Effective Failed 1031 Exchange Compliance Practices

A 1031 exchange can be a powerful tax-deferral tool for many real estate investors seeking to build wealth; however, it follows complex rules and strict deadlines. Even small mistakes can lead to total disqualification, triggering unexpected taxes and penalties.

It is important to understand common pitfalls and how to avoid them to protect your capital and keep it working for you. Working with a Qualified Intermediary can also help ensure compliance and avoid mistakes that could lead to costly tax consequences later on.

At Universal Pacific 1031 Exchange, we’ve helped hundreds of real estate investors navigate the complex process of a 1031 exchange with ease. We understand how stressful and confusing the whole process can be, so we assist you in drafting the necessary documents, ensuring your exchange funds are handled correctly, while maintaining strict compliance with the IRS procedures. Reach out to us today to start an exchange.

This article explores the various reasons why an exchange fails, the consequences of a failed 1031 exchange, and how to prevent it.

What Is a Failed 1031 Exchange?

A failed 1031 exchange is a situation where a real estate investor attempts to defer capital gains taxes under Section 1031 but does not meet one or more of the IRS requirements. When any of these rules are not met, the exchange fails, and the IRS treats the transaction as a normal real estate investment sale rather than a tax-deferred exchange. According to a quote from Justin Bergman:

“Even seasoned investors can have a 1031 exchange fail. Missing deadlines, taking direct control of sale proceeds, or not properly identifying replacement property can all cause the IRS to disqualify an exchange”

This means that the investor must recognize the gain and pay taxes in the tax year the property was sold. A 1031 exchange is generally designed to allow investors and other taxpayers to defer capital gains taxes when they sell an investment property. By rolling the exchange proceeds of the sale of one investment property into another, they can avoid paying immediate capital gains and keep more of their capital working for them.

However, this is only possible if all the strict legal and procedural requirements are fully satisfied; if not, the exchange loses its tax-deferral status. Common reasons why a 1031 exchange fails include missed deadlines, improper documentation, or choosing unqualified properties.

How Do Failed 1031 Exchanges Occur?

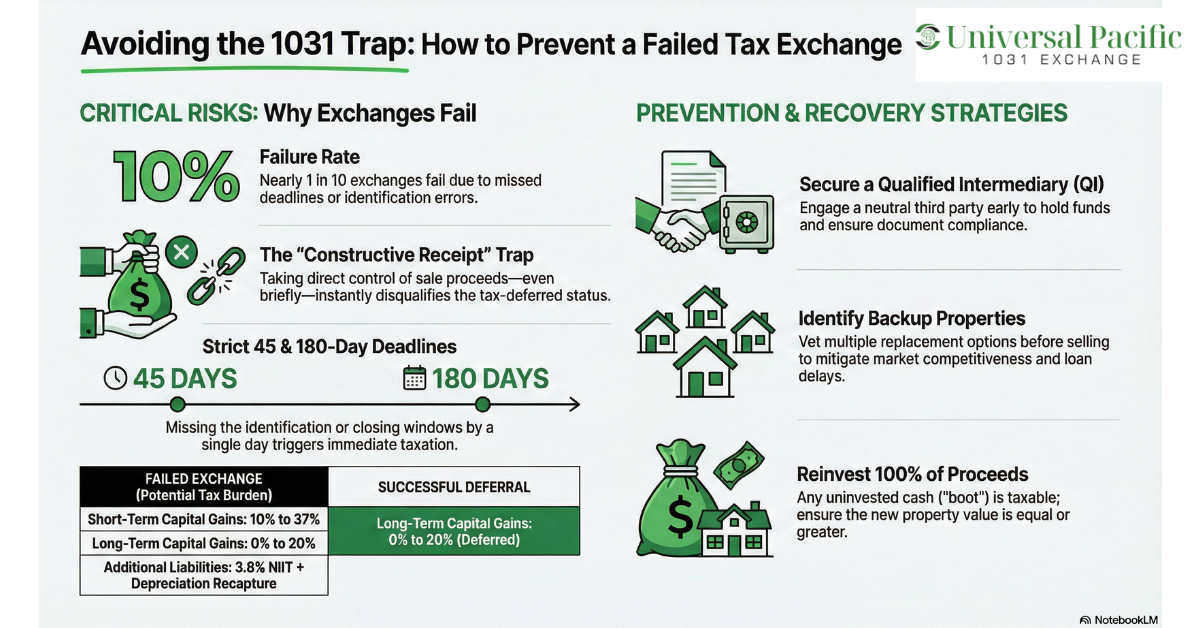

A 1031 exchange is governed by strict rules and timelines, and missing any of them could cause the exchange to be disqualified by the IRS. Industry research shows that about 8% – 10% of attempted exchanges do not complete successfully due to missed deadlines or inability to secure like-kind replacement properties. Below are some of the common reasons why a 1031 exchange might fail.

