What Happens When You Sell a 1031 Exchange Property?

Selling a property acquired through a 1031 exchange can trigger deferred capital gains tax, depreciation recapture, and possible state tax unless the investor completes another properly structured exchange. This guide explains what may happen when you sell a 1031 exchange property, when taxes may become due, and what options may be available before closing.

In a delayed 1031 exchange, the sale proceeds should be held by a qualified intermediary or in an exchange account controlled through the exchange structure, so the taxpayer does not receive or control the funds. Replacement property must be identified within 45 days and the exchange completed within 180 days. If the investor sells a property previously acquired through a 1031 exchange and does not roll the proceeds into another properly structured exchange, the deferred gain may become taxable.

Planning to sell a property involved in a 1031 exchange? Universal Pacific 1031 can help coordinate the qualified intermediary process, exchange documents, fund handling, and deadline tracking before closing. Speak with our team early so your CPA, escrow, title, and advisory team can review the structure before proceeds are received. Contact us for a free consultation to discuss what may apply to your transaction.

This blog will provide a comprehensive guide to selling a 1031 exchange property, covering key considerations, tax implications, and various options available after the sale. It will also explore strategies for maximizing benefits.

What Is a 1031 Exchange Property?

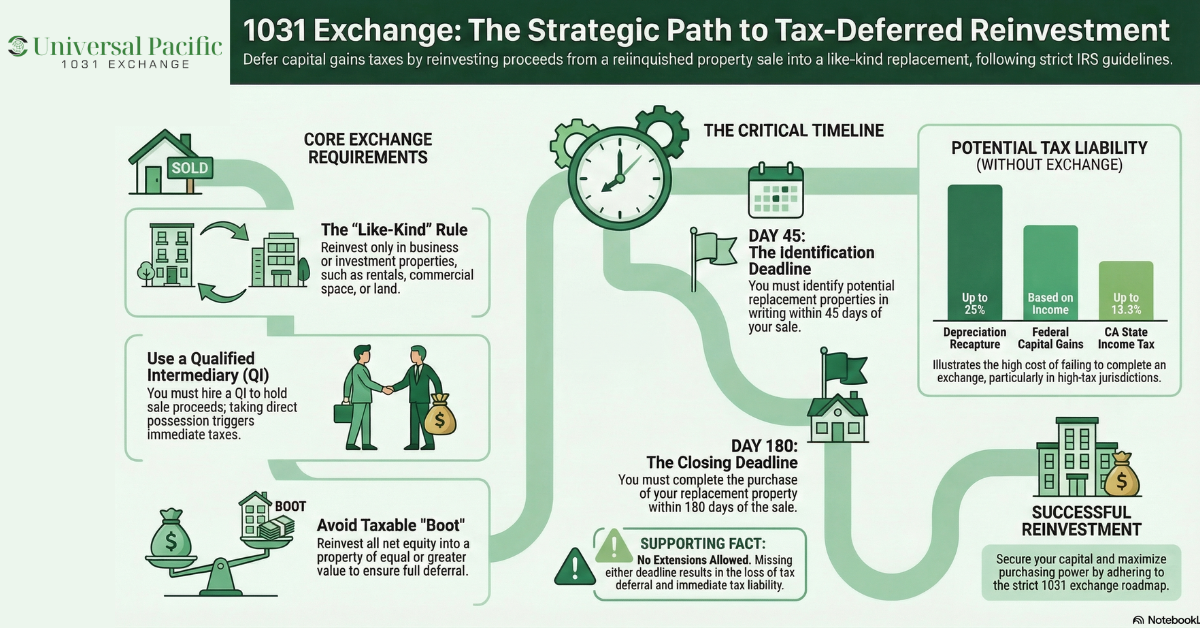

Real estate investors looking to postpone capital gains taxes under the U.S. Internal Revenue Code will find a useful tactic in a 1031 exchange, sometimes referred to as a tax-deferred exchange. Investors can defer instant tax obligations by reinvesting the proceeds from the sale of an investment property into a “like-kind” replacement property, therefore preserving their whole equity for the next purchases. This deferral gives investors a big benefit since it lets them increase their portfolios and buy more valuable real estate free from the weight of upfront taxes on sales.

A 1031 exchange’s main advantage—the tax deferral—defines its main use. Generally speaking, investors pay capital gains taxes on the profit when a property increases in value and is sold. But as long as the proceeds are reinvested into qualified properties, a 1031 exchange defers these taxes.

