How 1031 Exchanges Make Money: Tax Benefits in Real Estate

A 1031 exchange lets a real estate investor sell one investment property and roll the entire sale proceeds into another property of equal or greater value, with no federal capital gains tax due at the time of sale. The tax is deferred under Section 1031 of the Internal Revenue Code, so the investor keeps every dollar of equity working in the next deal instead of losing a chunk to the IRS.

Over a long career, the difference between a chain of taxable sales and a chain of deferred exchanges can be hundreds of thousands of dollars in additional buying power, and the tax consequences of each decision compound through investment real estate portfolios in ways that are easy to underestimate. Investors who learn to defer capital gains taxes through 1031 exchanges create a meaningful advantage in long-term wealth building.

If you’ve been considering a 1031 exchange but have been hesitant because of the rules, deadlines, and paperwork involved, Universal Pacific 1031 Exchange can help simplify the process. Our experienced team guides investors through every step of the exchange, helping ensure compliance with IRS requirements while making the transaction as smooth and efficient as possible. Contact us today to get started.

This article explores what a 1031 exchange means, a step-by-step process for executing a seamless transaction, and the significant tax benefits of a 1031 exchange.

What Is a 1031 Exchange

A 1031 exchange, also called a like-kind exchange or a tax-deferred exchange, is a transaction defined under Section 1031 of the IRS tax code. It is a valuable tool that allows an investor to swap one investment property for another and defer the capital gains tax and depreciation recapture that would otherwise be owed on the sale. A 1031 exchange differs from an ordinary sale and reinvestment in one important way. Investors sometimes describe the result as “tax-free,” but that is not accurate.

Tax-deferred exchanges defer the tax owed on the original property; they do not eliminate it. The deferred tax follows the investor into the new property and is paid only when the chain of exchanges ends. In a standard real estate transaction, the seller sells the property, pays taxes on the gain, and reinvests what is left. In a 1031 exchange, the qualified intermediary holds the proceeds, the investor never touches the cash, and the entire sale amount flows into the replacement property. That structural difference is what produces the tax deferral and the larger pool of capital the investor can put to work.

Tax Benefits of a 1031 Exchange

There are three major tax benefits of a 1031 exchange. The first is the deferral of capital gains taxes. When an investment property is sold for more than its adjusted basis, the gain is normally taxed at long-term capital gains rates (up to 20 percent federal), plus the 3.8 percent net investment income tax, plus state tax. A 1031 exchange defers all of these to the eventual sale of the replacement property. The tax is not erased, but the deferral preserves cash for reinvestment.

The second is the deferral of depreciation recapture. When a property has been depreciated for tax purposes over many years, the IRS taxes that depreciation back at a 25 percent rate on the final sale, called unrecaptured Section 1250 gain. A 1031 exchange defers this depreciation recapture along with the capital gains tax, and the new property’s depreciation deductions are reset under specific rules that a tax advisor can model.

The third is the elimination of immediate tax liability, which translates directly to more buying power. An investor who would have paid 30 to 35 percent in combined taxes on a $500,000 gain instead has the full $500,000 working in the next deal. The financial impact compounds when the investor uses a series of exchanges over many years.

Example Scenarios

The following are hypothetical scenarios used to illustrate how beneficial a 1031 exchange can be. Please note, these are not testimonials from actual clients.

