Does Vacant Land Qualify for a 1031 Exchange?

You bought a parcel of raw land years ago, and today a buyer is offering far more than you paid. That gain feels great until you see the capital gains taxes waiting on the other side of the sale. A 1031 exchange gives you a legal way to postpone that bill and keep your money working in new real estate. However, knowing whether vacant land qualifies, what rules apply, and how to structure the exchange correctly is essential.

Since 2015, Universal Pacific 1031 Exchange has served real estate investors in all 50 states as a qualified intermediary. Our team carries over 32 years of combined experience and has closed more than $100 million in commercial real estate across 1,000-plus exchanges. Contact us today to initiate an exchange.

This article covers what a 1031 exchange entails, properties that qualify for a tax-deferred transaction, and the process of conducting a 1031 exchange with vacant land.

Understanding 1031 Exchanges

A 1031 exchange takes its name from Section 1031 of the Internal Revenue Code. It lets you sell one investment property and buy another without paying immediate capital gains taxes on the sale. The property you sell is called the relinquished property. The property you buy is called the replacement property.

The core idea is tax deferral, not a permanent escape. You are not paying taxes now, but the deferred gain follows you into the new property. When you eventually sell without another exchange, the tax liabilities come due. Many investors continue exchanging for years. Under current federal tax law, assets included in a decedent’s estate may receive a step-up (or step-down) in basis, which can affect the deferred gain for heirs. Because estate and tax rules can change, investors should discuss this strategy with a qualified tax advisor.

The idea has deep legal roots. In Alderson v. Commissioner, a 1963 case, a federal appeals court backed an investor who swapped land instead of selling it. The Aldersons had their buyer acquire a second parcel and trade it for theirs, and the court upheld the deal. That ruling helped open the door to the facilitated land exchanges intermediaries handle today.

The Tax Cuts and Jobs Act of 2017 narrowed the rules. According to the IRS, Section 1031 now applies only to exchanges of real property. It no longer covers personal property or intangible assets after December 31, 2017. For land and buildings, the strategy remains fully intact. The tax laws still favor patient real estate investment.