Important guidelines include exchanging “like-kind” properties, following rigorous deadlines (45 days to find replacement properties and 180 days to close), and finding a Qualified Intermediary (QI) to handle the sale revenues. It’s important to note that like-kind properties do not include primary homes; eligible properties range from residential rental properties to commercial real estate and unoccupied land. Understanding these rules will help investors use this tax-efficient technique for long-term financial gain.

What Happens When You Sell a 1031 Exchange Property?

If you sell a property acquired through a prior 1031 exchange, the deferred gain does not disappear. It may become taxable in the year of sale unless you complete another properly structured exchange before closing. Depreciation recapture may apply, boot may be taxable, and the taxpayer should not receive or control the exchange proceeds. State tax treatment may vary. Review the transaction with a CPA or tax advisor and engage a qualified intermediary early if you plan to continue deferring tax.

When you sell a property involved in a 1031 exchange, several important tax implications and procedural steps come into play that every investor should understand.

Tax Consequences of Selling a 1031 Exchange Property

A 1031 exchange allows real estate investors to defer capital gains taxes by reinvesting the proceeds from the sale of an investment property into another like-kind property. If the investor chooses not to reinvest and sells the property outright, capital gains tax may become due on the profit. This tax is calculated based on the difference between the sale price and the property’s adjusted basis, considering prior depreciation claimed during ownership. Prior depreciation may create unrecaptured Section 1250 gain, which can be taxed federally at a rate of up to 25%. The exact treatment depends on the property type, depreciation history, holding period, and reporting position, so investors should confirm the calculation with a CPA. In California, capital gains tax on real estate can be substantial. The depreciation recapture, taxed at rates up to 25%, may further increase the tax liability. Failing to complete another 1031 exchange can result in significant tax costs, reducing the investment’s overall financial benefit.

Depreciation Recapture

Any gain attributable to previously claimed depreciation must be reclaimed and taxed as ordinary income when a house is sold. Depending on the type of property and depreciation technique, the IRS taxes this part of the gain—known as “unrecaptured Section 1250 gain”—at rates up to 25%. This relates especially to real estate’s straight-line depreciation.

Investors who sell a property without reinvesting in another like-kind property have tax obligations on capital gains and depreciation recapture. Although capital gains are taxed at lower rates, the higher tax rate on recaptured depreciation will greatly lower overall profits.

State vs. Federal Taxes

Tax rules for 1031 exchanges varied greatly across states, influencing real estate investors’ decisions. The general profitability of real estate investments can be greatly impacted by high-tax jurisdictions like California, with a top income tax rate of 13.3%, and New Jersey, known for its high property taxes averaging 2.23%. On the other hand, low-tax states such as Florida and Nevada—which have no state income tax—offer better conditions for those trying to maximize returns on their assets.

When considering a 1031 exchange, an investor’s approach may change depending on these different tax systems. For example, reinvesting proceeds from a sale in a high-tax state may result in significant tax obligations, whereas low-tax jurisdictions offer increased cash flow and lower tax obligations. Making wise decisions about property sales and reinvestments depends on awareness of these variations since they immediately affect net returns and long-term investment objectives. To properly negotiate this complexity, investors should closely review their particular situation and speak with an expert tax advisor.

How to Sell a 1031 Exchange Property

Closing the sale of a 1031 exchange property is a pivotal moment that requires precision and careful attention to detail. Each step plays a crucial role in ensuring a smooth, compliant transaction. Here’s what to focus on:

Engage a Qualified Intermediary (QI):

A Qualified Intermediary (QI) is crucial for managing the sale proceeds and facilitating a 1031 exchange, ensuring compliance with IRS regulations. They not only manage the sale proceeds but also ensure full compliance with IRS regulations. By handling the funds and adhering to strict deadlines—45 days to identify replacement properties and 180 days to close—the QI keeps the process on track while protecting your tax deferral benefits.

Prepare Required Paperwork:

Sales agreements, property disclosures, title records, and closing remarks constitute the basic documentation that you need to prepare when closing the sale of the 1031 Exchange property. Each document serves a vital function: from outlining sale terms and disclosing known property issues to verifying ownership and recording the transaction’s financial details, ensuring transparency and legal compliance.

Conduct Due Diligence:

Ensure all property inspections and appraisals are completed, and any contingencies are addressed. Completing inspections and appraisals helps verify the property’s condition and value, addressing any potential issues before finalizing the deal.

