Can You Do a 1031 Exchange on a Second Home?

Many real estate investors seeking to expand their portfolios and diversify into different property types frequently ask, “Can you do a 1031 exchange on a second home?” The simple answer is yes, you can, but only if the property is treated as an investment property and not as a personal residence.

As long as it is held for business or investment purposes, the IRS allows you to sell the property and reinvest the proceeds into another like-kind property while you defer capital gains taxes. However, the process requires careful planning, strict compliance, and the presence of a Qualified Intermediary to be successful.

Universal Pacific 1031 Exchange has 35+ years of experience in facilitating successful exchanges across the 50 US states. We have helped thousands of property owners and real estate investors complete smooth and compliant exchanges while protecting their investment capital and deferring capital gains taxes. Contact us today to start an exchange.

This article explores the requirements for converting a second home to an investment property, the benefits of 1031 exchanges, as well as the challenges real estate investors face when performing an exchange.

What Is a 1031 Exchange on a Second Home?

A 1031 exchange, named after Section 1031 of the Internal Revenue Code, is a tax-deferral strategy that allows a real estate owner to sell one property and reinvest the proceeds into another like-kind property without paying immediate capital gains taxes. Rather than paying taxes at the time of sale, they are able to defer these taxes until they sell without another exchange.

In this process, the property that is sold is called the relinquished property, and the new property is referred to as the replacement property. The exchange must involve real estate, and not personal property, which means that it must be held for business or investment purposes. The exchange must also be structured properly according to the IRS’s strict rules and deadlines. The purpose of this exchange is to allow real estate investors to continually keep their investment capital working rather than immediately paying capital gains tax.

The term second home simply refers to a property that is not one’s primary residence. A 1031 exchange involving a second or vacation home just means applying the same exchange rules to that type of property. Using second homes has become common, so much so that in 2025, about 27 out of every 100 homes in the US were bought by investors. However, there are certain requirements that must be met for a second home to qualify for tax-deferral benefits.

How Do You Qualify a Second Home for a 1031 Exchange?

Not all second homes can be used for a 1031 exchange. The IRS outlines certain rules that determine if a second home or vacation property can qualify for an exchange. Below are some of the main qualification criteria.

1. Use as an Investment Property

The most important rule for both second homes and any other replacement property is that they must be held for business or for investment use in a trade or business. In plain terms, the second home must function as an investment property eligible under Section 1031. This means the property must be owned with the intent to invest, earn rental income, or increase in value as part of your real estate investment strategy.

According to the U.S. Census Bureau, 37% of homes in the United States are not lived in by the owner. Instead, these homes are rented out or held as investment properties. The IRS generally checks the use of the rental property to determine if it qualifies for a 1031 exchange or not.

