Maximizing Your Investment: Understanding the 1031 Exchange Time Limit

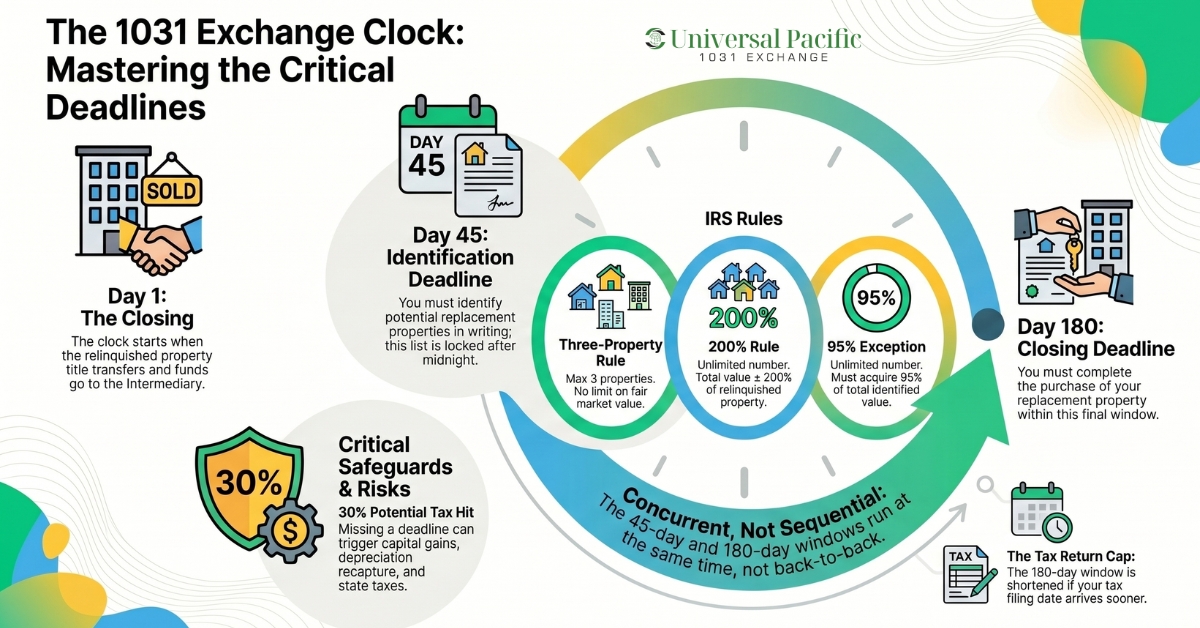

The 1031 exchange time limit is built around two deadlines that run from the day the relinquished property closes: 45 calendar days to identify potential replacement properties in writing, and 180 calendar days to close on one or more of them. Both windows are firm, both run at the same time rather than back to back, and the IRS does not pause them for weekends, holidays, or ordinary business delays. Real estate investors who plan around these deadlines from the day they list a property for sale rarely miss them, while those who treat the dates as flexible often forfeit the entire tax deferral they came to Section 1031 to capture.

Universal Pacific 1031 Exchange has over 32 years of experience in assisting real estate investors navigate the complexities of 1031 exchanges. We provide the guidance, expertise, and support needed to help investors meet IRS requirements and successfully complete tax-deferred transactions. Contact us today to get started.

This guide explains how the time limit works in detail, the identification rules, the consequences of missing a deadline, and the planning strategies that keep an exchange transaction on track.

Understanding the 1031 Exchange Timeline and Deadlines

A 1031 exchange is defined under code section 1031 of the Internal Revenue Code (IRC section 1031), with the procedural rules for delayed exchanges set out in Treasury Regulation §1.1031(k)-1. The IRS regulations on the exchange process are detailed, and the tax consequences of any procedural misstep are immediate.

The IRS allows a taxpayer to sell investment property or business property, defer the capital gains tax that would otherwise be due, and roll the sale proceeds into a like-kind replacement property held for productive use in a trade or business or for investment. Both the relinquished and replacement properties must be held for that purpose, and the ownership of each property acquired through the exchange must be in the same taxpayer’s name.