Vacant Land as a Qualifying Property

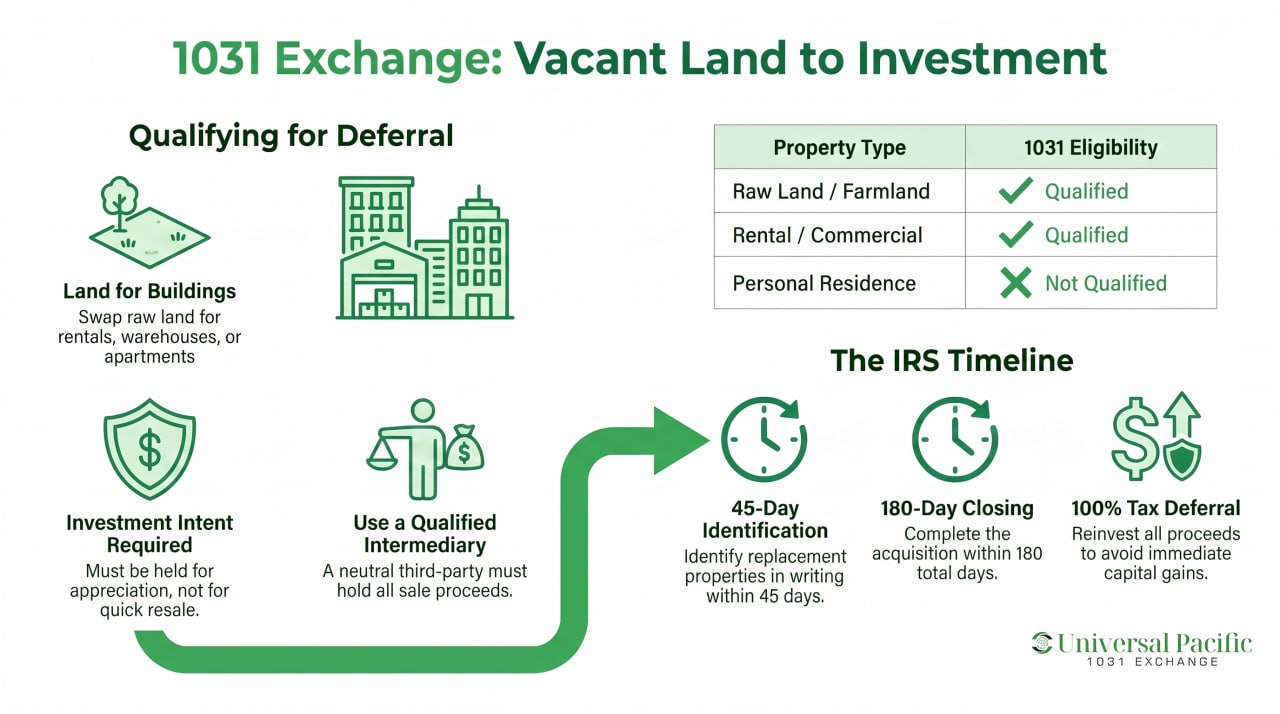

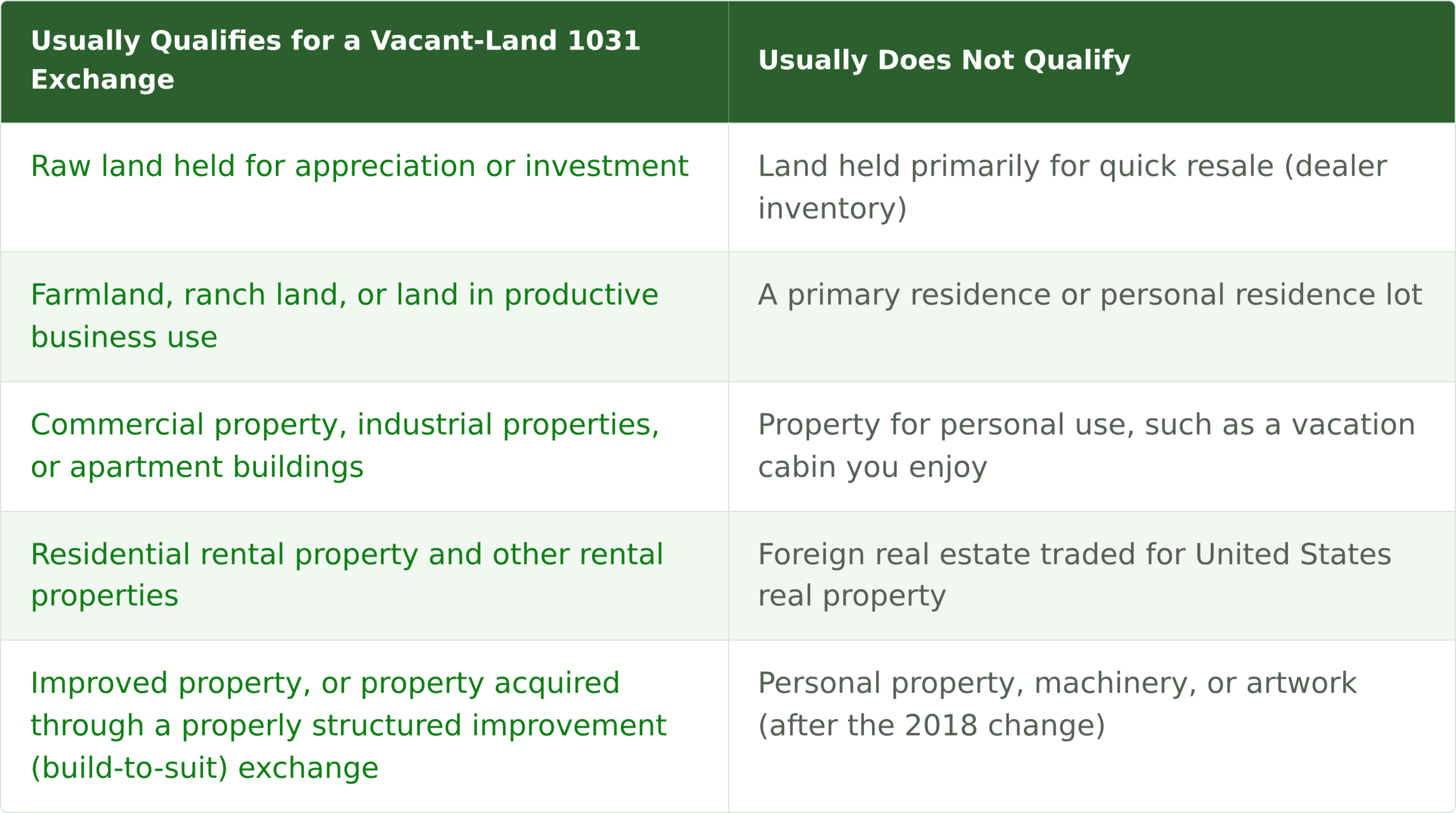

Yes, vacant land qualifies for a 1031 exchange. The land must be held for investment or for productive use in a trade or business. That is the same standard the IRS applies to any real property in an exchange. Raw land held for appreciation is a textbook example of property held for investment purposes. Land used in your trade counts as business property held for investment or business purposes.

The IRS confirms that unimproved land counts. In its like-kind exchange guidance, the IRS states that real properties are generally like-kind whether they are improved or unimproved. The IRS states that real property improved with a residential rental house is like-kind to vacant land.

