Maximizing Tax Benefits Through Like-Kind Exchange Partnership Interest

If you own real estate through a partnership or LLC and you want to defer the capital gains taxes on a sale, you have probably hit the same wall most investors do: a partnership interest itself does not qualify for a 1031 exchange. Some partners want to roll into the next property, others want cash, and the structure that lets every partner reach their own goal is not obvious. There are real, IRS-tested ways to get the deferral, but each one demands careful planning and clean execution. The right path depends on the partnership agreement, the timeline, and how much risk of IRS scrutiny each partner is willing to accept.

At Universal Pacific 1031 Exchange, we have served as a qualified intermediary on partnership-level 1031 exchanges for years, including drop and swap structures, swap and drop arrangements, tenancy-in-common conversions, and Delaware statutory trust acquisitions. Our team works directly with your tax advisor and your real estate attorney to align the partnership agreement, the timeline, and the IRS regulations so the exchange stands up to audit. Contact us today for guidance on the right structure for your partnership and your investors.

This guide explores like-kind exchanges for partnership interests, the special requirements for a deferred exchange, and common partnership issues and their solutions.

Understanding Like-Kind Exchanges of Partnership Properties

A like-kind exchange of partnership-held property is possible, but the property has to move correctly, and the partnership interests themselves cannot be the thing exchanged. Before moving on, let’s first understand what a 1031 exchange is.

A like-kind exchange under Internal Revenue Code Section 1031 lets a taxpayer sell investment real property and acquire like-kind replacement property while deferring the capital gain. The relinquished property and the replacement property must both be real property held for investment or for use in a trade or business. The taxpayer cannot receive the cash proceeds at any point during the exchange process.

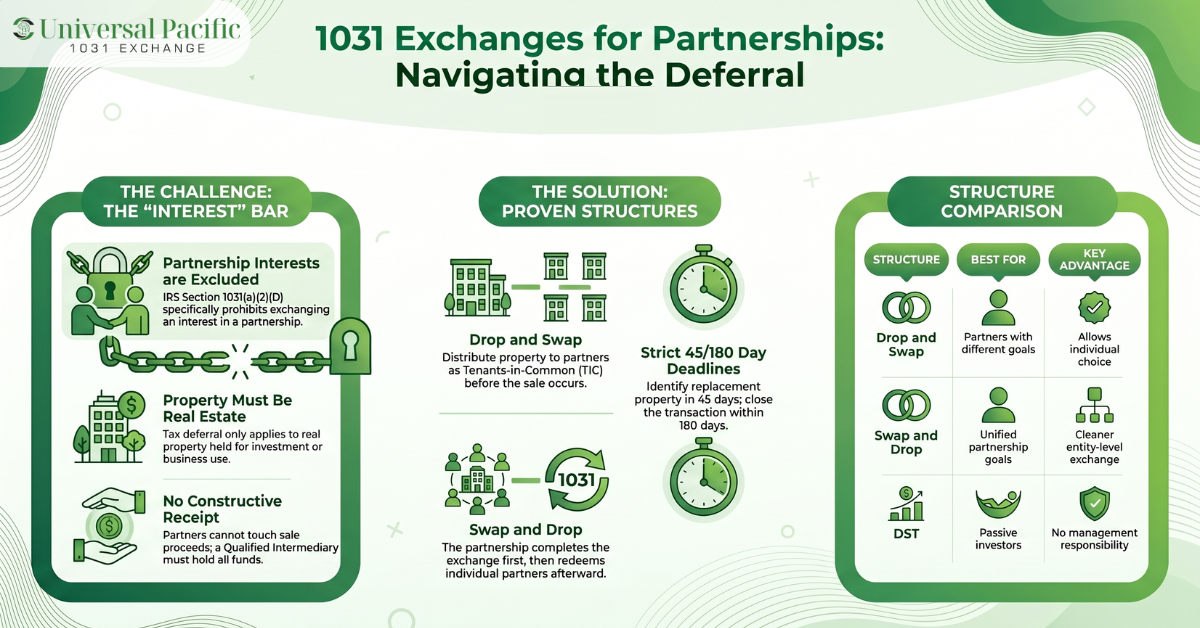

Real property owned by a partnership or LLC is eligible for a 1031 exchange when the partnership itself is the taxpayer for the entire exchange. The 45-day identification and 180-day exchange deadlines apply, and a qualified intermediary must hold the funds. If different partners want different outcomes, the partnership cannot simply give some partners cash and have others continue the exchange without restructuring first.

