Essential Compliance for 1031 Exchange Inherited Property

Executing a successful 1031 exchange on inherited property can be complex. The process comes with strict timelines and requirements, and even a little mistake can lead to taxable consequences.

It becomes even more difficult when the property is owned by many heirs or more than one family member with varying opinions. Working with a Qualified Intermediary can eliminate the uncertainty and fear that comes with like-kind exchanges and ensure that the transaction remains tax-deferred.

Universal Pacific 1031 Exchange has 35+ years of experience in handling even the most complex of exchanges across the 50 US states. We work closely with investors, families, and professionals, to guide each step of the process with clarity and ease. Contact us today to get started.

This article explores the benefit of a 1031 exchange on Inherited property, the rules guiding the exchange, and common challenges most heirs face during the transaction.

What Is 1031 Exchange Inherited Property?

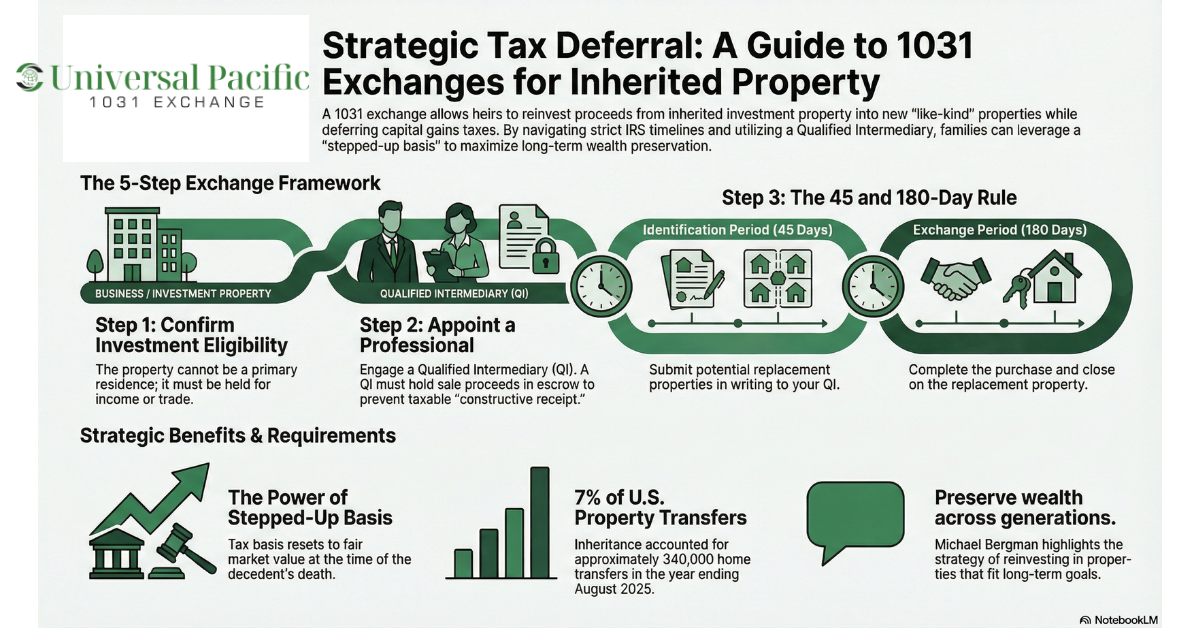

A 1031 exchange inherited property situation happens when someone inherits real estate and later decides to use a 1031 exchange to defer capital gains taxes instead of selling the property and paying taxes immediately. In the 12 months ending August 2025, an estimated 340,000 homes in the United States were transferred to heirs through inheritance, and for the first time these transfers made up about 7 % of all U.S. property transfers.

When an individual receives inherited property after a decedent’s death, the property receives a stepped-up basis. This step up in basis simply means the tax basis is adjusted to the property’s fair market value at the time of death and not the original purchase price. Due to this step up, if the property sells shortly after inheritance at its current fair market value, there usually will be little to no taxable gain.

However, if the inherited real estate increases in value over time, capital gains liability may come up, and that is when a 1031 exchange can become a useful tax-deferral strategy. For an inherited property to qualify for a like-kind exchange, it must meet the IRS regulations. One major requirement is that both the old property and the replacement property must be held for investment purposes or used in a trade or business.

For example, a rental property that produces rental income can qualify, as well as other types of real property held for real estate investments. Personal properties such as primary residences do not qualify, and vacation homes often face certain limits depending on how they are used.

How Does a 1031 Exchange Inherited Property Work?

A 1031 exchange involving inherited properties is usually complex to execute. This is because, like every other type of exchange, the IRS outlines strict rules by which an exchange can be considered valid for tax-deferral. Below is a step-by-step framework on how a 1031 exchange for inherited properties actually works.

