Are 1031 Exchanges Only for Investment Properties?

No. A 1031 exchange is available only for real estate held for investment or used in a trade or business. Personal residences and properties held mainly for personal use do not qualify. Knowing which properties are eligible can help you avoid costly mistakes and complete your exchange correctly.

For over 30 years, Universal Pacific 1031 Exchange has assisted real estate investors, both new and experienced, through the complex process of 1031 exchanges. We can guide you through every step of the process, help you meet IRS deadlines, and make your exchange as simple and stress-free as possible. Contact us today, and let us help you defer capital gains taxes on your next exchange.

This article explains the types of properties that qualify for a 1031 exchange, provides a step-by-step guide to executing a seamless exchange, and addresses common questions about a 1031 transaction.

Understanding 1031 Exchanges

With a 1031 exchange, you can sell one property and buy another like-kind property while deferring the tax on your gain. The name comes from Section 1031 of the Internal Revenue Code, and people often call it a like-kind exchange. Instead of paying capital gains taxes now, you roll the capital gain into the replacement property. This makes it a powerful tax deferral strategy for real estate investors who want to keep their money working. One point matters up front, though. A 1031 exchange is tax-deferred, not tax-free. When the property is eventually sold without another exchange, the deferred tax comes due.

Eligibility Criteria for 1031 Exchanges

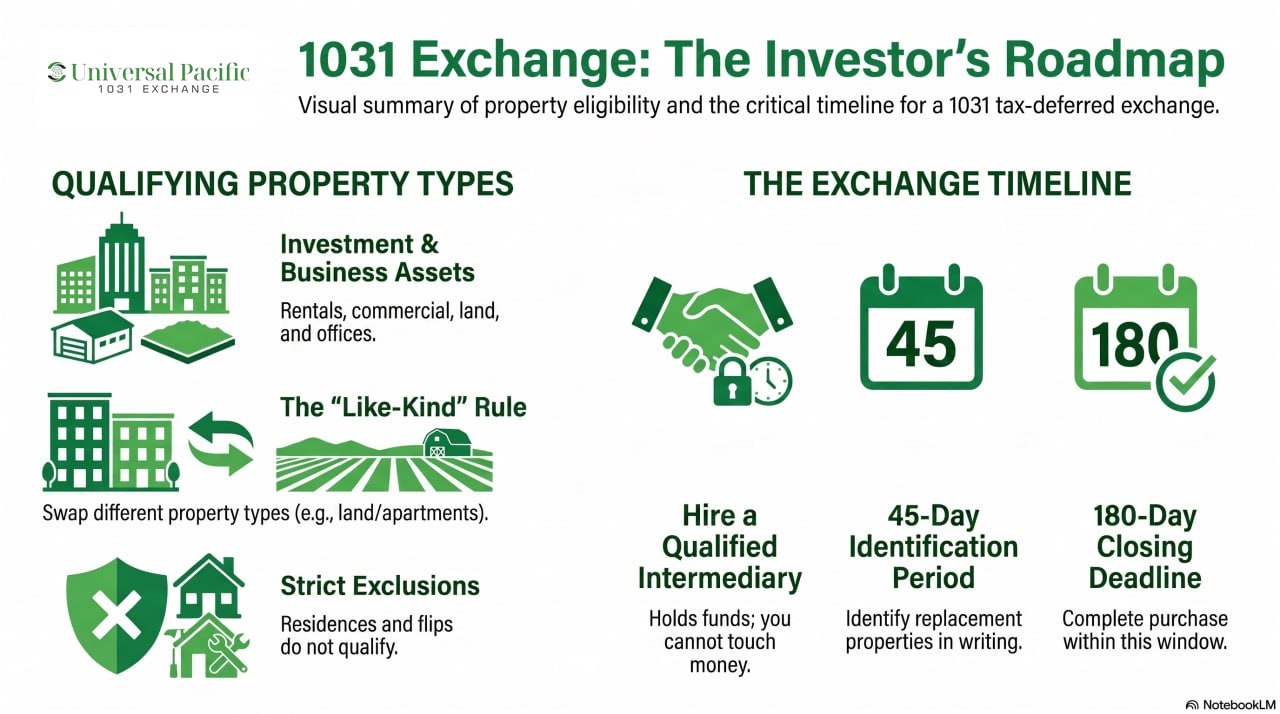

So are 1031 exchanges only for investment properties? No, and this is the myth worth clearing up. Under Internal Revenue Code Section 1031(a)(1), the property used in an exchange must be held for productive use in a trade or business or for investment. That little word “or” opens a second door. A building you run your own business from can qualify through business use, even if you would never call it an investment.

