Can You 1031 Exchange Multiple Properties Into One?

You bought rentals one at a time over twenty years, and now you own six smaller properties scattered across two counties. Each one needs a roof, a tenant call at 11 p.m., and its own set of books. Consolidating those several properties into one larger property through a 1031 exchange is one of the cleanest ways to reduce management drag without writing a check to the IRS. The mechanics are straightforward once you understand aggregation under Internal Revenue Code (IRC) Section 1031.

At Universal Pacific 1031 Exchange, we structure multi-property 1031 exchanges for real estate investors ready to trade portfolio sprawl for a single, higher-quality asset. Our team coordinates the identification windows, qualified intermediary controls, and replacement property timing so the exchange holds up under IRS scrutiny. Schedule a consultation with our team before you list anything.

This article explores the benefits of consolidating multiple properties, basic steps to successfully exchange multiple properties into one, and specific rules to consider when carrying out a multiple-property transaction.

Understanding the 1031 Exchange Process

A 1031 exchange is a tax-deferred swap of real property held for productive use in a trade, business, or investment. The relinquished property (the one you sell) and the replacement property (the one you buy) must both be held for investment or business use. Tax is deferred, not eliminated. The deferred gain rolls into the basis (your tax cost in the property for future calculations) of the replacement property and becomes taxable if and when that property is later sold without another exchange.