Not Using a Qualified Intermediary

One common cause of a failed exchange is not working with a Qualified Intermediary. For an exchange to be considered valid, the IRS requires that the proceeds from the sale of a relinquished property be held by a Qualified Intermediary. A Qualified Intermediary is a neutral party responsible for holding sale proceeds in an escrow account, ensuring strict compliance throughout the transaction, and ultimately facilitating the entire exchange process.

If the investor or taxpayer takes direct possession of the funds, even for a short time, it would result in immediate tax liability. For example, in this case study between Christensen v. Commissioner, the US Tax Court ruled that the taxpayer had direct access to the exchange proceeds during the transaction lost eligibility for a 1031 treatment. The court decided that constructive receipt of funds invalidated the exchange, leading to immediate taxation of the gain.

Missing the IRS Timelines

The IRS places strict timelines by which potential replacement properties must be identified and closed on. After the relinquished property sale, the IRS allows a 45-day period for you to properly identify replacement properties and submit to the QI in writing. You also have 180 days from the original property sale to purchase replacement properties and close the exchange. These timelines are very strict; they run even during weekends and holidays and cannot be extended except in cases of federally declared disasters.

Missing these deadlines could lead to the disqualification of the entire exchange process. Let’s take a real case study to see how important these deadlines are. In Dobrich v. Commissioner, the taxpayer tried to carry out a 1031 exchange but failed to properly identify the replacement property within the 45-day identification window. Because of this, the IRS disqualified the exchange, and the court upheld that decision, making the entire gain taxable.

Not Adhering to the Identification Rules

There are three basic rules investors can use when purchasing multiple replacement properties. They are the three-property rule, the 95% rule, and the 200% rule. The three-property rule allows investors to identify up to three replacement properties regardless of their market value. The 95% rule allows investors to identify more than three properties as long as the total value of the properties acquired equals at least 95% of the total value of the identified properties.

Under the 200% rule, investors can identify more than three properties as long as the total fair market value does not exceed 200% of the relinquished property. Failing to adhere to these rules can cause the exchange to fail. Additionally, the identified properties must be clearly written down and submitted to the QI. The identification notice must include:

- The property’s street address

- Clear description of each new property

- The name of the taxpayer completing the exchange

- A clear statement that the listed properties are being identified as potential replacement properties to show bona fide intent to complete a like-kind exchange

- The date of the identification notice

- The taxpayer’s signature.

Choosing Non-Like Kind Property

To perform a 1031 exchange, the IRS requires that both the relinquished and replacement property be like-kind. This means that they must both be held for business or investment intent. Properties that qualify include land, apartment buildings, retail spaces, office buildings, or other real estate used for investment or business. Personal residences, vacation homes not rented for investment, or property held primarily for resale (like flips) are considered non-like-kind property and do not qualify. Choosing a replacement property that does not meet this criterion could lead to the disqualification of the exchange, requiring the taxpayer to pay capital gains taxes in the tax year of the sale.

Failing to Invest the Entire Sale Proceeds

Another common mistake investors make in a 1031 exchange is not using all of the exchange proceeds from the relinquished property sale when acquiring the replacement property. If a taxpayer fails to invest all of the money when purchasing the replacement property, any cash or portion of the proceeds that is not reinvested is called cash boot, and this becomes immediately taxable and can reduce or eliminate the purpose of the exchange, which is basically to defer taxes. When you choose a replacement property that is worth less in value than the relinquished property, the remaining cash is taxed. Additionally, if the replacement liability is less than the relinquished liability, the difference may be treated as taxable income.

What Are the Consequences of a Failed 1031 Exchange?

When an exchange fails, the IRS treats the sale of the relinquished property as a standard property sale, and this eliminates the tax-deferral benefit of the exchange. This means the capital gains from the sale become immediately taxable, and the investor must pay capital gains taxes in the taxable year. In tax year 2022, taxpayers paid approximately $336.3 billion in federal capital gains taxes, showing how significant these liabilities can be when gains are realized instead of deferred.

Depending on how long you’ve held the property, your capital gains can be subject to either short-term (less than a year) or long-term (over a year). Federal tax rates for short-term holdings are 10% to 37%, depending on your total taxable income. Long-term capital gains rates are taxed at 0% for lower-income taxpayers, 15% for most taxpayers, and 20% for high-income taxpayers. There is also an additional 3.8% Net Investment Income Tax (NIIT) that could apply to certain high-income taxpayers.

Losing your tax deferral benefit can harm your investment strategy, especially if you planned to move a large profit into a replacement property. Once the exchange falls through, the investor can no longer delay paying taxes; instead, the full capital gains tax liability becomes due immediately.