Like-kind is broader than it sounds too. Like-kind property means the same nature or character as real estate, not the same quality or grade. You can exchange real property for very different real property, and the exchanged property still qualifies. Raw land can be swapped for an apartment building, or an office building for farmland. The replacement can be almost any other property held for investment or business use.

Holding period is a common question with no clean answer. The law sets no minimum number of days. It turns on your intent to hold the property for investment or business purposes. Most tax professionals suggest holding at least one to two years to show that intent, though that is guidance, not a rule. Understanding the tax consequences of a short hold early prevents surprises later.

Types of Properties Eligible for 1031 Exchanges

There are two broad groups of properties that qualify. The first is investment property, which covers rental property, commercial buildings, and raw land held for investment purposes. The second is business property, which covers real estate you use to run a trade or business, such as a warehouse, a store, or a farm. Both count as investment and business property under the rule, and both can trade for the other.

Some qualifying property types surprise people. A long-term lease with 30 or more years to run can be exchanged for owned land. Fractional interests in a Delaware Statutory Trust can serve as replacement property under IRS guidelines. A few states even treat certain mutual ditch, reservoir, or irrigation company shares as real property. Personal property does not qualify, and neither do stocks, bonds, or partnership interests.

The table below sorts the common cases into what qualifies and what does not.

| Usually qualifies | Does not qualify |

|---|---|

| Rental homes and apartment buildings | Your primary residence |

| Commercial and office buildings | A vacation property used mainly by you |

| Raw land held for investment | Fix-and-flip homes held primarily for sale |

| Farmland and property used in your business | Dealer inventory, stocks, and partnership interests |

The exclusions deserve a closer look. Section 1031(a)(2) blocks properties held primarily for sale. A fix-and-flip bought to resell quickly is inventory, not an investment, so it fails. The IRS weighs your intent, how often you sell, and how long you hold when it decides whether you are a dealer.

Can I Do a 1031 Exchange on My Primary Residence?

No, your primary residence does not qualify for tax-deferral, because you hold it for personal use rather than investment. The tax break for a main home is a different one. Section 121 allows homeowners to exclude up to $250,000 of gain, or $500,000 for a married couple. You qualify for this exclusion if you’ve owned and lived in the house two of the last five years.

There is a workaround worth knowing. If you convert a former home into a genuine rental and hold it for investment, it can later qualify for a 1031 exchange. You can sometimes combine the Section 121 exclusion with 1031 deferral on a property that served as both a home and a rental. If you move into a property you received through an exchange, a five-year ownership rule applies before you can use the home-sale exclusion.

Can a Vacation Home Qualify for a 1031 Exchange?

Vacation homes sit in a gray area. A home you use purely for yourself does not qualify, even if it gains value. In Moore v. Commissioner, the Tax Court rejected an exchange of two lake houses because the owners used them personally and never rented them.

The IRS created a safe harbor in Revenue Procedure 2008-16 for second homes that are truly held for rental. Meet its personal use limits, and the IRS will not challenge whether you held the property for investment. The rules apply to both the relinquished property and the replacement property. The table below shows the test for each side.

| Requirement | Relinquished property | Replacement property |

|---|---|---|

| Ownership window | 24 months before the sale | 24 months after the sale |

| Rent at fair market value | 14 or more days each year | 14 or more days each year |

| Personal use limit each year | 14 days or 10% of rented days, whichever is greater | 14 days or 10% of rented days, whichever is greater |

Here is how the math works. If you rent the home 200 days in a year, your personal use can reach 20 days, since that is 10% of 200. Rent it only the minimum 14 days, and your personal cap drops to 14 days.

Step-by-Step Guide to Completing a 1031 Exchange

A 1031 exchange must follow a specific process to qualify for tax deferral. Missing a required step or an IRS deadline can make the entire transaction taxable. Planning ahead and working with experienced professionals can help the exchange move smoothly. Below is a simple explanation of each step.