What matters is why you hold the property. Land you bought to resell quickly is treated as inventory, not investment. That kind of property held primarily for sale does not qualify. Your personal residence and any land for personal use also fall outside the rules. Those are not held for business or investment purposes.

Like-Kind Property Rules

The phrase like-kind confuses many first-time exchangers. It does not mean the two properties must look alike. It means they share the same nature or character as real estate. The IRS puts it plainly. Properties are of like-kind if they share the same nature or character, even when they differ in grade or quality.

Because almost all real estate shares that character, your options are wide. You can trade vacant land for a very different asset class and still qualify. The main geographic limit is that United States real property is not like-kind to foreign real estate.

The table below shows how a vacant land exchange typically breaks down. It separates the property types that qualify from those that do not, so you can gauge your own situation quickly.

As the table shows, land can move into buildings and buildings can move into land. A property owner can swap one investment property, a bare lot, for a leased warehouse among industrial properties. All of these are valid real estate transactions under the like-kind property rules.

Dealer vs. Investor: Why Holding Intent Matters

Holding intent decides many land transactions. The IRS looks at whether you held the property for investment or as stock you flip for profit. Someone who buys and resells parcels rapidly may be classified as a dealer. Dealer property is inventory, and inventory never qualifies for tax deferral.

This is where proper documentation earns its keep. Records that show you held the land for appreciation, leased it, or used it in business support your position. Short holding periods, frequent sales, and marketing the land for resale point the other way.

“The biggest mistake we see with land is intent,” says Michael Bergman, CPA, president and CEO of Universal Pacific 1031 Exchange. “If you flip parcels every few months, the IRS may treat you as a dealer, and dealer property cannot go into an exchange. We help clients document that the land was truly held for investment before they sell.”

Benefits of Using Vacant Land in a 1031 Exchange

Using vacant land in a 1031 exchange offers numerous benefits for real estate investors. You defer capital gains taxes that would otherwise hit at the closing table. Left unsheltered, that gain can face a heavy federal tax bill. As of 2026, federal long-term capital gains rates are generally 0%, 15%, or 20%, and some higher-income taxpayers may also owe the 3.8% Net Investment Income Tax. Keeping that money invested is a powerful tax advantage, because you compound on the full sale price rather than the after-tax amount.

Section 1031 also gives you flexibility to reshape your real estate portfolio. You can trade your current property, an idle lot, for a building that pays rent every month. This lets you move toward your investment goals without triggering immediate tax liabilities. Many investors use this tax deferral strategy to shift from raw land into cash-flowing real estate assets.

These deals matter beyond any single investor. A 2021 Ernst & Young study, published by the National Multifamily Housing Council, measured how much like-kind exchanges move the economy. It found that Section 1031 exchanges supported roughly 976,000 jobs in 2021. The same study tied them to $97.4 billion in value added and $13.1 billion in federal, state, and local taxes.

Process of Executing a 1031 Exchange With Vacant Land

The exchange process runs on strict rules and short deadlines. Missing one step can turn a tax-deferred trade into a fully taxable sale. Here is how a clean land exchange usually moves forward.

1. Engage a Qualified Intermediary

Before you close on the sale, you hire a qualified intermediary. This is a neutral third party who holds your sale proceeds. You cannot touch that money, or the exchange fails. The intermediary works alongside your title company to handle the paperwork on both closings.

2. Sell the Relinquished Property

You sell your original property, the land, and the proceeds flow to the intermediary rather than to you. This starts the clock on the exchange period. Your tax professional and the intermediary confirm that the sale documents flag the transaction as part of a 1031 exchange.

3. Identify Replacement Property Within 45 Days

You have 45 days from the sale to identify potential replacement properties in writing. Per the IRS instructions for Form 8824, this deadline is firm. Most investors identify their options early and line up several backups.

4. Close on the New Property Within 180 Days

You must acquire the replacement property within 180 days of selling the original property. The new property should be equal or greater in value to defer the entire gain. If you take cash or reduce debt, that leftover value is called boot, and boot is taxable.

5. Report the Exchange to the IRS

A successful exchange still gets reported. You file Form 8824 with your tax return for the year of the sale. Keeping proper documentation of every step protects you if the IRS reviews the transaction later.

Common Challenges and Solutions

Financing raw land is harder than financing a building, so plan the replacement side early. Lenders often want more equity for land, which can shrink your buying power. Working with real estate professionals who understand exchanges helps you find similar property that fits both your budget and the deadlines.

Timing is the challenge investors underestimate most. The 45-day window to identify properties is short, and good deals move quickly. A practical fix is to start shopping for the new property before your land even sells. Some investors use a reverse exchange, which lets you buy the replacement property first and sell the land second.

