1031 Exchange Rules in Florida

Florida is one of the best states for conducting 1031 exchanges because of its relaxed real estate investment rules, especially the absence of state income tax. However, it has a documentary stamp tax that is imposed on any replacement property acquired during such transactions.

Despite the ease of doing business in the state, most realtors have seen their exchanges disqualified for simple, avoidable mistakes. As such, the success of your tax-deferred exchange depends a lot on the competence and experience of the Qualified Intermediary you choose to work with.

At Universal Pacific 1031 Exchange, we help investors navigate complex exchanges with clarity and confidence while deferring their capital gains taxes. With 35+ years of professional experience, we offer one of the most trusted Qualified Intermediary (QI) services in Florida. Contact us for a free consultation today.

This comprehensive guide gives a detailed breakdown of the 1031 exchange rules in Florida and how to navigate them. It also covers the types of 1031 exchange structures that exist and a step-by-step process on how to carry out a like-kind exchange in Florida.

What Is a 1031 Exchange?

A 1031 exchange is a provision under Section 1031 of the IRC code that allows taxpayers to defer capital gains taxes on real estate by swapping one investment property for another like-kind property. This strategy allows you to reinvest the proceeds from the sale of one property into another without incurring immediate taxes.

These capital gains taxes stay deferred until the new property is finally sold with the intent to cash out. The 1031 exchange is a valuable tool that has proved resourceful for most Florida investors seeking to build their portfolios and accumulate long-term wealth.

What Are the 1031 Exchange Rules in Florida?

Like every other U.S. state, Florida follows the same 1031 exchange procedures because the transactions are governed by federal law. Notably, Florida does not impose any state income tax on the exchange, making it especially favorable for investors.

That said, this is one of the major Florida-specific distinctions that investors should consider during such transactions:

Documentary Stamp Tax and Transfer Tax in Florida

Although Florida does not charge a state income tax, it imposes a documentary stamp tax on real estate transfers. The terms “documentary stamp tax” and “transfer tax” are often used interchangeably, referring to the same type of tax in Chapter 201 of the Florida Statutes.

Every real estate transfer, including those under the 1031 exchange, is subject to the state’s documentary stamp once the property deed is recorded. This tax applies regardless of whether it’s a simple sale or part of a complex exchange.

The rates aren’t fixed statewide; they can vary by county and are subject to change, so don’t assume yesterday’s rate still holds. Always double-check the current documentary stamp rate before closing the deal. However, it typically ranges from $0.35 – $0.70 per $100 spent on the property, depending on the nature of the transaction.

What Types of Properties Qualify for a 1031 Exchange in Florida?

Only like-kind property owners can qualify for 1031 exchanges. “Like-kind” doesn’t mean you have to swap an exact type of rental property for another, or a warehouse for an identical one. In the eyes of the IRS, it simply means business or investment properties of any sort.

Real properties involved include rental homes, apartment buildings, vacant land, hotels, a ranch with oil and gas royalties, and other types of commercial properties.

When performing a 1031 exchange in Florida, both the relinquished and replacement properties must meet this “like-kind” criteria. Even an exchange from commercial to residential is completely valid as long as both properties are held for investment purposes.

It is important to note that any property located outside the United States does not qualify as “like-kind”. Other excluded assets include partnership interests, certificates of trust, property held primarily for resale, primary residences, stocks, or REITs.

What Are the Identification Rules in a Florida 1031 Exchange?

There are three rules for identifying replacement properties in a 1031 exchange. You’re expected to work with one of them, depending on the peculiarity of your exchange. They include the following:

- The three-property rule allows you to identify up to three properties irrespective of their combined fair market value (FMV).

- Under the 200% rule, you can identify three investment properties whose total FMV must not exceed 200% of the relinquished property’s value.

- The 95% rule, which is the last option, allows you to identify multiple properties, regardless of their total value, on the condition that you acquire at least 95% of the total identified value. This is risky and rarely used, but it’s an option for high-volume, high-commitment exchanges.

You may also identify replacement properties of lesser value, but it can sometimes lead to “boot” or taxable gain for the portion not reinvested. Irrespective of any of the options you choose to work with, you must identify the property within the stipulated IRS timeline, as we will discuss in subsequent sections.

