1031 Exchange Timeline

The 1031 exchange is a popular strategy for real estate investors to defer capital gains tax. It is termed “like-kind exchange” because it involves the sale of an investment property for a replacement property of a similar nature and character. Aside from its tax deferral strategy, it also allows investors to grow and diversify their portfolios.

For a successful exchange, the IRS requires that you adhere to a strict timeline of 180 days, consisting of the 45-day identification period and the remaining 135 days for completing the exchange. Failure to comply with these time requirements can disqualify your exchange and thus make your gains taxable.

Finding a reputable QI to guide you through the 1031 exchange timeline does not have to be a hassle. With 35+ years of experience, our licensed CPA professionals at Universal Pacific 1031 Exchange are experts at facilitating smooth and compliant 1031 exchange transactions. Schedule a free consultation with us to discuss your extension request and guide you through the process.

In this article, you’ll learn everything about the 1031 exchange timeline and its recent changes to avoid potential pitfalls that can disqualify your exchange.

What Is a 1031 Exchange and How Does It Work?

A 1031 exchange is a real estate investment strategy that allows you to defer capital gains taxes when you reinvest the sale proceeds of one investment property into another like-kind property. It takes its name from Section 1031 of the U.S. Internal Revenue Code and is regulated by the IRS. For a successful exchange, investors are required to understand and comply with the IRS regulations guiding the 1031 exchange.

For example, both the relinquished and replacement properties must be held for business or investment purposes. That means that you cannot use personal property, such as a primary residence. The properties must also be like-kind. You can purchase multiple properties as long as you follow the 1031 exchange identification rules.

You must also reinvest ALL the sale proceeds to fully defer taxes, unless you’re running a partial 1031 exchange where only the reinvested portion is tax-deferred. More importantly, you must complete the exchange transactions within the various deadlines that make up the 180-day timeline. Let’s look at a breakdown of the exchange timeline to help you stay on track.

Note that how these rules apply may vary depending on the 1031 exchange types. There are generally four types of exchange: the forward exchange, the simultaneous exchange, the reverse exchange, and the construction or improvement exchange. For example, reverse exchanges allow you to purchase the replacement property before selling the relinquished property. Therefore, you’ll be required to hand over the title to the replacement property to the Exchange Accommodation Titleholder until you sell the original property.

Breakdown of the 1031 Exchange Timeline

Since missing any of the 1031 exchange deadlines in the 180-day timeline disqualifies your exchange, you need a proper understanding of the timeline so you can plan your transactions to align properly. Below, we’ve provided a summary of the key deadlines and dates in the 1031 exchange process.

