Rental Property Tax Deferral: 1031 Exchange in the Same Year

Most real estate investors sell a rental property and buy a replacement property in the same calendar year. A 1031 exchange lets them defer capital gains taxes on that sale, as long as they follow the IRS rules and use a qualified intermediary. The money that would have gone to taxes stays invested in the next property. With the help of a QI, you can stay compliant with IRS rules while ensuring your taxes stay deferred.

Universal Pacific 1031 Exchange assists real estate investors and other taxpayers with navigating the complexities of 1031 exchanges while helping them meet critical IRS requirements and deadlines. With decades of experience serving clients nationwide, we provide qualified intermediary services designed to facilitate smooth transactions and support long-term tax deferral strategies. Contact us today to start an exchange.

This guide explains how a same-year 1031 exchange works, what qualifies, the deadlines, and the mistakes that can cost an investor the tax deferral.

Can You Complete a 1031 Exchange in the Same Tax Year?

Yes. You can sell one investment property and buy a replacement property in the same year and still defer capital gains taxes. In fact, this is the most common 1031 exchange of all. An investor who sells in March and closes on a new property in June has completed a same-year exchange.

One point matters most. A 1031 exchange is tax-deferred, not tax-free. You postpone the tax, you do not erase it. That difference is explained in more detail below. The timing turns on two IRS deadlines that start the day your relinquished property closes:

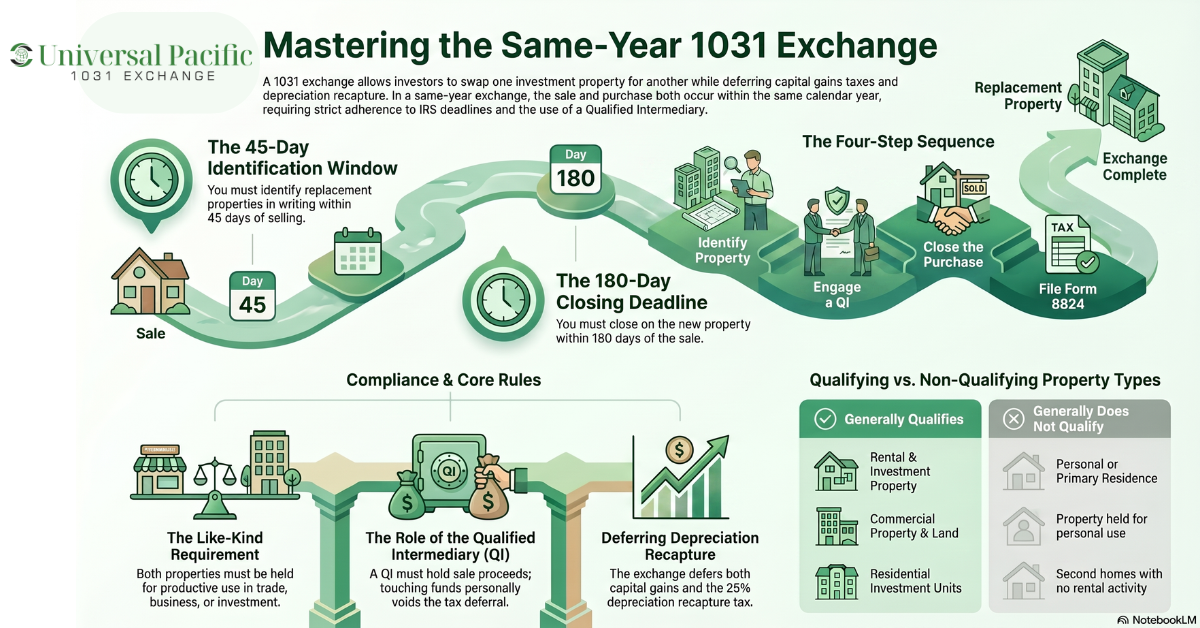

- You have 45 days to identify replacement properties in writing.

- You have 180 days to close on the replacement property.

When you sell early in the year, both deadlines fall inside the same calendar year, so the exchange is simple. When you sell late in the year, the 180-day period can run past the date your tax return is due. The IRS gives taxpayers a deadline that is the earlier of 180 days or the tax return due date for the year of the sale. To keep the full 180 days, you file a tax return extension on Form 4868. Investors who skip that step can lose weeks of their exchange period and put the entire tax deferral at risk.

Understanding 1031 Exchange Rules and Regulations

A 1031 exchange, named after IRC Section 1031, lets you swap one investment property for another and defer the capital gains taxes you would normally owe on the sale. The rules are strict, and small errors can disqualify the exchange.

Like-Kind Property Requirement

Both the relinquished property and the new property must be like-kind property. This means they must be held for productive use in a trade or business or for investment. For real estate, like-kind is broad. You can exchange a rental house for an apartment building, raw land for a commercial property, or a duplex for a retail unit. Since 2018, only real property qualifies. Personal property and partnership interests no longer count.

Time Frame for Exchange

The 45-day identification period and the 180-day exchange period run at the same time, not back to back. Both are calendar days, and the IRS does not extend them for weekends or holidays. Missing either deadline ends the deferral and makes the gain taxable.

Role of Qualified Intermediaries

https://docs.google.com/spreadsheets/d/1SxwZLaLb5tr7ahpaEXhr3OwC7VARrK-vKnSKILWLq2E/edit?usp=sharingA qualified intermediary is required. The investor cannot touch the sale proceeds at any point. If you receive the exchange funds, even briefly, the IRS treats the sale as a taxable event. The qualified intermediary holds the proceeds, prepares the exchange documents, and transfers the funds to buy the new property. This is the single most important safeguard in the exchange process.