How Long Do I Have to Complete a 1031 Exchange in Florida?

After you have identified the right replacement property, you have a maximum of 180 days from the date of the property sale to pay for the new property and complete the exchange. This 180-day period includes the initial 45 days used for property identification and is not an additional time.

The timeline is quite strict, and you may not get an extension even if the deadline falls on a weekend or holiday. If you don’t close the deal on or before the 180th day, the exchange will be disqualified, making the gain taxable.

Can I Do a 1031 Exchange Between Florida and Another State?

Yes, you can perform an interstate 1031 exchange as long as it meets all the Internal Revenue Service requirements. 1031 exchanges are governed by the federal tax code. Hence, they are not limited by state lines. However, both assets must be investment or business properties, and you must meet all IRS requirements.

Although Florida has no state income tax, the other states involved might. States like California will use their Clawback Provision to tax the gain later, even if you later conduct another out-of-state tax-deferred exchange. Be aware of state-level tax rules in both locations to avoid any unnecessary surprises.

Do I Have to Use a Qualified Intermediary (QI) in Florida?

Yes, hiring a Qualified Intermediary (QI) is mandatory when carrying out a 1031 exchange, whether you’re in Florida or anywhere else. The QI is not just there to guide you through the process, but is also responsible for holding the realized funds from sold property.

The QI will also prepare the exchange documents to ensure compliance and use the sale proceeds to purchase the replacement property on your behalf. This is important because you’re not allowed to touch the funds, even if briefly, as this could disqualify the entire exchange process and incur taxable consequences.

So, keep in mind that no QI is equal to no valid exchange. However, not just anyone can serve as your QI. Any attorney, real estate agent, or financial advisor who has represented you within the last two years is disqualified under IRS rules.

Because the QI is the one who handles your funds and ensures your transaction remains IRS compliant, finding the right one is critical. At Universal Pacific 1031 Exchange, we’ve facilitated hundreds of compliant exchanges nationwide, including Florida and interstate deals.

Our team of experts is dedicated to ensuring that your exchange process flows seamlessly while staying IRS-compliant. Contact us now for a free consultation.

Does the Taxpayer Name Have to Stay the Same in a 1031 Exchange?

Yes, the IRS requires that the same taxpayer name appear on the title of the relinquished and replacement properties. In simple terms, the entity that sells must also be the one that buys. This rule ensures consistency and validates that the exchange is being carried out by a single tax-paying party.

However, there is an exception for disregarded entities. For example, if a property is owned by a single-member LLC, the IRS treats it as the same taxpayer as the individual owner. So, if your property is held in a single-member LLC, and you’re the sole owner, you can still execute a 1031 exchange without breaking the “same taxpayer” rule.

When multiple owners, partnerships, or LLCs with multiple members are involved, it gets more complex. Although you can still complete an exchange as a group, each member must be in full support of the transaction to avoid violating the taxpayer identity rule.

Are Vacation Homes in Florida Eligible for a 1031 Exchange?

Yes, vacation homes in Florida are eligible for a 1031 exchange provided they are held for business, investment, or other commercial purposes. The vacation home must also adhere to the safe harbor rule.

It states that you must rent the property at fair market price for at least 14 days per year for two consecutive years before the exchange. Also, during those same years, your personal use of the property must not exceed the greater of 14 days or 10% of the total days it’s rented.

Failure to comply with this rule could result in the IRS disqualifying the exchange on the basis that the vacation home is personal property. Keep in mind that you must also own the replacement property for at least two years before selling.

What Happens If I Receive Cash or “Boot” in the Exchange?

Boot in a 1031 exchange refers to anything you receive that isn’t like-kind property, usually cash, but it can also be mortgage relief or other non-qualifying benefits. Under the IRS code, a boot is considered a taxable gain.

For instance, if you’re left with cash after an exchange, it means that all the proceeds from the old property were not reinvested. In that case, you’ll have to pay capital gains tax immediately on the amount of money remaining.

In the same vein, if you buy a replacement asset at a lower price than the relinquished property, the leftover amount is considered boot and so taxable. This includes any cash left in escrow or debt not replaced on the new property.

Note that the presence of a boot does not disqualify your 1031 exchange; it only triggers immediate taxes on the portion you didn’t fully reinvest.