2. Rental Requirements

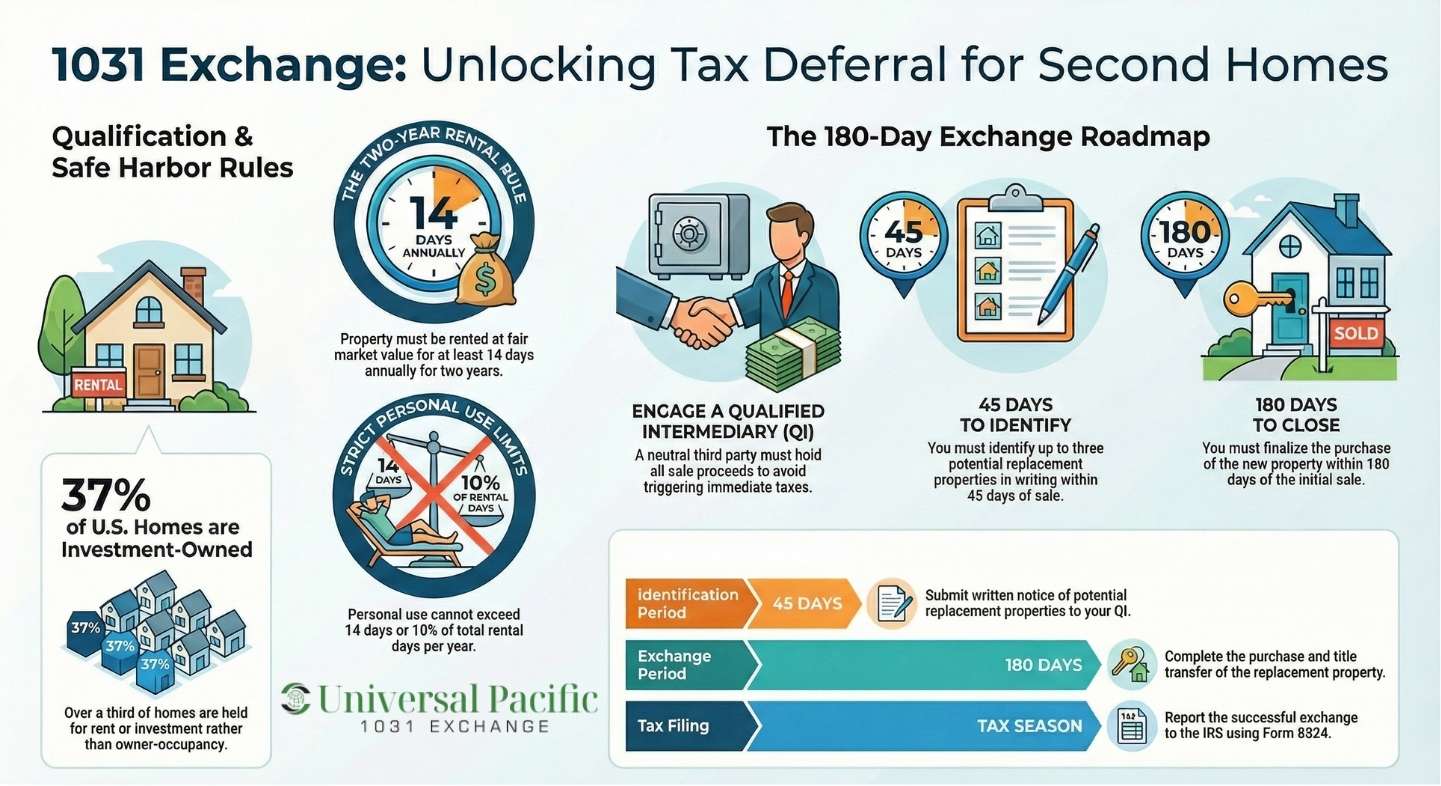

To prove investment intent, the property must be rented at fair market value. This means you must charge a normal fair market rent for occupancy and not a discounted rate for friends or family. Under Revenue Procedure 2008-16, also known as the safe harbor rule, the property should be rented out for at least 14 days per year for at least two years before the exchange. For example, in a case between Moore v. Commissioner, the US Tax Court ruled against certain taxpayers who tried to use their second home in a 1031 exchange because they never rented the property out and only used it for personal enjoyment.

The rental must be real and not a staged act; it must be documented and produce real rental income. To show that the property was used for business or for investment purposes, you should advertise the property, report income, and handle property maintenance like a landlord during those two years.

3. Personal Use Limitation

Even if the property is a second home or vacation property, you must put limits on personal use. Using the property for personal enjoyment exclusively can disqualify the exchange. Under the IRS safe harbor, your personal use of the property must not exceed 14 days per year or 10% of the total days the property was rented at fair market value, whichever is greater. Abiding by these laid-down limits can help to prove that the property was held for productive use rather than personal living.

What Are the Steps to Perform a 1031 Exchange?

After the above requirements have been satisfied, the second home can then be qualified as a like-kind property. However, executing a 1031 exchange in a second home requires careful planning and strict compliance with the IRS rules. A 1031 exchange is not just a simple buy and sell process; it follows a structured format to defer taxes fully. We’ve broken it down to a simple step-by-step process you can follow.

Step 1: Hire a Qualified Intermediary

Before even listing the property for sale, it is always advisable to engage a Qualified Intermediary (QI). Many real estate investors make the mistake of assuming that this step is optional or voluntary; however, it is a critical rule of a 1031 exchange. Without a QI, the IRS does not consider your exchange valid.

These QIs are neutral third parties responsible for holding the proceeds after the sale of a relinquished property. These proceeds are held in a segregated escrow account and then used to purchase the replacement property.

A QI also helps in preparing the necessary exchange documents that will be used during the process. They also help in documenting all communication and transactions while guiding you through every step of the process to avoid mistakes that could lead to the loss of your tax deferral benefit.