Finalize Financial Arrangements:

Coordinate with lenders and financial institutions to secure financing for the replacement property. Securing financing ensures that you can successfully close on the replacement property without any delays or financial complications.

Involve Legal and Financial Professionals:

Attorneys and CPAs play a vital role in reviewing contracts, ensuring compliance with state and federal laws, and providing tax advice throughout the process. Their involvement ensures your legal and financial interests are fully protected during the exchange.

Step-by-Step Process for Selling a 1031 Exchange Property

If you’re planning to sell a 1031 exchange, it is important to have a proper understanding of how the exchange process works so you can defer capital gains tax and avoid costly mistake. Below is a step-by-step process on how to sell a 1031 exchange property.

Step 1: Listing and Marketing the Property: The first step is to list your investment property for sale. This could be a rental property, vacant land, or other investment real estate used for business or investment purposes and not personal use. At this stage, it is important to work with experienced real estate agents, price the property based on its market value, and ensure it qualifies as real property under the Internal Revenue Code. Note that personal assets such as a primary residence, vacation property, or personal property do not qualify for a tax-deferred exchange.

Step 2: Receiving Offers and Accepting a Contract: Once buyers show interest in your property, you review offers and accept the best one for your property sale. When accepting an offer, add language in the contract stating that you’re completing a 1031 exchange, ensure the buyer agrees to cooperate, and plan your timeline carefully to avoid tax issues. This step is important because it sets up the rest of the exchange process and helps protect your tax benefits.

Step 3: Engage a Qualified Intermediary: Investors generally engage a qualified intermediary before closing to help avoid constructive receipt of the sale proceeds. This is generally part of a properly structured delayed exchange. They are responsible for holding the exchange funds, preparing the exchange agreement, and ensuring you follow all tax regulations. This is important because you cannot receive the money yourself. If you do, it becomes taxable income, and you lose your tax deferment.

Step 4: Follow the 45-Day and 180-Day Deadlines: After closing the sale of your exchange property, the deadlines start counting. Replacement property must be identified in writing within 45 days. The three-property rule allows identification of up to three replacement properties, subject to the other identification rules. The property must also be of equal or greater value than that of the old property. Then you must close on one replacement property within 180 days. These must be like-kind property, meaning that they are also real estate assets used for investment purposes.

Step 5: Reinvest in a Replacement Property: Finally, you use the sale proceeds from the relinquished property to buy a new property. For full tax deferral, investors generally try to reinvest all net proceeds and acquire replacement property of equal or greater value, subject to CPA or tax advisor review. If done correctly, one can achieve capital gains tax deferment. The aim is to move from one investment property to another while deferring capital gains tax and reducing your current tax liability.

When Should You Sell a 1031 Exchange Property?

When considering the sale of a 1031 exchange investment property, investors often weigh various factors that influence their decision. Understanding the reasons to sell and the timing considerations can significantly impact their financial outcomes.

Reasons to Sell:

- When market conditions are favorable—that is, during a seller’s market where property values are high—investors could decide to sell. This helps them maximize their return on investment and take advantage of gains.

- Managing an investment property may become taxing, particularly if it needs continuous maintenance or significant repairs. Selling can relieve these headaches and help investors concentrate on more under-control properties or alternative investing methods.

- Investors may be prompted to sell by changes in their financial situations, including liquidity demands or retirement planning. Selling the house will free them from real estate ties and provide funds for other investments or personal needs.

- Investors could find greater prospects elsewhere, in other markets or kinds of properties, designed to support stronger returns. Sales let them reinvest in these more profitable choices.

- Selling a 1031 exchange property offers a chance to diversify your assets. The revenues can be used by investors in several asset types or geographical areas, therefore lowering the risk related to changes in the market.

Timing Considerations:

Maximizing earnings and tax benefits from selling a 1031 exchange investment property depends critically on timing.

- It is important to stay updated on real estate market developments. Selling at the proper time can greatly increase profits and create better chances for reinvestment.

- The choice to sell should also take possible tax consequences into account. Although a 1031 exchange lets you delay taxes, keeping those advantages depends on knowing when to sell and reinvest, therefore maximizing future tax obligations.

- If an investor chooses to do a 1031 exchange following a sale, they have to follow rigorous deadlines, choose a replacement property within 45 days, and finalize within 180 days. Proper timing ensures compliance with these regulations and helps avoid unnecessary tax liabilities.

Key Considerations Before Selling a 1031 Exchange Property

Many important factors might greatly affect your choice and financial results when selling a 1031 exchange property. It is imperative to see a tax expert or CPA. These advisors can help estimate the potential tax consequences of selling and review structuring options that may defer eligible gain. Their guidance helps investors understand how the federal and state tax rules may apply to their facts.