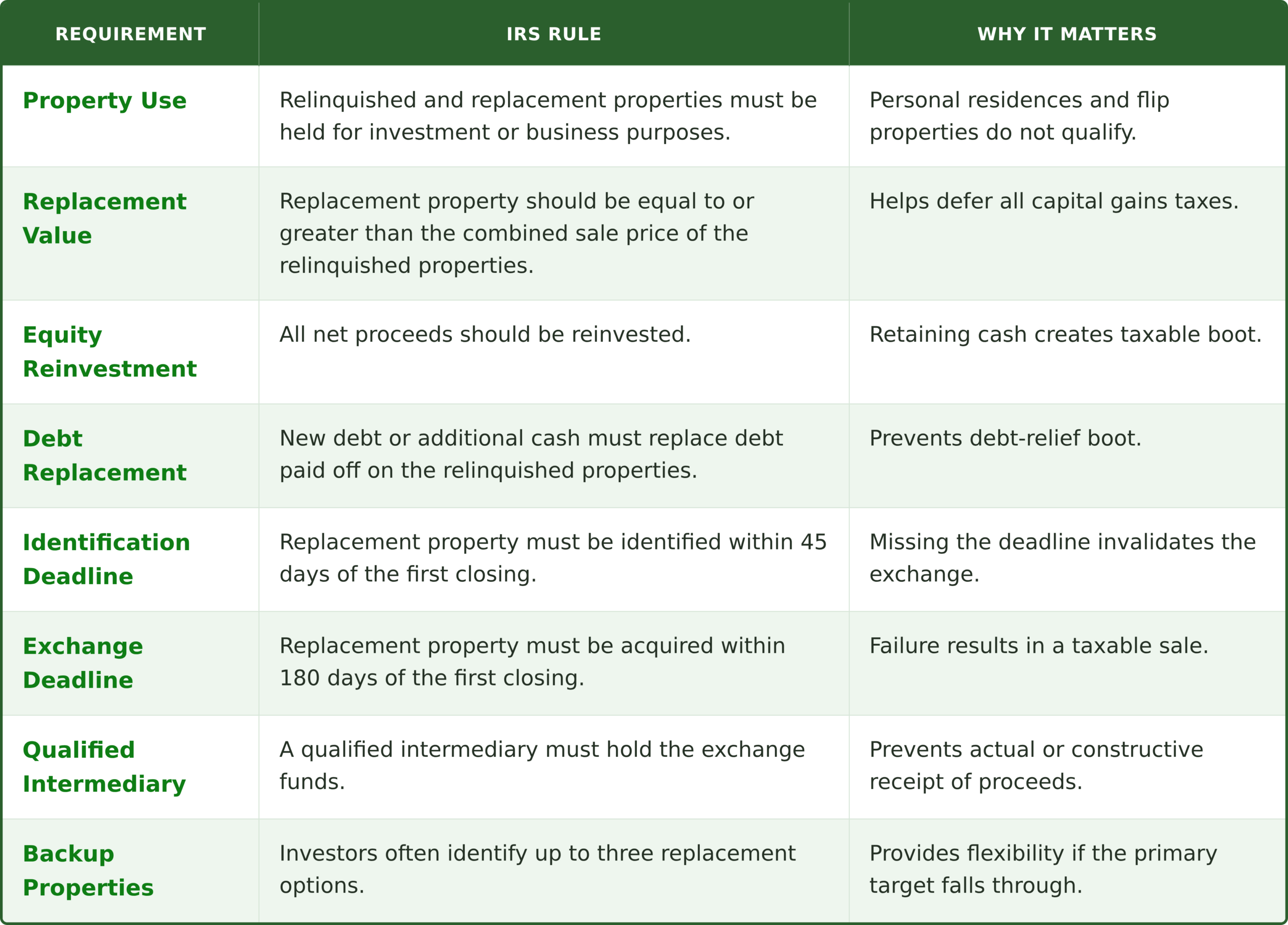

For real estate, the like-kind standard is broad. Raw land, a multifamily building, an industrial warehouse, a retail strip, and a single-family rental are all like-kind to each other. What matters is the character of the property, not its grade or class. You cannot exchange a primary residence or property held primarily for sale (a flip) under Section 1031.

Two deadlines control every exchange. From the date the first property closes, you have 45 days to identify replacement properties in writing, and 180 days to acquire one or more of the identified targets. Miss either clock and the exchange dies. Both periods start the same day, both fall on calendar days (not business days), and neither can be extended except in narrow federally declared disaster situations. One important wrinkle under IRC Section 1031(a)(3)(B): the 180-day clock is actually the earlier of 180 days or the due date (with extensions) of your federal tax return for the year of the sale, so a fourth-quarter closing can shorten the exchange timeline if you do not file an extension.

Key Benefits for Real Estate Investors

The major benefit of a 1031 exchange is tax deferral. The practical benefits run deeper: compounding equity that would otherwise be siphoned by tax, the ability to upgrade from management-intensive assets to passive ones, and the option to reposition geographically. According to the EY 2021 Macroeconomic Study commissioned by the 1031 industry coalition, like-kind exchanges supported 976,000 jobs and contributed $97.4 billion in value-added to U.S. GDP. That is a measure of how widely investors rely on the tool.

Can You 1031 Exchange Multiple Properties Into One?

Yes. Treas. Reg. 1.1031(j)-1 lays out the rules for exchanges of multiple properties, and Treas. Reg. 1.1031(k)-1 governs the deferred exchange mechanics that make consolidation possible. An investor can sell two properties, five properties, or an entire portfolio of relinquished properties and acquire a single replacement property, provided the standard identification period, valuation, and timing rules are satisfied.

The most common scenario is an investor with several aging rentals who wants to step up to one larger property such as a small multifamily building, a triple-net retail asset, or a self-storage facility. Aggregation pools the cash and debt from every property you sell. That single pool funds the one property you buy. The equal-or-greater-value rule still applies: the replacement purchase price must meet or exceed the combined net sale price of the relinquished properties, and the equity and debt levels must also be met. Any shortfall generates taxable boot.

Timing is where multi-property exchanges get tactically important. The 45-day identification period and the 180-day exchange period (or the tax-return due date, whichever runs first) are both measured from the closing of the first property in the relinquished group. If the second relinquished property has not closed by day 45, the investor must still identify the replacement property by that deadline. This is the central planning constraint when relinquished properties close on staggered dates.

Key Requirements for Exchanging Multiple Properties Into One

Benefits of Consolidating Multiple Properties

The decision to consolidate multiple properties into one larger property through a 1031 exchange delivers benefits beyond tax deferral. Property management simplifies dramatically when six leases, six tax bills, and six insurance policies collapse into one. Cash flow often improves because larger institutional-grade assets carry better cap rates, more predictable tenants, and lower per-unit operating costs.

Tax reporting also gets cleaner. Instead of tracking depreciation schedules and capital improvements across several properties, you maintain one set of books on a single property. Investors frequently use consolidation to upgrade asset class, moving from tired single-family rentals into a stabilized apartment building, a medical office, or a net-leased property. Compliance overhead, inspection cycles, and lender reporting all shrink. For investors approaching retirement, that simplification is often worth as much as the tax savings.

If consolidation could simplify your portfolio, request a 30-minute structural review with Universal Pacific before you list your first property.

Steps to Successfully Exchange Multiple Properties Into One

A multi-property exchange is built on a sequence of decisions and documents that must be lined up before the first sale closes. The four steps below cover the core procedural arc that every consolidation exchange follows.

1. Identify Eligible Properties

Begin with a clean inventory of the properties you intend to sell. Confirm each has been held for investment or business use, not flipped or used as a primary residence. Pull current appraised values, payoff amounts on existing debt, and a depreciation schedule for each relinquished property so you can calculate combined equity and debt that must be replaced. This step also includes a conversation with your CPA about deferred gain exposure.

2. Engage a Qualified Intermediary

Before the first sale closes, you must engage a qualified intermediary to hold the sale proceeds in a segregated exchange account. The qualified intermediary safe harbor is found in Treas. Reg. 1.1031(k)-1(g)(4). It establishes a set of conditions that, if satisfied, prevent the IRS from treating you as having received the exchange proceeds.