Step 1: Confirm that the Property Qualifies as an Investment Property

The first step to performing a 1031 exchange is to ensure that both the inherited property and replacement property qualify as investment property under the IRS regulations. As mentioned earlier, both properties must be held for business or investment purposes and not for personal use. Using non-like-kind properties can cause the exchange to fail.

Step 2: Engage a Qualified Intermediary

This step is essential if the exchange will be considered valid in the eyes of the IRS. A Qualified Intermediary is a neutral third party who is responsible for holding sale proceeds in escrow accounts and facilitating the entire exchange. The Internal Revenue Service does not allow the seller of the inherited property to receive the exchange funds directly. Taking direct possession of sale proceeds could lead to what is called “constructive receipt”, which the IRS views as taxable.

Step 3: Sell the Inherited Property

After confirming that the properties meet the IRS requirement of like-kind and engaging a Qualified Intermediary, the next step is to sell the inherited property. Because of the earlier step-up in basis, the potential capital gains liability is generally based on the appreciation that takes place after inheritance. It is important to keep track of those figures to determine the possible taxable gain and overall tax implications before moving into the new property.

Step 4: Identify Like-kind Replacement

After the sale of the original property, the IRS gives a 45-day identification period, during which you can identify potential replacement properties and submit them to your QI in writing. You can do this using any of the identification rules, such as the three-property rule, the 95% rule, and the 200% rule. Note that the replacement property must also be held for investment or business purposes to qualify for a like-kind exchange.

Step 5: Purchase the Replacement Property

The next step after identifying the replacement property is to purchase it and close the exchange. This must be done within 180 days after selling the original property. To maintain full tax deferment, the replacement property must be of equal or greater value than the property sold. In situations where there was debt on the old property, the new property must also carry equal or a greater amount of debt.

What Are the Benefits of a 1031 Exchange for Inherited Property?

One major benefit is the ability to defer capital gains taxes. By reinvesting the proceeds of one investment property into another like-kind property, heirs can successfully defer capital gains taxes, thereby preserving more of the proceeds for future investment. This strategy offers significant tax benefits, including helping to reduce estate taxes and inheritance taxes, depending on how the property is managed.

Another major advantage is continued investment growth. By reinvesting the money into a new property, heirs can continue earning income from rent or see the property increase in value over time. This keeps the money working for them and can help build long-term financial growth. Because heirs do not have to use part of their proceeds to cover capital gains taxes, this allows them to diversify their portfolio and support long-term wealth preservation. According to a quote from Michael Bergman:

“A 1031 exchange on inherited property allows heirs to defer capital gains taxes while strategically reinvesting in properties that fit their long-term goals. With careful planning and the right professional guidance, it’s possible to preserve wealth across generations.”

A 1031 exchange also gives flexibility. Heirs can choose a new property that fits their investment objectives better. For example, they might pick a property that is easier to manage, produces more income, or suits their long-term goals. This makes it easier to handle the property and use it in a way that works best for the family. There are also the estate planning advantages that a 1031 exchange gives.

This means that when inherited property is eventually passed from one generation to the next, the government allows the property’s value for tax purposes to be updated to its current market value at the time of that second inheritance. For example, imagine a parent inherits a property and later passes it to their child. The property may have increased in value since the original inheritance. When the child inherits it, the property could get a new “step up” in value, which becomes the new tax basis.

This means that if the child later sells the property, they would only pay taxes on any increase in value that happens after they inherited it, not on the gains that happened while the parent owned it. In simple terms, it’s like resetting the value of the property for taxes, so the family doesn’t have to pay taxes on all the growth that happened over multiple generations, but only on the growth after the latest inheritance.

What Challenges Are Common in 1031 Exchange with Inherited Property?

There are several challenges that can come up during a 1031 exchange for inherited properties. One major challenge is complying with the IRS rules. The government sets very strict rules that govern these exchanges, and if those rules are not followed judiciously, the exchange can be rejected. When this happens, heirs will be required to pay capital gains taxes on the property sale immediately.

Another big obstacle is sticking with the IRS timeline. As previously mentioned, the IRS has two strict deadlines for identifying replacement properties and closing the exchange. These deadlines are strict and cannot be extended except in cases of federally declared disasters. If any of these deadlines are missed, the exchange fails, and taxes could become due immediately.

This can be an issue, especially if the inherited property is owned by multiple family members, because all heirs must agree to participate in the 1031 exchange, and the ownership structure must be properly maintained. When there is disagreement about whether to sell and pay taxes or reinvest, this can affect timing. Choosing the right Qualified Intermediary is also important.

This is the person or company in charge of holding the money from the sale during the exchange. If the Intermediary makes mistakes, this can lead to serious problems and even an unfavorable tax ruling. Other issues include making sure the inherited property qualifies as an investment property and choosing a replacement property that is of equal or greater value than the original property.