The two exchange timelines that define the time limit were codified by Congress in 1984, in response to the 1979 Starker tax court case (Starker v. United States, 602 F.2d 1341, 9th Cir.), which established that delayed exchanges were permitted under Section 1031. Congress accepted the concept but added the 45 and 180-day rules to prevent indefinite tax deferral.

The clock starts on the date the relinquished property closes, which is the day the taxpayer transfers title and the qualified intermediary takes possession of the sale proceeds. From that moment, the taxpayer has 45 days to identify replacement property and 180 days to complete the entire exchange transaction. Two important dates the investor should mark immediately: day 45 (the identification deadline) and day 180 (the closing deadline).

The 45-day Identification Period

The 45-day identification rule requires the taxpayer to identify potential replacement properties in writing, sign the identification, and deliver it to the qualified intermediary within 45 days of the date the relinquished property closes. The identification has to describe each property with enough detail that there is no ambiguity, usually by street address or full legal description.

Three identification rules give investors flexibility on how many properties they can name.

| Rule | What it Allows |

| Three-property rule | Identify up to three potential replacement properties regardless of their fair market value. |

| 200% rule | Identify more than three properties, as long as their combined fair market value does not exceed 200% of the relinquished property’s fair market value. |

| 95% exception | When the identification exceeds both the three-property limit and the 200% limit, the taxpayer must acquire replacement properties whose combined value equals at least 95% of the aggregate fair market value of all identified properties. |

Most exchanges use the three-property rule, since it is the simplest. The 200% rule serves investors who want to identify a basket of smaller potential replacement properties and choose among them. The 95% rule is a rescue valve that almost no investor relies on deliberately, because acquiring 95% of an over-identified pool is operationally difficult.

A practical tip from years of handling exchanges: start the suitable replacement property search before the relinquished property closes. The 45-day window is shorter than most investors expect, and finding the right asset under time pressure rarely produces a good outcome. Investors who line up two or three credible candidates before day one have room to negotiate and walk away from a bad fit. Investors who start the search after closing usually feel rushed and overpay.

Backup plans matter. A buyer can fall out of contract, financing can collapse, or a property can fail due diligence. Identifying one property and putting all of the exchange eggs in that one basket exposes the taxpayer to a single point of failure. The cost of identifying two or three properties is zero, and the optionality matters when something goes wrong.

A frequently misunderstood point: the IRS permits an investor to change the identified properties within the 45-day window. The taxpayer can revoke an earlier identification and submit a new one as long as it is delivered to the qualified intermediary on or before day 45. After day 45, the identification is locked, and the taxpayer can only acquire properties from the identified list.

The 180-Day Exchange Completion Period

The 180-day rule requires the taxpayer to receive the replacement property, meaning closing on the purchase, within 180 days of the date the relinquished property closed. The clock runs alongside the 45-day clock from the same start date, so an investor who waits 44 days to identify has given themselves only 136 days to close. A faster identification leaves more closing runway.

The 180-day rule has one important interaction with the tax year and tax return filing dates. The exchange must be completed by the earlier of 180 days from the sale or the due date of the taxpayer’s federal income tax return for the year the relinquished property was sold, including extensions. For an exchange that begins in November or December, this cap can shorten the practical deadline well below 180 days unless the taxpayer files for a tax return extension. Investors closing late in the tax year should plan for this interaction with their tax advisor before the relinquished property closes.

A few common pitfalls cause exchanges to fail in the 180-day phase. Buying a replacement property of lesser value than the relinquished property creates boot equal to the shortfall, which is taxable. Reducing the mortgage balance without offsetting it with new cash creates a form of boot, since the IRS treats debt relief similarly to cash received. Receiving any cash or non-like-kind property in the transaction creates boot. The replacement property’s purchase price should equal or exceed the relinquished property’s sale price for full deferral, and the taxpayer should reinvest all of the sale proceeds.