How Does a Florida 1031 Exchange Work?

A 1031 exchange lets you sell your investment property, reinvest the proceeds, and defer capital gains tax legally. By deferring taxes, you keep more capital in motion, which means bigger deals, better locations, and compounding wealth. Every dollar not lost to taxes is a dollar working for your future portfolio.

One good thing in all these is that Florida has no state income tax, so while the IRS defers your federal capital gains, Florida takes exactly nothing off the top. This constitutes a serious edge over states like California or New York, where state taxes bite into your exchange.

Moreover, Florida’s market diversity, which includes residential, commercial, mixed-use, and raw land, makes executing a 1031 exchange more flexible and powerful. Due to all these benefits, Florida has seen a consistent demand from investors. In addition, migration and tourism trends have kept rents quite high in Florida.

However, keep in mind that in some Florida counties, title companies handle closings, while in others, real estate attorneys are required. Either way, as discussed earlier, your QI must coordinate precisely with local professionals to ensure funds are held and transferred correctly without triggering constructive receipt, which could disqualify the exchange.

Although Florida does not require state-specific 1031 forms, your QI should still prepare customized, compliant documentation that aligns with Florida closing practices. In summary, endeavor to work with professionals who know Florida inside and out.

Which Types of Properties Make Good Investments in Florida?

Florida offers a wide range of real estate property types that are suitable for a 1031 exchange if they are held for business or investment purposes. Vacation rentals near hotspots like Orlando or Miami can generate strong short-term income, though they come with more management demands.

On the other hand, multi-family properties like duplexes and triplexes often provide steady, long-term cash flow with less volatility. Commercial options such as office spaces, retail storefronts, and even self-storage facilities can be solid choices too.

Other great options for real estate investing in Florida are raw land or mobile home parks with strong long-term appreciation prospects. The major consideration as far as 1031 tax deferral under the tax regulations is concerned, is that you must prove you’re buying them with investment objectives in mind.

Common Types of 1031 Exchanges in Florida

When conducting a 1031 exchange in Florida, there are four major structures you can use. They include: delayed exchange, simultaneous exchange, reverse exchange, and construction/improvement exchange.

Delayed Exchange

Delayed exchange is recognized as the most common of the four. This type of exchange follows the normal procedure of identifying potential replacement property within 45 days and closing the exchange by the end of 180 days. It is used by most real estate investors due to its flexible and relatively straightforward nature.

Simultaneous Exchange

This type of exchange is rarely used. In a simultaneous exchange, both properties are closed at the same time. This simply means that the sale of the relinquished property and the purchase of the replacement happen on the same day.

This method requires precise coordination, and it’s quite prone to mistakes. It’s less common but can work well for private deals or closely aligned transactions.

Reverse Exchange

A reverse 1031 exchange rule is the direct opposite of a delayed exchange. It is mostly used by real estate investors who are seeking to buy the replacement property first before selling the relinquished property.

It is more complex and requires a special holding arrangement called an Exchange Accommodation Titleholder (EAT). This method is especially useful in Florida’s highly competitive market, where waiting to buy might mean missing out altogether.

Construction or Improvement Exchange (Build-to-Suit)

This type of exchange allows you to use your exchange funds to build or improve the replacement property. The tricky part here is that every improvement must be finished and reflected in all the property’s value before the 180 days are up.

It is especially useful in areas like Sarasota or St. Pete, where investors may want to renovate older buildings or develop new ones.