Step 1: Choose a Qualified Intermediary Before You Sell

Before selling your property, you need to hire a qualified intermediary (QI). The qualified intermediary prepares the exchange documents and holds the sale proceeds during the exchange. You cannot receive or control the money from the sale at any point. If you do, the IRS may treat the transaction as a taxable sale instead of a valid 1031 exchange.

Step 2: Sell Your Current Property

The exchange begins when your original property, known as the relinquished property, is sold. Instead of sending the sale proceeds to you, the funds are transferred directly to the qualified intermediary. The date the sale closes is important because it starts both the 45-day identification period and the 180-day exchange period.

Step 3: Identify Your Replacement Property

After selling your property, you have 45 calendar days to identify the replacement property you plan to buy. The identification must be made in writing and submitted to your qualified intermediary. There are three major rules real estate investors use when identifying properties. This could be the three-property, 95%, or 200% rule. Identifying backup properties can help if your first choice becomes unavailable.

Step 4: Purchase the Replacement Property

You must complete the purchase of your replacement property within 180 calendar days after selling the relinquished property. This timeline includes the first 45 days used for identifying properties. If you miss the deadline, the exchange will usually fail, and the capital gain may become taxable. Any money left over after buying the replacement property, known as boot, may also be subject to tax.

Step 5: Report the Exchange on Your Tax Return

After the exchange is complete, you must report it to the IRS when you file your federal income tax return. This is done using IRS Form 8824. The form explains the details of the exchange and calculates any taxable amount if applicable. Keeping complete records of the transaction can make it easier to support your exchange if the IRS requests additional information later.

Maximizing Tax Savings with 1031 Exchanges

The real power is compounding. Each time you exchange instead of sell, you keep your full equity invested and defer the tax bill. Real estate investors use this to trade up from a single rental to larger real estate investments over time. Deferring taxes this way can move far more money into new property than selling and paying taxes at each step.

Michael Bergman, President and CEO of Universal Pacific 1031 Exchange, says it this way: “The biggest mistake I see is people assuming their flip or their beach house qualifies. Know which door your property fits through before you sell, not after.” A reverse exchange, where you buy the replacement first, adds flexibility when timing is tight. A tax professional and a qualified intermediary can help you avoid the traps.

How Do You Know if Your Property Qualifies?

The short answer is that 1031 exchanges reach far past passive rentals. Property held for investment, or for use in your trade or business, can qualify, while your home and your flips cannot. The vacation-home and conversion rules are where careful timing pays off. Getting the category right before you sell is the whole game.

At Universal Pacific 1031 Exchange, we help real estate investors across all 50 states confirm eligibility and hold their funds as a Qualified Intermediary. Our CPA-led team spots the traps, from dealer property to vacation-home limits, before they cost you the deferral. Call us before you list your property, so we can structure the exchange while every option is still open.

Frequently Asked Questions

This section provides answers to common questions about eligible properties for a 1031 exchange.

Are 1031 Exchanges Only for Investment Properties?

No. The property must be held for investment or for productive use in a trade or business. That means your own business real estate can qualify, not just passive rentals. Personal-use property like your home does not.

Can I Use a 1031 Exchange for My Primary Residence?

No, a primary residence is personal-use property and falls under Section 121 instead. You may exclude up to $250,000 of gain, or $500,000 if married. If you first convert the home into a real rental, it can later qualify for an exchange.

What Types of Properties Are Restricted?

Anything held primarily for sale is out, including dealer inventory and fix-and-flip homes. Personal property, stocks, bonds, and partnership interests never qualify. Since the Tax Cuts and Jobs Act, only real property is eligible at all.

Can I Exchange Any Real Estate Investment Property?

Generally yes, as long as both the relinquished property and the replacement are held for investment or business use. You can exchange one investment property for another of a different type. A rental duplex for raw land, or a store for an office building, both work.

Do Vacation Homes Ever Qualify?

Sometimes. A vacation property qualifies only if it meets the personal use limits in Revenue Procedure 2008-16. You must rent it at fair market value for at least 14 days a year and keep your own use low. A home you enjoy full-time does not qualify.

How Long Do I Have to Complete an Exchange?

The timing is strict and not flexible. You have 45 days from the sale to identify your replacement property in writing. You then have 180 days from the sale to close on it. Missing either deadline usually ends the deferral.

Legal disclaimer: This article is general information, not legal or tax advice. Tax rules change, and every situation differs. Speak with a qualified tax professional before starting a 1031 exchange.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.