Step 2: Sell the Relinquished Property

Once your Qualified Intermediary is in place, you can go ahead to sell your original property. After the close of the sale, it is important not to take direct possession of the sale proceeds, as this can trigger what is called a “constructive receipt”. This simply means that the IRS will view that sale as any other taxable real estate sale and would require you to pay capital gains taxes immediately.

To avoid this, ensure that the money from the sale goes directly to the Qualified Intermediary. Selling the relinquished property officially begins the 1031 exchange timeline countdown. Additionally, it is important that the closing documents clearly state that the sale is part of a Section 1031 exchange and not a regular sale.

Step 3: Identify the Replacement Property Within 45 Days

After the sale of the relinquished property, you have exactly 45 days to identify your replacement property. The IRS deadline is very strict and does not allow for extensions except in cases of federally declared disasters. Also note that holidays and weekends are included in this timeline. This simply means that because the 25th of December is Christmas, it doesn’t mean that the timeline takes a break.

To avoid missing this deadline, it is advisable to start looking for a replacement property even before selling the old one. The property identified must be made in writing, signed by you, and handed over to your Qualified Intermediary. In most cases, you can identify up to three potential replacement properties regardless of their value, depending on the identification rule you choose. Each identified property must be like-kind and must be equal to or greater in value than the relinquished property.

Step 4: Purchase the Replacement Property Within 180 Days

You must close on the purchase of the replacement property within 180 days from the date the relinquished property was sold. Some real estate investors usually fall into the error of thinking that the 45 and 180-day periods are different. However, these timelines run concurrently, meaning that the 180 days include both the 45-day identification period. In reality, after identifying replacement properties, you have 135 days to close on the property.

To fully defer taxes, you must make sure that the replacement property is equal to or greater in value than the property that was sold, and you must reinvest all your sale proceeds to avoid taxable boot. If the relinquished property has debt on it, also ensure that the replacement property has the same amount of debt or even greater to avoid tax consequences. To purchase the property, the Qualified Intermediary transfers the sale proceeds to the seller to finalize the exchange.

Step 5: Report the Exchange to the IRS

After completing the exchange, you must report to the IRS when filing your tax return for that year. This is done using IRS Form 8824. You must also accurately account for the exchange, such as the closing documents, evidence that you did not take possession of the proceeds, identification notices, and exchange agreements.

Filing this form ensures that the exchange is formally recognised under the Internal Revenue Code and your taxes are deferred and not triggered. Accurate reporting is essential because errors in filing can lead to IRS audits or tax issues later on.

What Are the Benefits of a 1031 Exchange on a Second Home?

The biggest advantage of a 1031 exchange is the ability to defer taxes. Under normal circumstances, when you sell an investment property, you must pay taxes of 15-20% on the profit from the sale. This tax payment reduces the money you have available to reinvest in the purchase of another property. This was one of the biggest concerns amongst real estate investors, which led to a decrease in real estate investing.

However, after the 1031 exchange rule was established, real estate investors and even taxpayers can now keep more of their profits working for them rather than losing them to taxes. Another important benefit is portfolio diversification. This is particularly an appealing benefit for most investors seeking to grow their portfolio. A 1031 exchange gives you the flexibility to move from one property type to another as long as the new property is like-kind and held for investment.

For example, you can exchange a single rental home for apartment buildings, commercial real estate, and even multiple properties. Some investors even move into Delaware Statutory Trusts (DSTs) or other forms of fractional ownership interests to reduce management responsibilities. A 1031 exchange also increases investment power. Because you are deferring taxes, you can have more money available to purchase a higher-value replacement property.

What Challenges Might You Face With a 1031 Exchange?

A 1031 exchange can be a powerful tool for real estate investors, but it is not without its own challenges. When using a 1031 exchange on a second home that has been treated as an investment property, there are several challenges that can arise. One major challenge is maintaining compliance with the IRS rules. According to Micheal Bergman:

Many property owners don’t know how useful a 1031 exchange can be for making smart, long-term decision about their real estate. More often many investors have little or no knowledge about how an exchange works which leads to many complications during the process.