How to Implement Best Practices in 1031 Exchange for Inherited Property?

A successful 1031 exchange does not happen by chance; it often involves thoughtful preparation, careful planning, and the right professional support. Taking the time to prepare can help heirs avoid mistakes, reduce stress, and make better long-term decisions. Below are some best practices for a successful 1031 exchange:

- Plan Early and Set Clear Goals: Before listing the property for sale, it is important to take out time and review its value, income history, expenses, and overall performance. Decide on time whether the goal is to increase cash flow, reduce management responsibilities, or diversify into a different type of property. If multiple family members own the property, they should agree on whether to perform an exchange or sell and pay taxes before listing the property.

- Engage a Qualified Intermediary Early: A QI must be selected before the inherited property is sold. If the sale closes and the heir receives the sale proceeds, the exchange will automatically be disqualified. Choosing the right Intermediary early ensures the transaction is structured correctly from the beginning.

- Begin Searching for the Replacement Property Early: Many investors often miss the IRS deadlines because they find it difficult to identify and close on the replacement due to many reasons. One best practice that takes care of this problem is to first of all identify potential replacement properties before selling the old one.

- Keep Detailed Records and Monitor Deadlines Carefully: It is essential to keep copies of contracts, agreements, financial statements, and correspondence. Ensure to track all required timelines and adhere to them. Missing any of these deadlines can cancel the exchange and trigger taxes.

What Are the Next Steps After Completing a 1031 Exchange?

After completing a 1031 exchange, the next step is to keep all documents relating to the exchange in an organized manner. Save closing statements, agreements, and any documents related to the sale and purchase. These records are important when filing taxes, especially to show that the sale was done under a 1031 exchange.

The next step is to pay attention to tax reporting and future tax impact. Even though you delayed paying taxes, the gain is still tied to the new property. It is important to work with a tax advisor to ensure everything is reported properly and how the deferred capital gains taxes can affect your current and future tax situation.

After the exchange, you should focus on managing the new property well. If it is a rental, make sure that it is properly maintained, the tenants are trustworthy, and income is being documented. Finally, plan ahead. Review how the property is performing and decide whether it aligns with your long-term goals.

Navigate Your Inherited Property 1031 Exchange with Confidence

If a person dies and leaves property to family members, they are faced with important decisions. They can sell it, keep it, or reinvest the proceeds into another property through a 1031 exchange. Each choice they make has its financial implications and tax effects. If the property is held for investment, it may be possible to sell it and reinvest the money into another investment property without paying taxes right away.

This can help preserve more of the value and ensures the investment to continue growing. Navigating a 1031 exchange with inherited properties can be challenging; hence, it is important to work with an experienced QI who can guide you through the entire process.

At Universal Pacific 1031 Exchange, we have assisted hundreds of heirs, real estate investors, and taxpayers in executing successful exchanges with ease. Our team of experienced Qualified Intermediaries can help you with the necessary paperwork, handling of sale proceeds, and facilitating the exchange to comply with all IRS rules. Reach out to us today to start an exchange.

FAQ

This section provides answers to common questions about 1031 exchange inherited property.

What Are the Rules for a 1031 Exchange on Inherited Property?

First, the property must be used for business or investment, not as your personal home. If you just inherited it, you usually need to hold it as an investment before starting the process. You must follow strict timelines: identify a new property within 45 days after selling and close on it within 180 days. You also need to use a qualified intermediary to handle the funds. If you receive the money directly, the exchange will not qualify.

Can You Do a 1031 Exchange on a Property Inherited From a Family Member?

Yes, you can, as long as the property is treated as an investment. It does not matter that it came from a family member. What matters is how you use it. If you rent it out or hold it for income or growth in value, it may qualify. If you move into it as your main home right away, it usually will not qualify.

Are There Any Tax Implications for a 1031 Exchange Involving Inherited Property?

Yes. Inherited property often comes with a stepped-up basis, which can reduce the gain if you sell it soon after inheriting it. If you complete an exchange, you delay paying capital gains tax, which reduces your overall tax burden. However, the tax is not erased. It carries over to the new property and may be due later when that property is sold without another exchange.

How Long Do I Have to Wait to Do a 1031 Exchange on Inherited Property?

There is no fixed waiting period written in the law. However, the property should clearly be held for investment purposes before starting the exchange. Many people rent it out for a period of time to show intent to hold it as an investment. Acting too quickly without showing investment use can trigger immediate tax liability.

Can You Use a 1031 Exchange to Defer Taxes on Multiple Inherited Properties?

Yes, it is possible. You can sell more than one property and use the proceeds to buy one or more replacement properties, as long as you follow the timing rules and value requirements. Each property must qualify as investment or business property, and all exchange funds must go through the intermediary to keep the tax benefit.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise is invaluable for complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise is invaluable for complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.