Can the 1031 Exchange Time Limit Be Extended?

For most exchanges, the answer is no. The IRS rules treat the 45 and 180-day deadlines as bright lines that do not move for weekends, holidays, financing delays, or business inconvenience. The tax court has consistently sided with the IRS when taxpayers ask for relief from missed deadlines for ordinary reasons.

There is one structural exception. The IRS provides limited extensions to the identification and exchange periods for taxpayers affected by federally declared disasters, through Revenue Procedure 2018-58 and case-specific IRS notices. When the President declares a disaster area covering the taxpayer or the property, the IRS often issues guidance allowing eligible taxpayers an additional 120 days to meet either deadline, subject to specific eligibility criteria.

The same extension was used during the COVID-19 pandemic and after major hurricane events. Investors who think they may qualify should consult a tax advisor immediately, because the eligibility window depends on the IRS notice issued for the specific disaster.

Outside of disaster relief, the consequence of missing a deadline is the failure of the exchange. The full amount of the gain on the relinquished property becomes taxable in the year of the sale, capital gains tax and depreciation recapture apply, and the taxpayer loses the tax deferral they were trying to capture. There is no general “good faith” exception, and the IRS does not grant private letter rulings to retroactively fix missed deadlines.

Understanding Like-Kind Properties in 1031 Exchanges

The 45 and 180-day deadlines mean little if the property is not like-kind. Section 1031, as narrowed by the Tax Cuts and Jobs Act effective January 1, 2018, applies only to real property held for investment or business purposes. The “like-kind” standard for real estate is broad. The IRS treats real property as like-kind to other real property even when the type, grade, or quality differs, as long as both properties are held for business and productive use. An apartment building can be exchanged for raw land, a single rental for a portfolio, or a warehouse for a retail center.

Property held for personal use does not qualify. A primary residence, a vacation home used mainly for personal use, and a fix-and-flip property held primarily for sale all fall outside Section 1031. The taxpayer’s intent at the time of the exchange is only one factor in this analysis, but it is the factor the IRS scrutinizes most closely, and the holding period before the exchange is used as evidence of intent.

The investment use or business use requirement also restricts foreign exchange. Real property in the United States is not like-kind to real property outside the United States, even if the foreign property is held for the same business or investment purposes.

Role of Intermediaries in 1031 Exchanges

A qualified intermediary is required for any delayed 1031 exchange. The intermediary holds the sale proceeds from the moment the relinquished property closes through the closing of the replacement property, prepares the exchange documents, tracks the 45 and 180-day deadlines, and ensures the taxpayer never takes constructive receipt of the funds.

Constructive receipt is the doctrine that the IRS uses to determine when a taxpayer has access to money, even if they have not physically received it. If the taxpayer can demand the exchange funds at any time, can control the funds, or direct how the funds are used outside the safe-harbor structure, the IRS will treat the taxpayer as having received the money. That single ruling can disqualify the entire exchange. Treasury Regulation §1.1031(k)-1(g) provides four safe harbors to protect taxpayers from constructive receipt issues, the most common of which is the qualified intermediary safe harbor.

Not every QI is equipped to handle every exchange. The factors that matter most are independence from the taxpayer (a QI cannot be the taxpayer’s attorney, accountant, real estate agent, or fiduciary within the previous two years), financial controls (segregated accounts, errors and omissions insurance, audit history), and the experience to handle complex structures like the reverse exchange and improvement exchange when the situation calls for them.

What Happens If You Miss the 1031 Exchange Time Limit?

The IRS treatment of a missed deadline is straightforward. The transaction is not an exchange for Section 1031 purposes, and the sale of the relinquished property is taxed as an ordinary sale. The tax-deferred treatment that would have applied is lost, and the benefits of the powerful tax deferral strategy disappear for that transaction. The taxpayer owes federal long-term capital gains tax at the applicable rate (up to 20 percent), the 3.8 percent net investment income tax where it applies, and state tax where applicable. Any depreciation taken on the property is recaptured at 25 percent under the unrecaptured Section 1250 gain rules.