In addition, the disqualified-person rule in Treas. Reg. 1.1031(k)-1(k) restricts certain individuals from serving as your qualified intermediary. This rule generally bars anyone who has acted as your attorney, CPA, real estate broker, or employee during the two-year period ending on the date of the exchange.

A long-prior relationship can be acceptable; a current or recent one is not. The intermediary prepares the exchange agreement, assignment documents, and direct deeding instructions, and provides the security service that protects funds from constructive receipt. Choosing an intermediary with bonding, segregated accounts, audited controls, and Federation of Exchange Accommodators membership is the single biggest risk decision in the exchange.

3. Identify Replacement Property

Within 45 days of the first relinquished property’s closing, you must identify the replacement property in writing and deliver that identification to the qualified intermediary. The identification must be unambiguous, listing the address or legal description of the target property. Most investors consolidating multiple properties use the three-property rule and name one to three candidate replacement properties to give themselves a fallback if the first choice falls through.

4. Complete the Exchange

Close on the replacement property within 180 days of the first relinquished property’s sale. The qualified intermediary wires the proceeds from the exchange account directly to the closing, the deed flows to the investor, and any leftover cash becomes taxable boot. Once the exchange is completed, your CPA files Form 8824 with your federal return for the year of the exchange, reporting the deferred gain and the basis carryover. Per the IRS instructions, Form 8824 is required for every tax year in which a like-kind exchange occurs.

Rules and Considerations for Combining Multiple Properties

The IRS aggregation rules under Treas. Reg. 1.1031(j)-1 allow multiple relinquished properties and multiple replacement properties to be treated as a combined exchange when the regulatory requirements are met. Three tests sit at the foundation. The replacement purchase price must equal or exceed the combined sale price of the relinquished properties, net of allowable transactional costs.

Your equity in the replacement must equal or exceed the combined equity from the relinquished group. And the debt you take on the replacement must equal or exceed the debt paid off on the relinquished group, unless you make up any shortfall with new cash. If you paid off $400,000 of mortgage debt on the relinquished group, you need at least $400,000 of new debt or additional cash on the replacement to avoid debt-relief boot.

The three identification rules under Treas. Reg. 1.1031(k)-1(c)(4) are essential for executing multi-property exchanges. The three-property rule lets you identify up to three potential replacement properties regardless of value. The 200% rule lets you identify any number of properties as long as their combined fair market value does not exceed 200% of the combined sale price of the relinquished properties. The 95% rule lets you identify any number of properties of any value, but you must actually acquire at least 95% of the aggregate identified fair market value (measured by FMV, not by property count), or the entire exchange fails.

Throughout the identification and exchange periods, the qualified intermediary holds the proceeds in an exchange account insulated from the investor’s reach. That security service is what preserves the safe harbor. If the investor has actual or constructive receipt of the funds at any point, the exchange collapses, and immediate tax liabilities attach to the full gain. Any cash that exceeds the cost of the replacement property at closing is returned to the investor as cash boot and is taxable in the year of the exchange.

Common Pitfalls and How to Avoid Them

The most common failure mode is missing the 45-day deadline. Investors get distracted, negotiations slip, and identification letters arrive late. Identify replacement candidates before the first sale closes. According to Michael Bergman, President & CEO of Universal Pacific, “The key to a successful multi-property exchange is planning before the first sale closes.”

A close second is identifying too few replacement properties, which leaves the exchange with no backup if the primary target falls out of contract. Naming three properties under the three-property rule costs nothing and provides flexibility.

Debt replacement mismatch is another frequent trap. Investors fixate on cash and forget that paid-off debt counts as boot (taxable cash or relief from debt that the IRS treats as gain) if it is not replaced with new debt or additional cash investment. Equally damaging is choosing a non-independent intermediary, such as the investor’s longtime attorney or accountant. That kind of relationship makes the intermediary a disqualified person and, in turn, disqualifies the entire exchange.

Attempting to exchange a primary residence, a vacation home used primarily for personal enjoyment, or a flip property held for resale is a clean disqualification. Section 1031 applies only to property held for productive use in a trade or business or for investment. Finally, missing the 180-day completion deadline, often because replacement financing hits an underwriting snag, ends the exchange.

Build margin into your financing timeline and confirm the lender understands the 1031 exchange timing rules. Avoid the 45-day and debt-replacement traps. Schedule a pre-listing planning call with Universal Pacific to model the math before you commit to any sale.

Case Studies: Successful 1031 Exchanges of Multiple Properties

The following are illustrative scenarios drawn from common multi-property consolidation fact patterns. They are not specific Universal Pacific client transactions, and dollar figures in each example are presented only to demonstrate the mechanics.