How to Start a 1031 Exchange in Florida

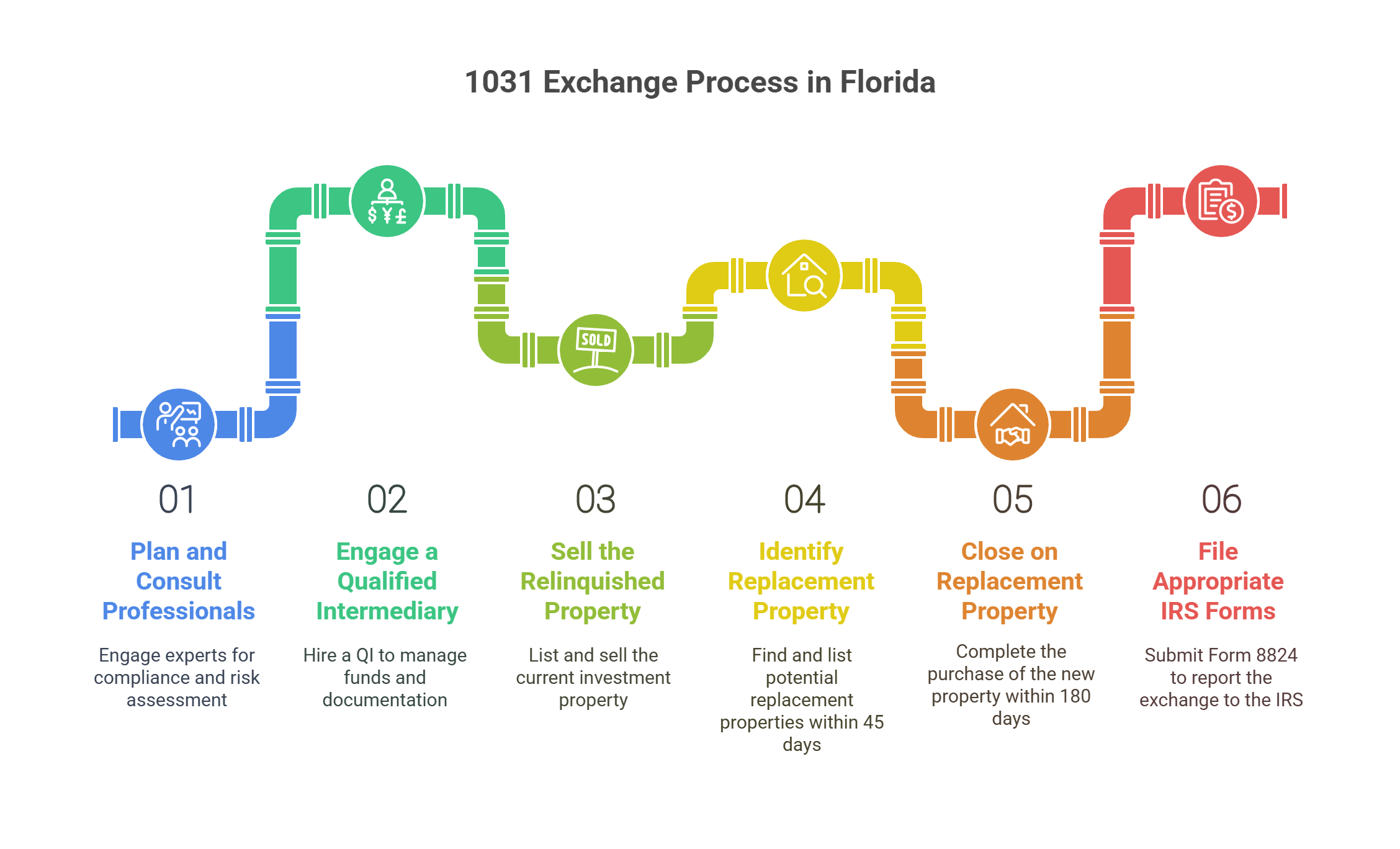

While executing a seamless 1031 exchange might prove burdensome, here is a step-by-step guide on how to navigate the entire process.

1. Plan and Consult Professionals

Before conducting a 1031 exchange in Florida, it is important to first consult professionals such as tax advisors, Certified Public Accountants (CPAs), real estate attorneys, and other experts in the Florida real estate landscape.

These professionals ensure the exchange complies with IRS rules, assist in navigating Florida-specific regulations, and spot potential risks before they become costly mistakes.

2. Engage a Qualified Intermediary

The next step is to engage a Qualified Intermediary. As earlier stated, an exchange cannot be considered valid without the participation of a QI. A QI holds the proceeds from the sale of your relinquished property, prepares the necessary documentation, and ensures you never take constructive receipt of the funds. Choosing the right QI is crucial, not just for compliance, but for peace of mind throughout the process.

3. Sell the Relinquished Property

After you have hired a competent QI, you can proceed to list your current investment property for sale. Once a buyer comes along, ensure the sales contract states that the transaction is intended to be part of a 1031 exchange.