The IRS requires that any property used in a 1031 exchange must meet the like-kind requirement, meaning that it must be held for business or investment purposes. If the requirements for converting your second home into a business property are not met, the entire exchange can be disqualified.

Hence, it is important to maintain rental agreements, proof of fair market value rent, expense records, rental income documents, and evidence of investment usage. Another major challenge is keeping to the IRS’s strict timelines. Once a relinquished property is sold, the IRS clock starts ticking. You have only 45 days to identify potential replacement properties and 180 days to close the transaction.

As previously mentioned, these timelines are strict and rarely extended. In a competitive real estate market, finding suitable replacement properties can be difficult, and securing them can even be more challenging. The best solution is to be prepared ahead of time. Start searching for replacement properties even before selling the original property. Having a backup option can help to reduce stress and prevent you from missing these deadlines and disqualifying the exchange.

Finding a suitable replacement property is also difficult. Aside from the competitive market concerns, it is also difficult to find a property with equal or greater value or debt to your relinquished property. It is either this or prices might be too high, and financing may prove difficult to secure. To avoid this, stay flexible during your search for properties. You can expand to different property types or even geographical areas as long as they are still within the U.S.

Unlock the Potential of Your Second Home With a 1031 Exchange

A 1031 exchange is a tax-deferral tool that allows you to sell and buy real estate properties without paying immediate capital gains. Simply by rolling over the proceeds from the sale of one investment property to another, adhering to the IRS timelines, and complying with the laid-down rules for an exchange, you can continually grow your portfolio, build wealth, and even expand into higher-income-producing properties.

As beneficial as this may sound, it is usually complex, as a single mistake can immediately trigger tax consequences. To avoid this, you must work with a Qualified Intermediary well experienced in carrying out numerous exchanges to guide you through the process.

At Universal Pacific 1031 Exchange, we help both new and experienced real estate investors navigate even the most complex of 1031 exchanges. Our team is skilled in guiding you through every step of the process with ease, ensuring that all IRS rules are strictly followed and your taxes stay continually deferred. We also work closely with your real estate agent, escrow officer, and tax advisor to keep the process smooth from beginning to end. Looking to start an exchange? Book a call today.

FAQs

Below is the answer to the question, “Can you do a 1031 exchange on a second home?”, as well as other related questions.

What Are the Rules for Doing a 1031 Exchange on a Second Home?

The main rule is that the property must be held for investment or business use. A second home cannot be treated as a personal residence or mainly used for personal enjoyment. It must show investment usage by being rented out at a fair market value and producing real rental income.

In other words, the exchange must involve real property and not personal property, and the new property must be like-kind. You must also make use of a Qualified Intermediary to hold exchange funds, adhere to the IRS strict timelines, and reinvest the entire proceeds into a replacement property of equal or greater value to fully defer taxes.

Can I Use a 1031 Exchange to Upgrade to a Larger Second Home?

Yes, you can move into a larger or more valuable property, as long as the new property is also held for investment purposes. Many real estate investors use a 1031 exchange to move from smaller, lower-income-producing properties to larger and higher-value properties.

Are There Any Time Limits for Completing a 1031 Exchange on a Second Home?

Yes, the IRS’s strict timelines govern any 1031 exchange, irrespective of the properties or location involved. The IRS allows you 45 days to identify potential replacement properties and submit in writing to your QI after the sale of your original property. From this time, you also have 180 days to purchase the replacement property or properties, as the case may be, and close the exchange. Missing any of these deadlines could result in the exchange being taxable.

What Are the Tax Implications of Doing a 1031 Exchange on a Second Home?

When a 1031 exchange is structured properly, it allows you to defer capital gains taxes on the sale of your investment property. This includes both long-term capital gains and potential depreciation recapture. However, note that these taxes are only deferred and not deleted; the gains deferred are carried over into the replacement property for as long as you perform a like-kind exchange. If you eventually sell the property without another exchange, the deferred capital gains immediately become taxable.

Can I Do a 1031 Exchange on a Second Home If I’ve Already Done One on My Primary Residence?

Yes, because you have previously done a 1031 exchange does not prevent you from completing another one, as long as the properties involved meet Internal Revenue Code Section 1031 requirements. However, a primary residence does not qualify for a 1031 exchange because it is considered personal use property. If you previously converted a primary residence into an investment property and it was properly held for investment, it may qualify.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.