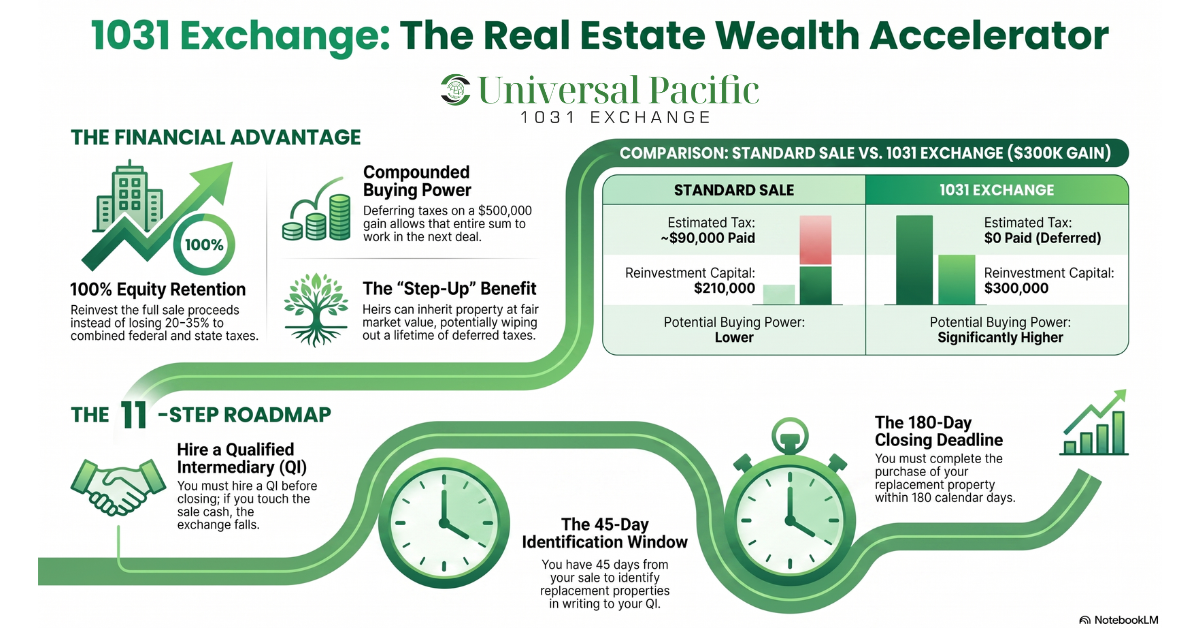

For the first example, let’s consider an investor named Alex who buys a small rental house for $300,000, holds it for ten years, and sells it for $600,000. Without a 1031 exchange, Alex pays roughly $90,000 in combined federal and state capital gains tax (more if depreciation recapture applies) and reinvests the remaining $510,000.

With a 1031 exchange, Alex defers the entire tax bill and reinvests the full $600,000 into a replacement property of equal or greater value. That $90,000 difference, combined with typical real estate financing, can support hundreds of thousands of dollars of additional purchase price. The result is more buying power and lower closing costs as a share of the deal compared with paying taxes upfront and reinvesting a smaller pool.

In this next example, let’s imagine an investor who exchanges every seven years across a thirty-year career, deferring roughly $100,000 in tax at each step. By the end of three exchanges, the deferred tax has been working as equity in real estate for two decades. The investor’s portfolio at retirement is materially larger than it would have been if each gain had been taxed at the moment of sale.

The numbers in any real transaction depend on the basis, the depreciation taken, the state of residence, and the financing on each property, which is why a tax professional should run the math before any decision.

Step-By-Step Guide to 1031 Exchanges

Performing a 1931 exchange can be quite complex, especially if it’s your first time or you’re dealing with multiple properties all by yourself. Below is a step-by-step process on how to execute a successful 1031 transaction.

Step 1: Contact a Qualified Intermediary Before Selling: You cannot receive the sale proceeds yourself if you want the exchange to qualify. Before closing the sale, hire a qualified intermediary (QI). The QI prepares the exchange documents and holds the money from the sale until you purchase your replacement property.

Step 2: Put Your Property on the Market and Find a Buyer: List your investment property for sale and negotiate with potential buyers. Once you accept an offer, inform all parties involved that the transaction will be part of a 1031 exchange.

Step 3: Sell Your Property: When the sale closes, the proceeds go directly to the qualified intermediary, not to you. This is a critical requirement because taking possession of the funds can disqualify the exchange.

Step 4: Start Looking for Replacement Properties: As soon as the sale closes, the exchange timeline begins. You should immediately start searching for properties that meet your investment goals and qualify under IRS rules.