One major benefit of a 1031 exchange is deferring federal capital gains tax and deferring the unrecaptured Section 1250 depreciation recapture (taxed at up to 25 percent). It also helps in preserving capital for the next acquisition and supporting long-term portfolio growth. For partnerships with appreciated property, the equity saved from taxes can fund a larger or higher-quality replacement property.

Deferred Exchange Special Requirements

For a deferred 1031 exchange, real estate investors must follow several special requirements to preserve their tax-deferred status. These rules govern how the exchange is structured, including strict identification and acquisition deadlines, the use of a qualified intermediary, and limitations on receiving sale proceeds. Failing to meet any of these requirements can disqualify the exchange and trigger immediate tax consequences.

Timeline and Identification Rules

The taxpayer has 45 days from the closing of the relinquished property to identify replacement properties in writing and 180 days to close. Both deadlines run from the same date. The Internal Revenue Service does not extend them for ordinary delays. For partnership exchanges, the deadline is the same whether the taxpayer is the partnership or, after a restructuring, individual partners.

Role of Qualified Intermediaries

The IRS rules require a qualified intermediary on virtually every delayed 1031 exchange. The intermediary holds the exchange proceeds, prepares the exchange documents, avoids actual or constructive receipt by the taxpayer, and manages the entire real estate transaction. Choosing a qualified intermediary with experience in partnership-level transactions is critical, because the documents and the timing of any restructuring must coordinate.

Special Considerations for Partnerships

When a partnership holds the property, the partnership is the taxpayer. If some partners want to exchange and others want to cash out, the partnership has to restructure before the sale, distribute the property in a way the IRS will recognize, or use a special allocation that does not break Section 1031.

Common Partnership 1031 Exchange Structures

Partnership Issues in 1031 Exchanges

The biggest issue is partner disagreement. One partner may want a redemption and to receive cash, others want to buy replacement property, and any structure that distributes cash to redeemed partners can affect the others. Some partners may prefer a special allocation under the partnership rules, while others want a clean disposition. Other partners may want to swap into different replacement properties, which the partnership cannot do as a single taxpayer.