This can include federal taxes and, in many cases, also state and local taxes. On top of that, any depreciation previously claimed on the relinquished property may be taxed through depreciation recapture. This eventually leads to the total tax bill being higher than expected, leaving the investor with less money to invest.

How Can a Failed 1031 Exchange Be Avoided?

One of the most important steps to avoid your exchange being disqualified is to engage a Qualified Intermediary from the outset. A good QI will ensure that exchange proceeds are handled with care and that all necessary documentation is accurate and properly filled. The intermediary should also have extensive experience in like-kind transactions and understand how to effectively navigate compliance requirements.

Another key step is to maintain strict adherence to the IRS deadlines. Most investors find it difficult to secure suitable replacement properties within the stipulated timeline due to market competitiveness and sometimes, the inability to secure a loan. To avoid this, we recommend having a replacement property as a backup option before selling the original property. It is also important to carefully review each potential replacement property to ensure that it qualifies as investment property and meets the IRS like-kind requirement.

Also, properly vet the properties to ensure that they are equal to or greater than the relinquished property in value before listing them as replacement properties. The most successful exchanges are usually planned before the relinquished property is sold. Try to speak with a tax advisor, coordinate with real estate agents, and review financing in advance before starting an exchange.

What Are the Next Steps After a Failed 1031 Exchange?

A failed exchange can be discouraging and even frustrating, but that does not mean that you are out of options. There are still practical steps you can take to manage the financial impact and move forward. Below are some of them:

Step 1: Review Your Tax Position Immediately

The first step to take after a failed exchange is to calculate the total capital gains from the relinquished property sale. To do this, you need to subtract depreciation from the purchase price plus the cost of improvements to determine your adjusted basis. This helps you prepare for the tax bill due in that taxable year and avoid confusion or surprises.

Step 2: Consult With a Tax Professional

The next step is to schedule a professional consultation with a tax advisor as soon as possible. A tax professional can help evaluate your situation and tell you the options available to you and the next possible step. They also help to ensure that your tax return is accurate and that you strictly adhere to the IRS rules.

Step 3: Explore Other Tax Relief Options

Even if your 1031 exchange did not work out, you still have other ways to reduce your tax burden. For example:

- Use capital losses to offset capital gains

- Consider an installment sale method if it aligns with your goals

- Reinvest in another investment property

- Adjust your overall tax planning strategy for the following year

- Use a tax straddling strategy

These steps may not fully replace the full potential benefit of a successful exchange, but they can also help to lower the overall financial impact.

Step 4: Reassess Your Investment Strategy

After settling the current tax issues, you need to review your long-term goals. This will help you prepare better for a future like-kind exchange.

Navigating the Aftermath of a Failed 1031 Exchange

Executing a successful 1031 exchange can prove challenging due to the IRS’s strict rules and guidelines. As a result, many investors end up making mistakes that eventually cost them their tax-deferral benefit.

Such mistakes include missing the IRS strict timeline, exchanging non-like-kind properties, not investing the entire sale proceeds into the like-kind replacement property, and, worst of all, not working with a Qualified Intermediary. In case your exchange has already fallen through, you are not without options. A Qualified Intermediary or tax professional can guide you on the next best step to reduce your financial burden.

At Universal Pacific 1031 Exchange, we work diligently to see that both investors and taxpayers preserve their capital without losing it to unnecessary taxes. We understand how disappointing a failed exchange is, so we structure each exchange with documentation and processes designed to support IRS compliance. Are you thinking of performing a successful 1031 exchange? Contact us today to get started.

FAQs

This section provides answers to frequent questions about failed 1031 exchanges.

What Are the Consequences of a Failed 1031 Exchange?

When a 1031 exchange transaction fails, the IRS treats the sale as a regular property sale instead of a tax-deferred exchange. This means the taxpayer must recognize and pay capital gains taxes when filing the tax return for the following tax year.

Can You Still Defer Taxes After a Failed 1031 Exchange?

In many cases, once an exchange is disqualified, you cannot go back and fix it; the original tax-deferral opportunity is lost. That said, this does not mean that you have no options. There are other planning strategies that may be available depending on timing and your overall investment objectives.

How Common Are Failed 1031 Exchanges?

It is estimated that 8-10% of attempted 1031 exchanges fail to complete. Although it is not so common, most failures come from missed deadlines, documentation issues, or financing problems that can delay closing.

What Are the Steps to Rectify a Failed 1031 Exchange?

While a 1031 exchange failure cannot generally be rectified, there are steps to take to move forward. The first step is to properly evaluate the full financial impact by calculating how much is owed. After this, consider speaking with a qualified tax professional to adjust your future investment plans to make up for the missed tax deferral. Even if the exchange cannot be repaired, you can still take steps to manage the outcome and avoid compounding the problem.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.