Step 5: Identify Potential Replacement Properties Within 45 Days: You have 45 calendar days from the sale of your original property to identify potential replacement properties in writing. The identification must be submitted to your qualified intermediary and follow IRS guidelines.

Step 6: Perform Due Diligence on the New Property: Review financial records, inspect the property, evaluate market conditions, and confirm the investment fits your long-term strategy. This helps avoid costly mistakes before closing.

Step 7: Enter Into a Purchase Agreement: Once you choose a replacement property, sign a purchase agreement with the seller. Your qualified intermediary will coordinate the exchange paperwork and transfer of funds.

Step 8: Complete the Purchase Within 180 Days: You must close on the replacement property within 180 calendar days of selling your original property, or by your tax filing deadline if it comes first. Missing this deadline can make the entire exchange taxable.

Step 9: Reinvest All Exchange Funds: To receive full tax deferral, use all the proceeds from the sale and acquire a property of equal or greater value. Any cash you keep or debt you reduce may be taxable.

Step 10: Keep Records of the Entire Exchange: Maintain copies of closing statements, identification notices, exchange agreements, and other important documents. These records will be needed for tax reporting and future transactions.

Step 11: Report the Exchange on Your Tax Return: When filing your taxes, report the exchange using the appropriate IRS forms. Even though taxes are deferred, the transaction must still be disclosed to the IRS.

The Role of Qualified Intermediaries

A qualified intermediary, sometimes called an exchange facilitator, is required for any delayed 1031 exchange. The intermediary holds the sale proceeds between transactions, prepares the exchange agreement and related documents, and ensures the investor never has direct access to the funds. If the investor takes possession of the cash at any point, the exchange fails, and the gain becomes taxable.

The qualified intermediary cannot be the investor’s attorney, accountant, real estate agent, or anyone with a recent fiduciary relationship to them. The role demands independence, strong compliance practices, and financial controls to hold investor funds safely for months.

Universal Pacific has worked as a qualified intermediary for more than 32 years across multifamily, land, industrial, office building, and retail asset classes. The firm keeps exchange funds in segregated accounts, carries $2 million in errors and omissions insurance, and reviews every transaction in-house with licensed tax professionals before closing.

Meeting Legal Requirements

The IRS regulations governing 1031 exchanges are strict, and minor errors can disqualify the transaction. The four rules investors need to internalize. First, both the relinquished property and the replacement property must be held for productive use in a trade or business or for investment. Primary residence sales do not qualify.

Second, the properties must be of like kind, which for real estate is read broadly: vacant land for an apartment building, a single rental for a portfolio of properties, an office building for a retail center. Third, the investor must identify potential replacement properties in writing within 45 days of the sale and close on one or more within 180 days, with the 180-day clock also capped by the due date of the investor’s tax return that year. Fourth, the qualified intermediary must hold all sale proceeds throughout the exchange.

Maintaining proper documentation is the discipline that keeps an exchange defensible. The exchange agreement, the identification notice, the closing statements, and the records of the intermediary’s handling of funds should all be kept with the year’s tax return. IRS Form 8824 reports the exchange to the IRS.

How 1031 Exchanges Make Money in Real Estate

Successful real estate investing is not just about buying and selling properties; it is about keeping more of your profits working for you. A 1031 exchange helps investors move from one investment property to another while preserving capital for future growth. Below are some of the benefits of a 1031 exchange.

Portfolio Diversification Opportunities

A 1031 exchange is one of the few tools that lets an investor reshape a real estate portfolio without losing equity to taxes. An investor with a single large asset can split into multiple properties, exchanging one office building for a pair of smaller retail centers in different markets. An investor with several scattered small properties can consolidate, exchanging them for a single larger asset and reducing management responsibilities.

Diversification across property types is another use. An investor concentrated in residential rentals can move some equity into industrial or vacant land. Diversification across markets is just as important: a California property can be exchanged for a property in Texas, Florida, or Arizona, putting different parts of the real estate holdings in different real estate market conditions. The “same nature or character” standard for like-kind property gives investors wide latitude to reshape their portfolio across real estate transactions of very different types.