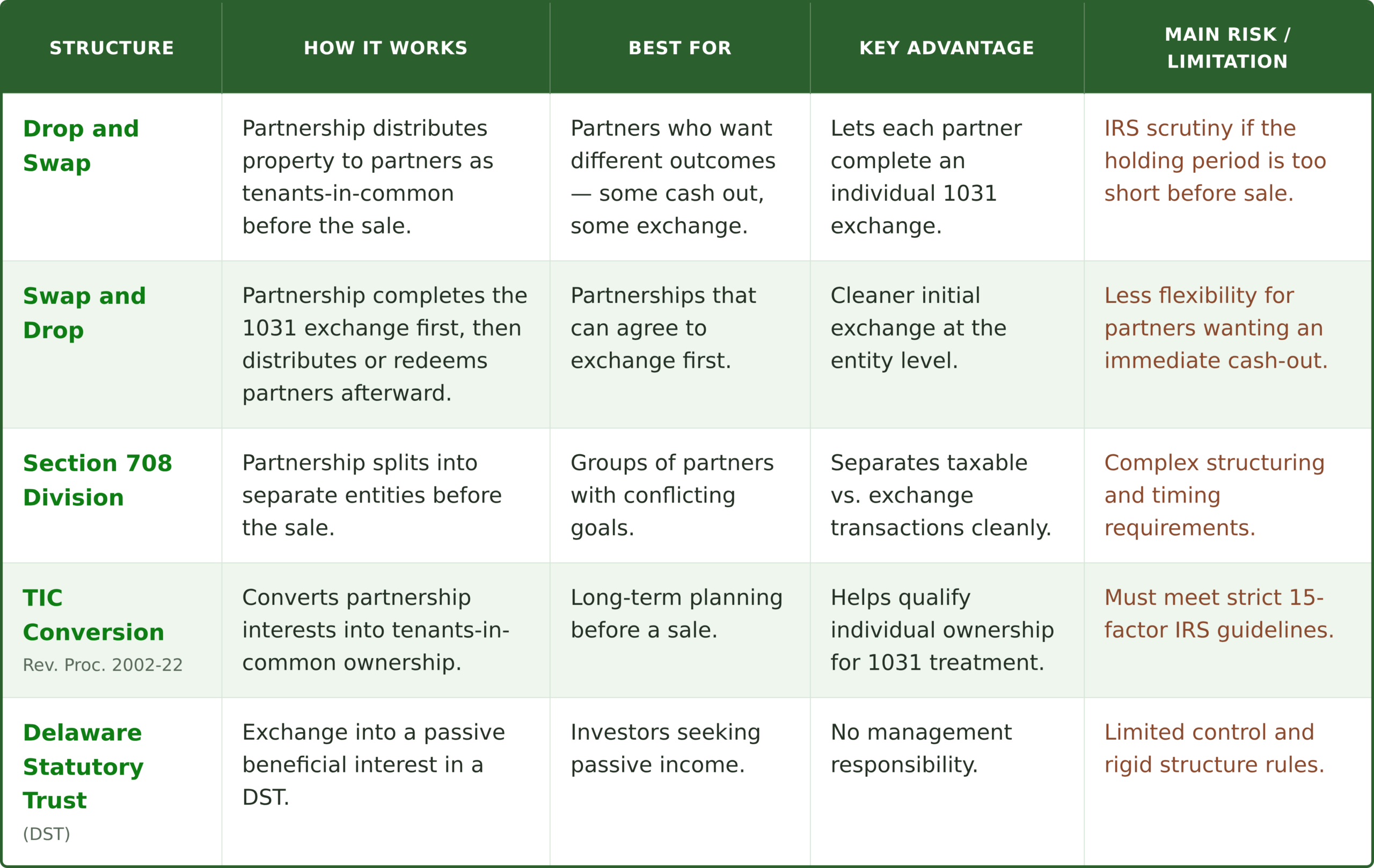

Three structures can help in most situations. The first is a drop and swap, which distributes the property to the partners as tenants in common before the sale, so each owner does an individual 1031 with the share they kept. The second is called a swap and drop. In this strategy, partners complete the 1031 first and then redeem any partners who want out, which is more conservative on holding period but harder to execute when partners disagree. The third is a partnership division under IRC Section 708, which separates the partners into two partnerships, one that exchanges and one that sells. Each option benefits from early planning and clean documentation.

Case Scenarios

To better understand a 1031 exchange partnership structure, let’s take this example. Imagine a three-partner LLC owns an apartment building, and two partners want to defer through a 1031 while one wants to cash out. The LLC distributes a tenant-in-common interest to each partner ahead of the sale. The two continuing partners use their TIC interests in their own 1031 exchanges; the third partner sells the TIC interest for cash and pays tax.

A second example comes from the New York case involving Benjamin and Rachel Hadar and Ruth Shomron, who were partners in a real estate partnership that owned an apartment building on Central Park West in Manhattan, New York City. Before the property was sold, the partnership distributed ownership interests to the partners as tenants in common (TICs) on the same day as the transaction.

The New York Division of Tax Appeals concluded that the partners’ TIC interests were held for investment and therefore qualified for Section 1031 exchange treatment. While the decision provides support for certain “drop and swap” transactions, it is not binding outside New York, and the IRS has not formally endorsed the ruling. As a result, investors should view same-day distributions and sales as a higher-risk strategy that requires careful planning.

Tax Implications of Like-Kind Exchanges for Partnership Interests

A valid 1031 exchange defers capital gains tax and the unrecaptured Section 1250 gain for federal tax purposes. The transaction is tax-deferred, not tax-free, and the deferred amounts carry over into the tax basis of the replacement property. The new basis equals the relinquished property’s adjusted basis plus any cash invested, less any cash received.

Beyond the immediate tax consequences, investors should also consider how an exchange may affect the underlying partnership structure. The partnership agreement may not contemplate a restructuring or a partner buyout, and the timing of distributions can affect Section 704 allocations. Updating the agreement before the sale to authorize a TIC distribution, a partnership division, or a special allocation prevents disputes and supports the IRS analysis later.

These planning considerations are important because the tax benefits of a 1031 exchange are deferred into the future rather than eliminated altogether. Because tax is deferred, the future tax liability on the new property reflects the lower carried-over basis. When the replacement property is eventually sold without another exchange, the deferred gain and the deferred depreciation recapture come due.

As Justin Bergman, the co-founder of Universal Pacific, would say, “A partnership 1031 exchange is not about whether investors qualify; it’s about whether the structure is built correctly before the sale. Once the property is sold, the flexibility disappears, and the tax consequences are locked in.”