You may also worry about depreciation recapture. Vacant land is not depreciable, so raw land usually carries no recapture on the sale. If your replacement property is a building, future depreciation and recapture attach to that improved property instead. A tax professional can model the tax implications before you commit.

Other Ways to Structure Your Exchange

Not every investor wants to manage another property directly. Delaware Statutory Trusts, often shortened to DSTs, let you exchange into a fractional share of larger real estate assets. A DST can hold apartment buildings, industrial properties, or commercial property, and it counts as like-kind real property. This suits owners who want income without landlord duties.

Reverse exchanges and improvement exchanges add more room to maneuver. A reverse exchange helps when the perfect replacement appears before your land sells. An improvement exchange lets you use exchange funds to build on the new property. Each structure follows the same IRS regulations, so the parties involved must document everything carefully.

Top Misconceptions About 1031 Exchanges

The most common myth is that the properties involved must be identical. They do not. Land can be swapped for a rental building, and the reverse works too. Both are real estate of the same nature.

Another myth is that a 1031 exchange erases taxes forever. It does not. The strategy defers tax, and the gain rides along until a later taxable sale. Touching the sale proceeds early also ends the exchange.

People often assume any property qualifies. It does not. A primary residence, a second home kept for personal use, and land held primarily for sale all sit outside the rules. Knowing which properties qualify before you sell saves you from an expensive surprise.

Is Vacant Land the Right Move for Your Next Exchange?

Vacant land can be one of the most flexible pieces in a 1031 exchange when you hold it for investment or business use. The rules reward patience, planning, and clear records that prove your intent. If your land has appreciated and you want to defer capital gains taxes, an exchange keeps your equity invested and growing. The deadlines are strict, so the earlier you plan, the smoother the trade.

At Universal Pacific 1031 Exchange, we act as your qualified intermediary and guide every step from the first call to the final closing. Our team coordinates with your title company and tax professional so the paperwork, timelines, and identification rules are handled correctly. Schedule a free exchange review with us before you sell your land, and we will build the timeline around your closing date.

Frequently Asked Questions

Below are common questions about executing a 1031 exchange with vacant land.

What Are the Requirements for Vacant Land to Qualify for a 1031 Exchange?

The land must be held for investment or for productive use in a trade or business. It cannot be property held primarily for sale, and it cannot be for personal use. You must use a qualified intermediary, meet the 45-day and 180-day deadlines, and reinvest the proceeds into like-kind replacement property. Keeping proper documentation of your intent and the transaction is part of every successful exchange.

Does Vacant Land Qualify for a 1031 Exchange?

Yes. The IRS treats raw land held for investment as real property that qualifies for tax deferral. The vacant land must have been held for business or investment purposes, not for quick resale or personal use. When that is true, it can serve as the relinquished property in a 1031 exchange.

Are There Any Specific Requirements for the Vacant Land to Qualify?

The key requirement is holding intent, backed by evidence. Records showing appreciation strategy, leasing, farming, or other business use support your case. Land you bought to flip fast can be classified as dealer inventory, which fails to qualify. A qualified tax advisor can review your situation and confirm the property meets IRS regulations before you sell.

Can I Exchange Vacant Land for Other Real Estate in a 1031 Exchange?

Yes. Because nearly all United States real estate is considered like-kind, you can exchange land for many property types. Common trades include swapping vacant land for residential rental property, commercial property, apartment buildings, or industrial properties. You can also exchange into improved property or new construction, as long as the value is equal or greater.

Can I Exchange Vacant Land for a Different Type of Property?

Yes, and this flexibility is one of the biggest reasons investors use exchanges. Land does not have to be traded for more land. You can move from a bare lot into rental properties, a warehouse, or a Delaware Statutory Trust that holds larger real estate assets. The one firm limit is that United States property cannot be exchanged for foreign real estate.

How Long Do I Have to Identify and Acquire a Replacement Property?

You have 45 days from the sale of your original property to identify potential replacement properties in writing. You then have 180 days from that same sale date to close on the new property. According to the IRS instructions for Form 8824, both deadlines run from the day you transfer the relinquished property. They do not extend for weekends or holidays, so plan early.

What Are the Potential Tax Benefits of Doing a 1031 Exchange With Vacant Land?

The main benefit is deferring the immediate capital gains taxes you would owe on an outright sale. That deferral keeps your full equity invested, which compounds your buying power over time. You can also reshape your real estate portfolio, moving from idle land into income-producing property that fits your investment goals. These tax benefits make the exchange a proven tax deferral strategy and one of the most trusted tax strategies for real estate investors.

The information in this article is provided for general educational purposes only and should not be considered legal, tax, or financial advice. While every effort has been made to present accurate and up-to-date information, 1031 exchanges are governed by complex federal tax rules, and each transaction involves unique facts and circumstances that can affect eligibility and tax consequences.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.