For investors who want exposure to institutional-quality real estate without active management, the Delaware Statutory Trust (DST) is an option recognized by the IRS as 1031-eligible. A DST holds a fractional interest in commercial real estate, and exchange proceeds can flow into DST interests as the replacement property. DSTs are not for every investor, since they offer no operational control, but they are a useful diversification tool when traditional replacement property is hard to find within the 45-day window.

Potential for Increased Cash Flow

Cash flow is often the practical reason property owners reach for an exchange. Real estate investors who track the tax basis on their properties exchanged know that receiving other property or cash creates a taxable boot, which is one of the few ways an exchange can produce an unexpected tax bill.

A property that produced good appreciation but weak rents can be exchanged for higher-value properties with stronger in-place income, often improving investment returns without raising the tax bill. A property that has been fully depreciated can be exchanged for a new property whose depreciation deductions are reset, providing fresh paper losses that shelter rental income.

Consider an investor who owns a long-held single-family rental in a high-cost coastal market. The property may have appreciated meaningfully, but it produces only a thin cap rate. By exchanging into a small multifamily property in a different market, the investor can lift their effective cash flow without taking a tax hit on the sale. Reinvestment of the full sale proceeds, with depreciation deductions on the new property’s higher basis, can transform the income profile of the portfolio.

Successful financial outcomes generally come from a disciplined reinvestment strategy, not from any single transaction. Identifying replacement assets that match the investor’s investment goals, financing them prudently, and resisting the urge to over-borrow are what turn the structural tax benefit into actual wealth. The properties involved in each exchange should align with the investor’s broader plan, not the other way around.

Long-term Financial Planning

Tax deferral compounds over time, which is why 1031 exchanges become more valuable the longer they are used. The math is straightforward. Money that would have gone to the IRS instead earns returns alongside the rest of the portfolio for years, sometimes decades. Even at a modest annual return, the deferred tax dollars can double or triple before they are ever paid.

The strategy can also dovetail with estate planning. When a real estate investor passes away holding real estate investment property, current federal tax law generally provides a step-up in basis to the property’s fair market value at death. Heirs inheriting the property may then sell with little or no capital gains tax, and the deferred tax burden built up over a lifetime of exchanges can effectively be wiped out. This combination of repeated 1031 exchanges during life with a step-up in basis at death is widely used in long-term real estate wealth planning.

The 1031 exchange is a powerful tax deferral strategy, but it works best inside a broader plan. A tax advisor and financial advisor can model how exchanges fit into the investor’s other investments and overall investment goals, and adjust the strategy as tax law and market conditions change.

Recent Updates to 1031 Exchange Rules

The most consequential change in modern times remains the Tax Cuts and Jobs Act of 2017, which narrowed Section 1031 to real property starting January 1, 2018. Since then, the core rules have stayed largely stable.

Several proposals have been floated to cap or limit 1031 exchanges, including a proposed cap on the deferred gain at $500,000 per taxpayer that appeared in Biden administration tax proposals in 2021. None of those proposals has been enacted into law as of this writing. Investors should pay attention to legislative developments, because future caps on Section 1031 would change the math for high-gain exchanges materially.

State-level rules also matter. California, in particular, has its own rules requiring continued tracking of deferred gains for state purposes when a California property is exchanged for property in another state. A tax professional familiar with the relevant states should review the multi-state implications before closing

The stability of the federal rules over the past several years has made 1031 exchanges a reliable planning tool, but the policy risk argues for using the strategy while it is available rather than waiting. Investors with significant gains in their current property and a long-term real estate horizon often benefit from acting on an exchange in the next planning window rather than deferring the decision indefinitely.

The practical adjustments are smaller than the headlines suggest. Investors should keep careful records, work with a qualified intermediary whose compliance practices stand up to IRS scrutiny, and maintain proper documentation of every step of the exchange process. These habits matter regardless of any future legislative change.