Many investors plan to exchange repeatedly and eventually pass property to heirs, who may receive a stepped-up basis. The possibility of repeated tax deferral over decades is one reason 1031 exchanges remain central to long-term real estate planning, and partnerships that specially allocate gains can use this to align partner outcomes.

Can a Partnership Interest Be Exchanged in a Like-Kind Exchange?

No. Section 1031(a)(2)(D) of the Internal Revenue Code specifically excludes partnership interests from like-kind exchange treatment. After the Tax Cuts and Jobs Act, Section 1031 also applies only to real property, so the question is settled twice over. A partner cannot exchange a partnership interest for another partnership interest, for real property, or for a TIC interest and claim Section 1031.

However, there are certain alternatives. The accepted workarounds focus on the underlying real property rather than the partnership interest. Drop and swap distributes the property out as tenant-in-common interests, which qualify as real property under Revenue Procedure 2002-22 when 15 factors are met. Swap and drop runs the exchange at the partnership level first. Delaware statutory trust interests acquired as replacement property are treated as direct real property under Revenue Ruling 2004-86, subject to the trustee restrictions known as the seven deadly sins. A partnership division under Section 708 splits the entity into separate entities and supports a partial transfer of property so different groups of partners can pursue different exit strategies. Each path requires planning well before any sale.

Need Help Structuring a Partnership 1031 Exchange?

A partnership interest cannot be exchanged directly under Section 1031, but partnerships can still defer tax on real estate sales with the right structure. Failed exchanges become taxable events with full tax consequences, including any debt secured against the property and any excess cash received as boot. Drop and swap, swap and drop, partnership divisions, TIC interests under Revenue Procedure 2002-22, and DST interests under Revenue Ruling 2004-86 each offer a path, and each comes with planning, timing, and audit considerations.

The biggest risks are partner disagreement and aggressive timing on a drop and swap. Plan the structure well before any sale, document each step, and work with a qualified intermediary who has handled partnership-level exchanges. Contact Universal Pacific to evaluate the right approach for your situation.

Universal Pacific 1031 Exchange has over 30 years of experience with partnership-related 1031 exchanges, including complex drop and swap, swap and drop, and DST acquisitions. Our team is committed to helping investors protect capital, navigate IRS regulations, and complete exchanges that hold up under audit. Contact us today to book a free consultation or start an exchange.

Frequently Asked Questions (FAQ)

Below are answers to common questions about like-kind exchanges partnership interests.

What Is a Like-Kind Exchange of Partnership Interest?

There is no direct like-kind exchange of a partnership interest, because Section 1031(a)(2)(D) excludes partnership interests and post-TCJA Section 1031 applies only to real property. The phrase usually refers to a 1031 exchange of real property held by a partnership, with structures like drop and swap that let partners reach their individual goals.

How Does a Like-Kind Exchange of Partnership Interest Benefit Investors?

A properly structured partnership-related exchange defers federal capital gains tax, depreciation recapture, and often state-level capital gains tax. The deferred amounts stay invested in the next property, which supports long-term portfolio growth.

Is There a Time Limit for Completing a Like-Kind Exchange of Partnership Interest?

Yes. The taxpayer has 45 calendar days to identify replacement property and 180 calendar days to close, measured from the relinquished property’s closing. For late-year sales, the 180-day deadline is shortened to the federal tax return due date unless an extension is filed.

Are There Specific IRS Rules Governing Partnership Interest Exchanges?

Yes. Section 1031(a)(2)(D) excludes partnership interests directly. Revenue Procedure 2002-22 governs TIC arrangements, Revenue Ruling 2004-86 governs Delaware statutory trust interests, and the IRS scrutinizes drop and swap timing for evidence that each partner held the property for investment.

Can Investors Engage in Multiple Like-Kind Exchanges Involving Partnership Ownership Structures?

Yes. Many investors complete repeated exchanges over decades, sometimes using a partnership division to separate existing partners from continuing ones. Each exchange transaction must independently meet the Section 1031 requirements, including the qualified intermediary rule, the timeline, and the rule that property be exchanged solely for like-kind property of equal or greater value, with no liquidation of partnership interests treated as a credit toward the exchange.

Disclaimer: This article is for general informational purposes only and does not constitute tax or legal advice. A qualified intermediary handles and documents a 1031 exchange but does not provide tax or legal advice. IRS regulations, Revenue Procedures, and Tax Court decisions can change, and every exchange depends on its own facts. Consult a licensed tax professional before starting an exchange.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.