Then one must grasp the state of the existing market. Real estate markets change depending on local demand, interest rates, and economic trends, among other things. Examining these patterns will help you decide whether waiting would produce better returns or if selling now is a good time. Knowledge helps you to decide strategically when to reinvest.

Additionally, you should be aware of your long-term strategy and match your choice with it. Whether your goals are cash flow, capital appreciation, or diversification, it is imperative to make sure the sale fits your general goals. Examining these elements—consulting experts, evaluating market conditions, and articulating your investment objectives—helps you make wise decisions that improve your real estate investing.

Options After Selling a 1031 Exchange Property

Sales of a 1031 exchange property provide sellers with numerous options with different consequences. These are some choices:

Option 1: Complete Another 1031 Exchange

To complete a 1031 exchange, follow these essential steps and adhere to the specified time frames:

- Close the Sale of the Relinquished Property: The process begins with selling your original investment property.

- 45-Day Identification Period: You have 45 days from the closing date of the relinquished property to identify potential replacement properties. Identification must be in writing, specifying up to three like-kind properties.

- 180-Day Completion Period: You must close on the replacement property within 180 days of the relinquished property’s sale or by your tax return due date, whichever is earlier.

- Engage a Qualified Intermediary (QI): A QI is necessary to hold the sale proceeds and facilitate the exchange without triggering tax liabilities.

- Prepare Required Documentation: Ensure all necessary paperwork, including contracts and disclosures, is ready for both the sale and purchase.

- Consult Professionals: Work with legal and financial advisors to ensure compliance with IRS regulations throughout the process.

Option 2: Sell and Pay Taxes

It can make sense in some circumstances to cash out and pay taxes on a 1031 exchange property. Sellers who anticipate the market may drop or who wish to avoid the hassles of reinvesting may decide to realise their gains and pay the taxes if property prices have increased sufficiently.

Furthermore, sellers may cash out right away for other investments or personal requirements, depending on their financial demands. Under such circumstances, obtaining liquidity lets investors grab fresh prospects or handle pressing financial responsibilities—even if it means paying capital gains taxes. Ultimately, making well-informed decisions requires balancing the advantages of instant cash flow against possible future rewards.

Option 3: Use a DST as Replacement Property

For those using a 1031 exchange, investing in a Delaware Statutory Trust (DST) presents a passive investment choice. DSTs let several investors have fractional interests in real estate assets free from active management’s obligations. This arrangement will appeal to those who wish to engage in real estate investments but prefer to avoid the complications of property administration.

Investors can postpone capital gains taxes on the sale of their former real estate by making a DST investment via a 1031 exchange. This means they can reinvest their whole stock into the DST, enabling possible expansion and income generation free from immediate tax obligations. Since the DST structure complies with IRS rules, it is a good choice for tax deferral.

Moreover, DSTs usually consist of institutional-grade properties, therefore offering diversity over many asset classes and geographic areas. This helps investors to concentrate on other financial objectives while still improving investment stability by letting them profit from passive income sources. Generally speaking, DSTs offer a good approach to use the tax benefits of a 1031 exchange while engaging in passive real estate investment.

Strategies for Selling a 1031 Exchange Property

Maximizing the benefits of selling a 1031 exchange property requires strategic planning and careful execution. The following are some of the strategies that can be implemented to maximize benefits when selling a 1031 exchange property.

Timing Your Sale and Exchange

By timing your sale and exchange, you can maximize your profit. Keeping an eye on market trends helps you make wise choices to capitalize on favorable circumstances. It’s critical to conduct extensive research before purchasing the ideal replacement property. You should assess possible properties that fit your investment objectives. Working with real estate experts experienced in 1031 transactions can help you negotiate the complexity and definitely secure properties that fit your criteria.

Using a Reverse 1031 Exchange

A reverse 1031 exchange offers investors the flexibility to acquire a replacement property before selling their existing one, minimizing the risk of losing a desirable investment opportunity. To execute this, work with a Qualified Intermediary (QI) who will manage the exchange process. You can also coordinate with tax advisors and other tax professionals to ensure compliance with the tax code.

First, identify and acquire or park the replacement property first, and then sell the relinquished property within the safe-harbor timeline. The investor generally must identify the relinquished property within 45 days and complete the exchange within 180 days. This approach ensures a smoother transition between investments while preserving tax benefits.

