing and submitted to your QI on or before the 45 days run out. At this stage, you can identify up to three properties even if you intend to purchase only one. The identified replacement properties must also be held for investment or business purposes and must have equal or greater value than the relinquished one.

Step 4: Purchase the Replacement Property Within 180 Days

You must purchase the property within 180 days after the sale of the original property. This timeline includes the 45-day identification period and cannot be extended except in rare cases. To fully defer capital gains taxes, you must fully reinvest the entire sale proceeds when purchasing the replacement property. The QI who holds the exchange funds uses them to purchase the property and then transfers the deed to you, closing the exchange.

Step 5: Complete Documentation and Report the Exchange

The exchange must be properly documented in order to avoid unnecessary errors when filing and prevent future audits. These documents include the exchange agreement, assignment forms, and written identification of the replacement property. Finally, the transaction must be reported on your tax return for that year. Finally, the transaction must be reported on your tax return for that year. Even though you defer capital gains taxes, the IRS still requires full disclosure of the exchange.

What Are the Benefits of a 1031 Exchange?

One of the biggest benefits of a 1031 exchange is the ability to defer taxes. Instead of losing a large part of your profit to taxes after a sale, you can defer those taxes by reinvesting the money into another qualifying property. According to statistics, 1031 exchanges generated around $97.4 billion in value-added to the United States GDP in 2021.

A 1031 exchange also gives investors room for flexibility. With this tax-deferral tool, you can move from one type of property to another as long as it qualifies as like-kind. For instance, you can exchange a small rental home for a commercial property, raw land, or a larger apartment building.

This allows you to upgrade, reduce management, or move into a stronger market without triggering immediate tax liability. Another major benefit is portfolio diversification. Investors can shift their holdings into different property types or different locations to reduce risk. Instead of keeping all your investments in one area or in one type of property, a 1031 exchange makes it easier to adjust your strategy while keeping your money invested.

What Are Common Challenges in 1031 Exchanges?

One major challenge is the strict timelines the IRS sets for identifying new properties. After you sell your old property, you have only 45 days to put potential replacement properties in writing. This is usually very difficult, especially in very competitive markets. Missing this deadline means that you have to pay capital gains taxes. Another challenge is the 180-day limit to complete the purchase of the new property.

As previously stated, this time includes both the first 45 days for identifying replacement properties, so you generally have about four and a half months to finish the transaction. When there are delays with financing, inspections, or completing the necessary paperwork, this can affect an investor’s ability to meet these deadlines. Paperwork and rules can also be complicated. Improper documentation or mistakes when filing your tax return can draw unwanted attention from the IRS or disqualify your exchange.

Valuing the properties is another major issue. It can be challenging to find a replacement that is equal to or greater in value than the property sold. Choosing a lesser-value property could lead to tax consequences. To overcome these challenges, ensure to work with an experienced Qualified Intermediary.

This is important because they can help you manage deadlines, prepare the necessary documents, and guide you through the exchange process correctly. Another way to reduce stress is to look for replacement properties before even selling your old property. Endeavor to keep all paperwork organized, including contracts and closing statements

What Are Best Practices for Successful 1031 Exchanges?

One of the most important tips is to plan your exchange in advance. Do not wait until you sell your investment property before thinking about the next step to take. Start looking for possible replacement properties early and review financing options. Planning early gives you more choices and reduces the pressure of the 45-day identification deadline.

It is also important to consult with tax professionals regularly. A tax advisor can help you understand the impact of your capital gains taxes and how they align with your overall investment goals. Another best practice is to carefully select a reliable Qualified Intermediary. This person or company plays a key role in holding your sale proceeds, preparing exchange documents, and facilitating the entire exchange.

Your 1031 Exchange Journey Begins Here

A 1031 exchange is a tax-deferred strategy that allows real estate investors to sell and buy replacement properties while deferring capital gains taxes. However, as beneficial as this tool is, navigating its complexities can be daunting. That is why you need the right knowledge and proper legal guidance in order to stay compliant with IRS rules and avoid mistakes that could invalidate the exchange.

At Universal Pacific 1031 Exchange, we help real estate investors execute smooth and compliant exchanges from the initial process to the end. Our team of experienced Intermediaries is well-equipped to handle the sale proceeds, prepare the required exchange documents, and guide you through each step so your transaction meets the IRS requirements. Reach out to us today to start an exchange.

Frequently Asked Questions

Below are commonly asked questions about the 1031 exchange requirements and their respective answers.

What Are the Time Limits for a 1031 Exchange?

A 1031 exchange has very strict deadlines. After you sell your investment property, you have 45 days to identify your replacement property in writing. This means you must clearly list the property or properties you may buy. You then have 180 days from the date of the sale to complete the purchase of the new property. The 180 days include the first 45 days. If you miss either deadline, the exchange will not qualify, and you may have to pay capital gains taxes.

Can I Do a 1031 Exchange With a Property That Is Not My Primary Residence?

Yes, but the property must be held for investment or business use. A primary residence does not qualify for a 1031 exchange. The property must be real estate used for rental income, business, or long-term investment. Property used mainly for personal use, such as a family home, usually does not qualify. In short, the property must be an investment property, not your main home.

What Are the Benefits of a 1031 Exchange?

The biggest benefit of a 1031 exchange is that it allows you to defer capital gains taxes when you sell an investment property. Instead of paying taxes right away, you can reinvest the full sale proceeds into another property.

This helps you grow your investment faster because more of your money stays working for you. It can also improve cash flow if you move into a higher-income property. Over time, investors can build more wealth by using this strategy.

Do I Need a Qualified Intermediary for a 1031 Exchange?

Yes. You need a Qualified Intermediary to complete a 1031 exchange. The Qualified Intermediary holds the money from the sale of your property and uses it to buy the replacement property. If you receive the money directly, the exchange becomes taxable. This is why choosing a reliable and experienced intermediary is very important.

Are There Any Restrictions on the Types of Properties that Can Be Exchanged in a 1031 Exchange?

Yes, there are restrictions. The exchange must involve real property that is held for investment or business use. The properties must be like-kind, which usually means both are real estate used for investment. For example, you can exchange a rental home for commercial property or raw land. However, personal property such as cars or equipment does not qualify. Your primary residence also does not qualify.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.