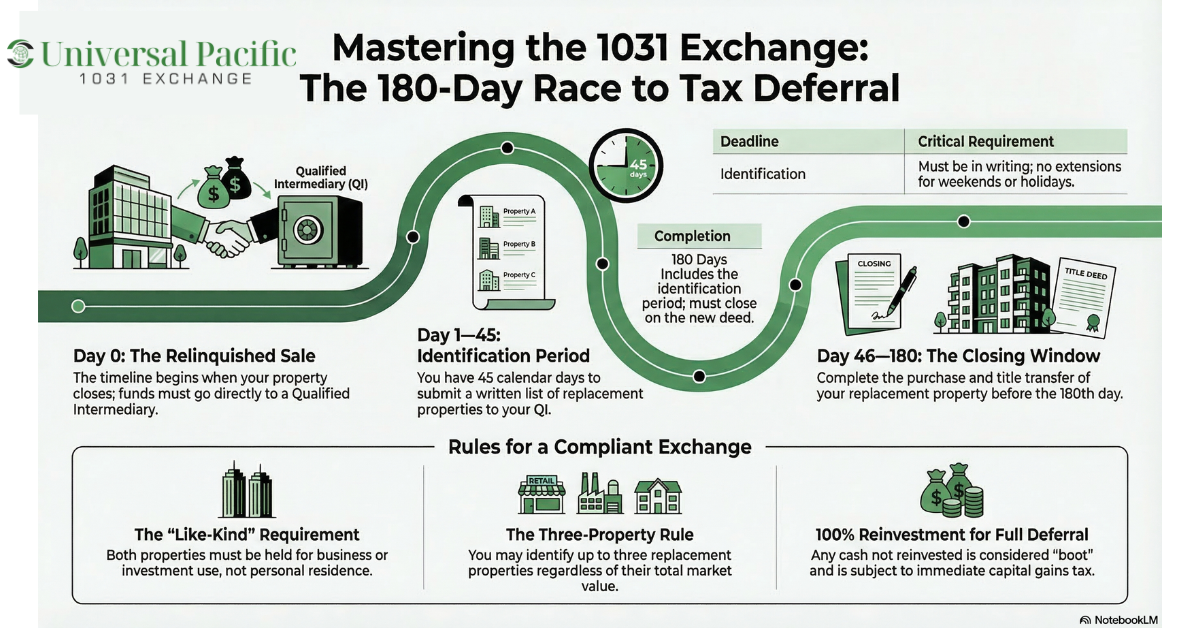

Day 0: Sale of the Relinquished Property

The 1031 exchange timeline starts ticking on the day you sell your relinquished property. You must transfer the proceeds to a Qualified Intermediary (QI), who will hold the funds until you purchase your replacement property. You are not allowed to receive or control the exchange funds at any point. If you do, the IRS will consider the sale as a taxable event, and the exchange will be disqualified. That’s why it’s important to learn how to find a qualified intermediary with the right experience and expertise to run a successful and compliant exchange.

Day 1 – 45: 45-Day Identification Period

From the day after you sell your relinquished property, you have exactly 45 calendar days to identify potential replacement properties. This deadline is strict, even if the 45th day falls on a weekend or holiday. You must submit your identified replacement property in writing to your QI before the deadline. Verbal agreements or informal notes do not count as official identification.

For a 1031 exchange with multiple properties, you can identify up to three properties or even more than three properties, provided that you follow either the three-property rule, 200% rule, or the 95% rule. For example, you can identify a single-family rental property, raw land, an apartment building, or any other commercial property. It is crucial to understand how each rule applies to the ‘equal or greater value’ requirement. Note that you’re not mandated to purchase all the identified properties, but you must purchase at least one of them.

During the identification period, you’ll need to work with real estate agents within the properties’ location to help find suitable listings. It’s recommended to also work with other professionals to help you evaluate the market value of the properties to be sure they align with your targets.

Day 45 – 180: Purchase the Replacement Property

After submitting your property identification, you have an additional 135 days to close on the purchase. The total timeframe for completing the 1031 exchange is 180 days from the sale of your relinquished property. The closing process must be fully completed within this period, including transferring ownership, recording the deed, and finalizing all payments.

Remember that any portion of the sale proceeds that is not reinvested is known as boot in a 1031 exchange, and is subject to capital gains tax. Additionally, if the replacement property has a lower mortgage balance than the relinquished property, the difference in debt will also be taxable. To avoid last-minute issues, it’s best to secure financing and conduct due diligence on the replacement property as early as possible. Many investors begin negotiating and arranging financing before the 45-day identification period ends to be sure they can close within the 180-day deadline.

File IRS Form 8824

Once your exchange is complete, you must report it to the IRS when filing your tax return for that year, using IRS Form 8824. The form provides details about the properties involved, the timeline, and how the exchange complies with 1031 rules. You can read our blog on how to file a 1031 exchange.

Filing incorrectly or missing required details can trigger IRS audits or penalties. To be sure everything is reported accurately, it’s best to work with a tax professional who has experience with 1031 exchanges. They can help you complete Form 8824 and verify that your exchange meets all legal requirements.

Consequences of Missing the 1031 Exchange Timeline

Missing the 1031 exchange timeline can have serious consequences, primarily resulting in the loss of the tax-deferral benefits that the exchange provides. The most significant consequences include the following:

- Immediate Tax Liability – This is the primary consequence of missing the 1031 exchange deadlines. You will owe capital gains tax on the profit from the sale of the relinquished property. If you claimed depreciation on the relinquished property, you must pay depreciation recapture taxes on the recaptured depreciation. These taxes can significantly reduce the proceeds available for reinvestment.

- Loss of Tax Deferral Opportunity – A 1031 exchange is designed to defer capital gains taxes, allowing you to reinvest the full sale proceeds into a new property. Missing the deadlines forfeits this opportunity, forcing you to pay taxes upfront.

- Financial Strain or Delays – Paying taxes immediately after the sale may strain your finances, especially if you were relying on the full proceeds for reinvestment. It may also delay your ability to close on a replacement property, particularly in competitive markets where quick action is often required.

- Increased Transaction Costs – A failed 1031 exchange could lead to additional costs, such as legal or qualified intermediary fees already paid for the exchange process, tax penalties, or interest charges if taxes are not paid promptly after disqualification.