The financial impact varies. For a property with a large built-in gain, the combined tax can run 30 percent or more of the gain. For a property held for many years with significant depreciation, the recapture alone can be substantial. Failed exchanges often result in tax bills well into six figures, which is the principal reason investors take the deadlines so seriously.

If an investor sees a deadline approaching with no clear path to closing, a few options remain. The taxpayer can sometimes restructure by acquiring a less ideal property on the identified list to preserve the exchange, even if the property is not the first choice. A reverse exchange, structured at the front end of the process, can avoid the back-end deadline pressure but requires planning before the relinquished property is sold. Once the 180-day deadline lapses, however, the exchange is over and the gain is taxable.

Strategies for Success: Navigating 1031 Exchange Time Constraints

![]()

The investors who run clean exchanges treat the timeline as the primary project from day one rather than the secondary concern. A successful exchange usually has these elements: a replacement property search begun before the relinquished property closes, and a written identification of two or three credible properties delivered to the QI well before day 45. It also includes financing pre-approved on the most likely replacement candidate, due diligence on the leading property substantially advanced before identification, and weekly checkpoints with the QI and the tax advisor to confirm the schedule.

Year-end timing deserves separate attention. An exchange where the relinquished property closes in October, November, or December runs into the tax return due date cap on the 180-day rule. The remedy is to file a tax return extension before the original due date, which preserves the full 180 days, but the extension has to be filed correctly and on time to work.

Reverse exchanges deserve consideration when the right replacement property is available before the relinquished property can be sold. In a reverse exchange, an exchange accommodation titleholder acquires the replacement property and holds it until the relinquished property sells. The same 45 and 180-day clocks apply, but they run from the date the replacement property is parked with the EAT rather than from the relinquished property sale. Reverse exchanges add cost and complexity, but they remove the time-pressure risk that catches many delayed exchanges off guard.

Checklist for Meeting All Exchange Deadlines

Before the relinquished property closes: engage a qualified intermediary, begin the replacement property search, talk with the tax advisor about year-end timing, and model the 45 and 180-day calendar dates.

Day 1 to Day 45: continue due diligence on candidates, deliver a written identification to the QI well before day 45, confirm the identification follows the three-property or 200% rule, and revoke and replace if a candidate falls out.

Day 45 to Day 180: secure financing on the leading identified property, complete due diligence, schedule closing well before Day 180, watch the tax return due date cap if the exchange spans tax years.

After closing: file Form 8824 with the federal income tax return for the year the relinquished property closed, keep the full exchange file (identification letter, closing statements, QI agreement, settlement records) with the return documents.

Engage a Qualified Intermediary Today

The 1031 exchange time limit is the single most important constraint in a delayed exchange, and missing either the 45 or 180-day deadline almost always ends the chance to defer capital gains taxes on the sale of the relinquished property. The IRS does not extend the deadlines for ordinary delays, weekends, or holidays, and the only meaningful exception is federally declared disaster relief.

Investors who plan the entire exchange around the calendar from day one, identify backup properties, file a tax return extension when the exchange spans tax years, and work with an experienced, qualified intermediary almost always finish on time.

If you are preparing to start a 1031 exchange, Universal Pacific 1031 Exchange can walk you through the timeline and the IRS rules before you list the relinquished property. Our team will help you structure the exchange correctly from the beginning, coordinate the required documentation, monitor critical deadlines, and serve as your Qualified Intermediary throughout the transaction. Contact us today to start an exchange

Frequently Asked Questions

Below are common questions about the 1031 exchange timeline and their respective answers.

What Is the Time Limit for a 1031 Exchange?

The time limit consists of two deadlines that run from the date the relinquished property closes. The taxpayer has 45 days to identify potential replacement properties in writing and 180 days to complete the purchase of one or more of them. Both clocks run at the same time, not back to back, and the 180-day deadline is also capped by the due date of the taxpayer’s federal income tax return for the year the relinquished property was sold, including extensions.

What Is the Time Limit for Identifying Replacement Properties in a 1031 Exchange?