How Soon Can You Sell a 1031 Exchange Property?

When considering how soon you can sell a 1031 exchange property, it’s essential to understand the specific timelines involved in the process. When you sell the relinquished property, there are two important deadlines that you must meet:

- 45-Day Identification Period: You have 45 days starting on the closing date of your relinquished property to find potential replacement locations. This identification must be completed on paper and given to your qualified intermediary (QI).

- 180-Day Completion Period: You have 180 days from the date of sale of the relinquished property to complete the purchase of the identified replacement property. It’s important to plan ahead because this time frame includes weekends and holidays.

If these deadlines are missed, the exchange can be disqualified and the deferred gain may become taxable. Investors should review the impact with a CPA or tax advisor. Prompt and efficient action is necessary to ensure compliance and optimize the benefits of a 1031 exchange during this time. By being aware of these deadlines, investors can plan their sales and reinvestments more carefully, ensuring a smooth exchange procedure.

What Happens If the 1031 Exchange Fails?

Real estate investors may suffer greatly financially from not finishing a 1031 exchange. The IRS will disqualify your transaction if you cannot locate a qualified replacement property within the designated deadlines—more especially, the 45-day identification period and the 180-day completion term. Your relinquished personal property will thus be handled as a taxable event, and you will be liable for capital gains taxes on any profits earned.

The IRS will tax your sale depending on the capital gains obtained from the sale when you miss these dates; this is computed as the difference between the sale price and your adjusted basis in the property. Any depreciation taken while the property is owned will also be liable to depreciation recapture, taxed at rates up to 25%.

Planning to Sell a 1031 Exchange Property?

Selling a 1031 exchange property involves deferred gain, possible depreciation recapture, and strict deadlines if you plan to continue deferring tax through another exchange. Understanding the dates for identifying and closing on replacement properties, working with a licensed intermediary, and staying on top of potential tax implications are all critical to protecting your returns. If you miss a deadline, your profits may be reduced by capital gains tax and depreciation recapture.

At Universal Pacific 1031 Exchange, we coordinate the qualified intermediary process, exchange documents, fund handling, and deadline tracking before closing. We work alongside your CPA, attorney, escrow, and title team throughout the exchange. Whether you’re looking to start a 1031 exchange or need assistance with compliance, our Qualified Intermediary can assist you. Ready to take the next step? Reach out to our 1031 exchange offices in Los Angeles for a free consultation, and let us guide you toward maximizing your real estate potential with ease.

FAQ

Below are common questions about selling a 1031 exchange property and their provided answers.

What happens when you sell a 1031 exchange property?

Selling a property acquired through a 1031 exchange can trigger the previously deferred capital gains tax, depreciation recapture, and possible state tax unless the investor rolls the proceeds into another properly structured exchange. If you cash out, the deferred gain may become taxable in the year of sale. Engage a qualified intermediary before closing if you plan to continue deferring tax, and review the transaction with a CPA or tax advisor.

Do you pay taxes when selling a 1031 exchange property, and can you do another 1031 exchange after selling?

Yes — if you sell outright without setting up another properly structured exchange, the deferred gain plus any depreciation-related amount may become taxable. You can do another 1031 exchange to defer eligible gain again if the structure is in place before closing and you meet the 45-day identification and 180-day exchange deadlines. Engage a qualified intermediary early and confirm the structure with your CPA or tax advisor.

What happens if you miss the 45-day or 180-day deadline?

Missing the 45-day identification deadline or the 180-day exchange deadline can disqualify the exchange and make the deferred gain taxable in the year of the relinquished sale. The IRS generally does not allow extensions for these deadlines, although a narrow disaster-area extension may apply in limited cases. Review the impact with a CPA or tax advisor.

What is boot when selling a 1031 exchange property?

Boot is any value the investor receives in the exchange that is not like-kind real estate. This includes cash boot (proceeds not reinvested) and mortgage boot (debt relief, when replacement debt is less than relinquished debt). Boot is generally taxable to the extent of recognized gain. Investors should review any cash, debt relief, or non-like-kind property received with their CPA or tax advisor.

Do you need a qualified intermediary before closing?

For a delayed 1031 exchange, the investor generally must engage a qualified intermediary before closing so the QI can accept assignment of the sale contract and receive the proceeds. The QI helps reduce the risk of constructive receipt by the taxpayer. Contact Universal Pacific 1031 as soon as the relinquished property is in escrow so the documents and coordination can be prepared on time.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.