Below is a table illustrating the key 1031 exchange deadlines and their implications.

| Deadline Name | Duration | Description | Consequence of Missing Deadline | Tips to Meet the Deadline |

| Exchange Start Date | Day 0 (the day the original property closes) | The exchange officially begins when the property you are selling closes. This date starts both the 45-day identification period and the 180-day exchange period. | If the exchange is not properly set up before the closing, the sale may not qualify for a 1031 exchange. | Plan the exchange early and choose a qualified intermediary before the sale of your property closes. |

| 45-Day Identification Period | 45 days after the sale closes | During this period, you must choose and list the property or properties you plan to buy as replacements. The list must be in writing and sent to the qualified intermediary. | If you do not identify replacement property within 45 days, the exchange will fail, and the profit from the sale may become taxable. | Start searching for replacement properties before the sale closes and list backup options in case your first choice does not work out. |

| 180-Day Exchange Period | 180 days after the sale closes (this includes the first 45 days) | You must complete the purchase of the replacement property within this time. This means the closing for the new properties must happen before the 180th day. | If the purchase is not completed within 180 days, the exchange becomes invalid, and you may owe capital gains taxes. | Work with lenders, agents, and inspectors early so the purchase process moves quickly. |

| Tax Return Filing Deadline | Usually, April 15 of the following year, unless you file an extension | If your tax filing deadline comes before the 180-day period ends, the exchange must be finished before you file your tax return unless you request an extension. | Filing your taxes before the exchange is completed can end the exchange period early. | File a tax extension if needed so you can use the full 180 days to complete the exchange. |

| Property Identification Documentation Deadline | Within the 45-day period | The list of replacement properties must be written, signed, and delivered to the qualified intermediary within 45 days. | If the identification is late or not done correctly, the exchange can be rejected even if you have found a property. | Prepare the identification document early and confirm that the intermediary received it before the deadline. |

How to Avoid Missing the 1031 Exchange Deadlines

Careful and strategic planning and execution is essential to ensure your exchange complies with the strict IRS timelines. Here are some ways you can manage your tax-deferred exchange to minimize time-related challenges.

- Work with a qualified tax advisor and other experienced professionals, such as legal experts, qualified intermediaries, etc., to ensure compliance.

- Understand the IRS timeline requirements and monitor deadlines closely.

- Conduct proper research, such as property inspections, title searches, etc., to assess the property.

- Identify backup replacement properties in case your primary choice falls through.

- If you’re looking to finance the potential replacement property, secure financing before the 180-day deadline to avoid delays.

- Maintain an accurate record of all transactions and communications related to the 1031 exchange. This will help with tax reporting and ensure you meet IRS requirements.

How a Qualified Intermediary Helps You Avoid Missing Exchange Deadlines

The qualified intermediary plays various important roles in helping you keep to the exchange timelines and comply with other requirements. To start with, the QI helps make sure the exchange remains valid by holding the proceeds from the relinquished property sale in a secure escrow account. The QI also reviews the investor’s property identification list to confirm it meets IRS requirements, reducing the risk of errors that could lead to disqualification.

Once the investor selects a replacement property, the QI coordinates with the seller, title company, and escrow agents to complete the purchase within the 180-day deadline. The QI releases the exchange funds only when all conditions are met, ascertaining that the transaction complies with IRS guidelines. This structured process prevents delays that could cause the investor to miss the final deadline.

Many property owners face unexpected challenges during a 1031 exchange, such as financing delays, failed property inspections, or changing market conditions. The QI helps investors navigate these challenges by advising on backup property options, potential delays, and alternative strategies to stay within the 1031 exchange timeline.

After the exchange is completed, the QI provides documentation and records to help the investor or their tax advisor properly complete the form, ensuring IRS compliance and avoiding audit risks.

Potential Pitfalls and Delays in the 1031 Exchange Timeline

Sometimes, real estate investors might find it challenging to identify and secure a business or investment property that both qualifies as like-kind and aligns with the investors’ goals. Market conditions and property availability can also make it difficult to find a suitable replacement property within the 45-day identification period.

Legislative Update: The Tax Cuts and Jobs Act (TCJA) provisions affecting 1031 exchanges were made permanent under the One Big Beautiful Bill Act (OBBBA), signed into law in July 2025. Previous proposals to cap 1031 exchanges at $500,000 were not enacted.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.