The taxpayer must identify potential replacement properties within 45 days of selling the relinquished property. The identification must be in writing, signed by the taxpayer, and delivered to the qualified intermediary. After day 45, the list is locked, and the taxpayer can only acquire properties from that identified list.

How Long Do Investors Have to Close on Replacement Properties in a 1031 Exchange?

Investors have 180 days from the closing of the relinquished property to close on the replacement property, or the due date of their federal tax return for that tax year (including extensions), whichever is earlier. The deadlines are calendar days, not business days, and the IRS does not extend them for weekends or holidays.

Can the Time Limits for a 1031 Exchange Be Extended?

In most cases, no. The 45 and 180-day deadlines are firm under the IRS rules, and the tax court has consistently upheld them. The principal exception is federally declared disaster relief, which the IRS provides under Revenue Procedure 2018-58 and disaster-specific notices. Eligible taxpayers may receive up to 120 additional days when the President declares a disaster covering the taxpayer or the property.

What Happens If an Investor Fails to Meet the Time Limits in a 1031 Exchange?

The exchange fails for Section 1031 purposes, and the sale of the relinquished property is taxed as an ordinary sale in the year of the sale. Capital gains tax, depreciation recapture at 25 percent, and applicable state tax all become due. Depending on the gain and the depreciation history, the tax can run 30 percent or more of the sale proceeds.

Are there any Exceptions to the Time Limits in a 1031 Exchange?

The only general exception is federally declared disaster relief. No ordinary business reason, financing delay, escrow issue, or unforeseen complication qualifies for relief outside the disaster framework. Investors should not plan around the assumption that an extension will be available.

Does the 180-Day Rule Include Weekends and Holidays?

Yes. The 180-day rule is measured in calendar days, including weekends and federal holidays. The IRS does not extend the deadline when day 180 falls on a Saturday, Sunday, or holiday, which is one of the most common surprises for investors completing year-end exchanges.

What Happens If My Replacement Property Falls Out of Escrow?

If the replacement property fails to close before day 180, the exchange fails for that property. The taxpayer can still close on another property from the identified list within 180 days if one exists, which is why backup identifications matter. If no identified property closes by day 180, the exchange is over.

Can I Change Identified Properties After 45 Days?

No. After the 45-day identification deadline, the list of identified properties is locked. The taxpayer can change or revoke identifications within the 45-day window by submitting an updated identification to the qualified intermediary on or before day 45, but no changes are permitted after that date.

Does Filing a Tax Extension Affect the Exchange Deadline?

It can help. The 180-day clock is capped by the due date of the federal income tax return for the year the relinquished property closed, including extensions. For exchanges that span tax years, filing a timely tax return extension before the original due date preserves the full 180 days. Without the extension, the deadline can be shortened to the original April due date, which can be well inside 180 days.

What If I Identify Multiple Replacement Properties?

The IRS allows multiple identifications under the three-property rule, the 200% rule, or, in narrow situations, the 95% rule. The three-property rule lets the taxpayer name up to three properties regardless of value. The 200% rule allows more than three identifications as long as their combined fair market value does not exceed 200% of the relinquished property’s value. The 95% rule applies when both prior limits are exceeded and requires the taxpayer to acquire 95% of the value of identified properties.

Can Disaster Relief Extend the 1031 Exchange Deadline?

Yes, in limited circumstances. When the President declares a disaster, and the IRS issues guidance covering 1031 exchanges, eligible taxpayers may receive additional time to meet the 45 or 180-day deadlines. The standard framework is set out in Revenue Procedure 2018-58, and the specific extension is governed by the IRS notice issued for the particular disaster. A tax advisor should review eligibility immediately, since the relief is time-sensitive.

Disclaimer: This article is for general educational purposes and does not constitute tax or legal advice. A qualified intermediary handles and documents a 1031 exchange but does not provide tax or legal advice. IRS rules and state rules can change, and every transaction depends on its own facts. Investors should consult a licensed tax professional before starting an exchange.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.