This alerts all parties, especially the title and escrow, that the process must follow the IRS guidelines. Your QI will then step in to coordinate the paperwork and hold the proceeds in escrow, keeping everything compliant and on track.

4. Identify Replacement Property Within 45 days

Endeavor to comply with the IRS identification rules when searching for a replacement property. As discussed earlier, this rule mandates you to identify the potential replacement property(ies) within 45 days after the sale of the original property.

Then, formally record them in writing and submit the list to your QI within the 45-day deadline. Be sure to include key details such as street address, city, and a clear, identifiable description of each property.

5. Close on Replacement Property Within 180 Days

After identifying the replacement property, you must close the deal on the new property within 180 days. This 180-day timeline started counting from the date you disposed of the old property.

This deadline is strict, irrespective of whether the 180th day is Christmas or any other national holiday. Missing it could disqualify the entire exchange, triggering a full tax liability. Plan properly and ensure your QI and closing team are fully aligned.

6. File Appropriate IRS Forms (Form 8824)

You can’t just carry out a 1031 exchange without informing the IRS. Hence, you will be required to report the exchange using Form 8824. The form contains a description of both the relinquished and replacement properties and key dates in the transaction, including when you identified and transferred the properties.

It also captures the fair market values of the properties involved in the exchange and the calculation of any capital gain that was deferred. Filing it out accurately is crucial, so consider passing it through a tax professional or CPA. Mistakes can trigger audits or unexpected tax bills.

Ready to Start Your 1031 Exchange in Florida?

Navigating through the process of a 1031 exchange can prove both worrisome and taxing at the same time. From keeping up with the IRS’s strict deadlines and nuanced rules to having the proper documentation, it’s easy to feel overwhelmed–or worse, make a costly mistake. That’s where Universal Pacific 1031 Exchange steps in.

As a leading Qualified Intermediary in Miami and beyond, Universal Pacific 1031 Exchange helps investors confidently complete their exchanges from start to finish. We safeguard your funds, prepare IRS-compliant documents, ensure you meet critical timeframes, and guide you through each step with clarity and precision. You can contact us for a free consultation or visit our 1031 exchange office to start an exchange today.

FAQs

How Much Property Must I Acquire in an Exchange?

The number of properties to acquire in a 1031 exchange depends on the identification rule you choose to work with. The three rules are:

- You can use the 3-property rule to identify one to three properties notwithstanding their total FMV, as long as it has an equal or greater value than the original property.

- The 200% rule is for identifying only three properties, provided that their FMV doesn’t exceed 200% of the relinquished asset.

- The 95% rule allows you to identify more than three properties as long as you purchase up to 95% of their combined value.

What’s the Best Time of Year to Perform an Exchange in Florida?

There is no perfect time to start a 1031 exchange, but certain seasons offer strategic advantages, most especially in Florida. It is advisable to begin early in the year, preferably winter or spring, so you have more flexibility with the 180-day window and tax deadlines.

Can I Live in a 1031 Exchange Property in Florida?

Not immediately. Moving into a 1031 exchange property suggests to the IRS that you didn’t purchase the property for the investment process. It will void the transaction and open you up to immediate tax liabilities.

However, you can convert the property to a primary residence after two years of renting it out and collecting rent. During these two years, you may use the apartment for a maximum of 14 days per year or 10% of the total days it was rented out.

What Happens If I Miss a Deadline?

Missing a 1031 exchange deadline automatically disqualifies the exchange. This means that the IRS treats it as a taxable sale, and you’ll have to pay immediate capital gains taxes on the profit from the relinquished property. So, be sure to stick to the IRS timelines to avoid taxable events.

How Does Depreciation Recapture Work?

Depreciation recapture happens when you sell a property and the IRS “recaptures” the tax benefits you got from the depreciation deductions. It is taxed up to 25% on the portion you’ve written off. A full 1031 exchange defers it, but if the exchange fails or boot becomes involved, the IRS will come for a share.

Can I Do Multiple 1031 Exchanges?

Yes, you can do multiple 1031 exchanges; there’s no limit. As long as each one follows IRS rules, you can keep deferring taxes and rolling gains into new properties indefinitely.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.