Start an Exchange Today

A 1031 exchange offers numerous benefits that go beyond a one-time tax saving, and the financial advantage compounds when investors apply the strategy across a long real estate career. Deferring capital gains taxes and depreciation recapture preserves equity, supports portfolio diversification, opens the door to higher value properties with stronger cash flow, and pairs effectively with estate planning.

The IRS rules are strict, the timelines are firm, and the cost of an error is the full tax bill, so proper planning and clean documentation are not optional. Before starting an exchange, investors should consult a qualified tax professional and engage a qualified intermediary with strong compliance practices.

Universal Pacific 1031 Exchange has over 30 years of experience in helping real estate investors smoothly navigate the process of a 1031 transaction. Our team will provide you with the necessary guidance, documentation, and support needed to meet IRS requirements, avoid costly mistakes, and complete your exchange with confidence. Reach out to us today to start an exchange.

Frequently Asked Questions

This section provides answers to common questions about how 1031 exchanges make money: tax benefits, real estate.

What Is a 1031 Exchange?

A 1031 exchange is a transaction under Section 1031 of the Internal Revenue Code that lets a real estate investor sell investment property and reinvest the sale proceeds into a like-kind property without recognizing the gain for federal income tax purposes in that year. The tax is deferred, not eliminated, and the deferred amount carries into the new property as a reduced tax basis.

How Do 1031 Exchanges Benefit Investors in Real Estate?

The principal benefit is the deferral of capital gains taxes and depreciation recapture at the time of sale, which keeps the investor’s full equity working in real estate. The strategy also enables portfolio diversification across property types and markets, supports moves from low-cash-flow to higher-cash-flow assets, and resets depreciation deductions on the replacement property. Used repeatedly over time, the deferral compounds into materially more buying power and a larger portfolio at retirement.

What Are the Tax Benefits of a 1031 Exchange for Investors?

The tax benefits include deferral of federal long-term capital gains tax (up to 20 percent plus the 3.8 percent net investment income tax), deferral of depreciation recapture at 25 percent, and deferral of applicable state tax in most cases. When combined with the step-up in basis at death under current federal law, the deferred tax can be substantially reduced or eliminated for the investor’s heirs. These tax benefits are why 1031 exchanges are considered a powerful tax deferral strategy in real estate investing.

How Can Universal Pacific Help Investors With 1031 Exchanges?

Universal Pacific is the qualified intermediary on the exchange. The firm holds the sale proceeds in segregated accounts, prepares the exchange agreement and required documentation, tracks the 45-day and 180-day deadlines, and coordinates with the investor’s attorney, accountant, and real estate agents through closing. With more than 32 years of experience and a focus on the complex reverse exchange and improvement exchange structures, Universal Pacific helps investors satisfy the IRS rules without sacrificing their broader investment strategy.

Are There Specific Rules and Timeframes to Follow for a Successful 1031 Exchange?

Yes, and the IRS does not extend them. The investor must identify potential replacement properties in writing within 45 days of selling the relinquished property, and must close on one or more of the identified properties within 180 days of that sale. Both deadlines are firm regardless of weekends or holidays, and the 180-day clock is also capped by the due date of the investor’s tax return, including extensions. The exchange must use a qualified intermediary, the properties must be held for investment or business use, and the transaction must be reported to the Internal Revenue Service on Form 8824.

What Types of Properties Can Be Exchanged Under Section 1031?

Real estate held for productive use in a trade or business or for investment qualifies, including rental property, vacant land, an office building, an industrial warehouse, a retail center, and similar real property. A primary residence does not qualify, since it is not held for investment. A vacation home used mainly for personal purposes generally does not qualify either. Since the Tax Cuts and Jobs Act took effect in 2018, personal property and intangibles no longer qualify, even though they did before.

Disclaimer: This article is for general educational purposes and does not constitute tax or legal advice. A qualified intermediary handles and documents a 1031 exchange but does not provide tax or legal advice. IRS rules and state rules can change, and every transaction depends on its own facts. Investors should consult a licensed tax professional before starting an exchange.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise is invaluable for complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise is invaluable for complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.