Consider an investor who owns three single-family rentals worth roughly $400,000 each, with combined mortgage debt of $300,000. The investor sells all three over a 60-day window, with the first property closing March 1 and the second relinquished property closing April 10.

The 45-day identification deadline runs from March 1, so the investor identifies a $1.3 million eight-unit apartment building before April 15 and closes by late August. Combined equity of $900,000 is reinvested, $400,000 of new debt funds the rest of the purchase, and the deferred gain rolls into a single replacement property with a clean depreciation schedule.

A second scenario involves an investor consolidating five small retail condos into one larger retail center. Because closings are staggered, the investor uses the 200% rule to identify multiple potential replacement properties whose aggregate value does not exceed 200% of the combined sale price.

A third scenario is a reverse exchange, governed by IRS Revenue Procedure 2000-37. In a reverse exchange, the investor acquires the replacement property first through an exchange accommodation titleholder (a special-purpose entity that holds title temporarily), then sells the multiple relinquished properties within the 180-day window. Reverse exchanges are useful when the right replacement property surfaces before the existing portfolio sells.

Some investors who want fully passive consolidation also direct their proceeds into a Delaware Statutory Trust (DST), a fractional interest in institutional real estate that the IRS treats as like-kind under Revenue Ruling 2004-86. The Federation of Exchange Accommodators tracks growth in these structures. Research cited by 1031buildsamerica.org shows like-kind exchanges rose roughly 15% from 2019 to 2023 even as overall real estate transactions fell more than 22%.

Are You Ready to Simplify Your Portfolio With a 1031 Exchange?

Consolidating multiple properties into a single replacement property is fully supported under IRC Section 1031 when the identification, timing, equity, and debt rules are respected. The benefits, including simplified property management, improved cash flow, and asset-class upgrades, often outweigh the planning effort.

The risks of a missed deadline, a non-independent intermediary, or a debt mismatch are recoverable only with careful structuring up front. Universal Pacific helps investors map that sequence and complete the exchange on time.

Universal Pacific 1031 Exchange has over 30 years of experience in helping real estate investors navigate the complexities of a 1031 exchange. Our team structures multi-property 1031 exchanges regularly and coordinates with qualified intermediaries, real estate counsel, and CPAs to keep every deadline and every dollar of equity inside the safe harbor. Book a call with us today to start an exchange.

FAQ

Below are answers to common questions about exchanging multiple properties into one.

Can You 1031 Exchange Multiple Properties Into One?

Yes. A 1031 exchange allows you to sell multiple investment or business-use properties and use the proceeds to acquire a single replacement property. This strategy is often used by investors who want to simplify their portfolios, reduce management responsibilities, or move into a larger asset. To defer all eligible capital gains taxes, the replacement property generally must have a purchase price equal to or greater than the combined value of the relinquished properties, and all exchange requirements must be satisfied.

Is There a Limit to the Number of Properties You Can Exchange Into One in a 1031 Exchange?

No. The IRS does not impose a specific limit on the number of relinquished properties that can be exchanged into a single replacement property. Investors can combine several investment properties into one larger asset, provided the exchange follows IRS rules, including identification deadlines, reinvestment requirements, and like-kind standards.

What Are the Advantages of Exchanging Multiple Properties Into One in a 1031 Exchange?

Consolidating multiple properties into a single replacement property can provide several benefits. It may reduce management responsibilities, lower operating costs, and simplify recordkeeping. Investors may also gain access to larger or higher-performing assets that generate stronger cash flow and long-term appreciation potential. In some cases, consolidation can improve portfolio efficiency and make estate or succession planning easier.

Are There Any Specific Rules or Requirements for Exchanging Multiple Properties Into One in a 1031 Exchange?

Yes. The same IRS rules that apply to other 1031 exchanges also apply when combining multiple properties into one. The replacement property must generally be identified within 45 days of transferring the relinquished properties, and the acquisition must be completed within 180 days. To maximize tax deferral, the investor typically must reinvest all exchange proceeds and acquire replacement property of equal or greater value. Working with a qualified intermediary is also required to maintain compliance with exchange regulations.

Can I Exchange Properties of Different Types Into One in a 1031 Exchange?

Yes. Under current IRS rules, most real property held for investment or business purposes is considered like-kind to other qualifying real property. This means you may be able to exchange different property types, such as residential rental properties, commercial buildings, industrial properties, or vacant land, into a single replacement property. However, all properties involved must be held for investment or productive use in a trade or business, and personal residences generally do not qualify for 1031 exchange treatment.

Disclaimer: The content above is provided for general informational purposes only and does not constitute legal, tax, or investment advice. Tax outcomes from a 1031 exchange depend on the specific facts of each transaction and the application of current IRS regulations. Universal Pacific does not provide legal or tax opinions, and reading this content does not create a client relationship. Consult a qualified tax advisor and licensed attorney before initiating any 1031 exchange.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.