What Properties Qualify for a Same-Year 1031 Exchange?

The property must be held for investment or business use. The table below shows what generally qualifies and what does not.

| Generally Qualifies | Generally Does Not Qualify |

| Rental property and investment property | Personal residence or primary residence |

| Commercial property and land | Principal residence |

| Residential real estate held for investment | Property held primarily for personal use |

| Mixed-use property (the investment portion) | A second home with no rental activity |

A vacation home can qualify under a safe harbor in Revenue Procedure 2008-16. For each of the two years after the exchange, the owner must rent the home at fair market value for at least 14 days and limit personal use to 14 days or 10 percent of the days it was rented, whichever is greater. A true personal residence never qualifies, because it is not held for investment.

Step-by-Step Guide to Completing a 1031 Exchange

The exchange follows four steps. Each one has its own compliance points.

Step 1: Identify Potential Replacement Properties

Start the search before you sell. Within 45 days of closing, you must name your replacement properties in writing. Do your due diligence early on price, condition, and rental income, because the clock does not stop while you negotiate.

Step 2: Engage a Qualified Intermediary

Hire the qualified intermediary before you close the sale. The intermediary sets up the account that holds the exchange funds and keeps the proceeds out of your hands. Choosing a reputable intermediary protects both your money and your tax deferral.

Step 3: Close on the Replacement Property

The intermediary uses the held funds to buy the new property and complete the transfer to you. To defer all of the tax, the purchase price of the replacement property should equal or exceed the value of the property you sold. Any leftover cash is taxable.

Step 4: File the Necessary Tax Documents

Report the exchange to the IRS on Form 8824 with the tax return for the year of the sale. The form lists the properties, the dates, and the deferred gain. File on time, or file an extension if your exchange runs into the next year.

Tax Implications of a 1031 Exchange in the Same Year

A 1031 exchange keeps more capital working for you instead of sending it to the IRS.

Deferring Capital Gains Taxes

Capital gains taxes apply to the profit when you sell an investment property for more than your adjusted basis. A 1031 exchange defers that tax, so the full proceeds roll into the next property. The potential tax savings can be large, and they improve cash flow and buying power on the new purchase. The deferred gain carries into the replacement property and stays deferred until you sell without another exchange.

Impact on Depreciation and Recapture

Depreciation recapture is the part investors forget. Over the years you own a rental, you deduct depreciation, which lowers your taxable income but also lowers your basis. When you sell, the IRS taxes that recaptured depreciation. This unrecaptured Section 1250 gain is taxed at a federal rate as high as 25 percent. A 1031 exchange defers depreciation recapture along with the capital gains, because the old basis carries over to the new property. The tax is not gone. It becomes due when you eventually sell the replacement property in a taxable sale.

Reverse and Improvement Exchanges

Two variations help in special situations. A reverse exchange lets you buy the replacement property before you sell the old one, using an exchange accommodation titleholder to hold title until your sale closes. The IRS recognized this structure in Revenue Procedure 2000-37. An improvement exchange lets you use exchange funds to build or improve the replacement property before you take title. Investors use these when the market moves fast or when the new property needs work to match the value of the property they sold.

Common 1031 Exchange Mistakes

The mistakes below cause most failed exchanges.

- Missing the time limits: Blowing the 45-day or 180-day deadline ends the deferral.

- Mishandling exchange funds: Taking control of the proceeds, even for a day, makes the sale taxable.

- Improper identification: Vague or late property identification is rejected by the IRS.

- Related party transactions: Buying from or selling to a family member draws IRS scrutiny and has extra holding rules.

- Receiving cash boot: Any cash or debt relief you keep is taxable, even inside a valid exchange.

- Violating IRS guidelines: Skipping a qualified intermediary or filing the wrong forms can void the whole exchange.

Practical Examples

These examples show how the rules play out and what the tax consequences are.

Example 1: An investor sells one investment property in March and uses a qualified intermediary to buy a replacement property of equal value in June. Both legs close in the same year, the deadlines are met, and the entire capital gain is deferred. No tax is due now.

Example 2: An investor sells a rental property in November. The 180-day period would run past the April tax return due date, so the investor files a Form 4868 extension and closes on the replacement property within the full 180 days. The deferral holds because the deadline was preserved.

Example 3: An investor sells a property and has the proceeds wired to a personal account before buying the next one. Because the investor took control of the exchange funds, the IRS treats the sale as a taxable event. The capital gains taxes and depreciation recapture all become due, even though the investor intended an exchange.

Strategic Considerations for Same-Year 1031 Exchanges

Evaluating Market Trends

Study current market conditions before you sell. If replacement inventory is tight, line up strong candidates early so you are not forced into a weak property to beat the 45-day clock.

Financial Planning and Cash Flow Management

Budget for closing costs, financing, and other expenses that the exchange funds may not cover. Plan how the new property’s rental income will support your cash flow during the exchange.

Ensuring Compliance with IRS Guidelines

Compliance is not optional. Follow the IRS guidelines on deadlines, identification, and intermediary use exactly. This is where a qualified intermediary like Universal Pacific adds the most value, by keeping the documentation, deadlines, and funds in order so the exchange holds up.

Schedule a Consultation With Universal Pacific

A same-year 1031 exchange is a proven way to defer capital gains taxes and keep your equity working in real estate. Success depends on meeting the 45-day and 180-day deadlines, using a qualified intermediary, and following IRS guidelines to the letter. Remember that the tax is deferred and not erased, so plan for the day it may come due.

Because the rules are strict and the stakes are high, make tax planning part of your decision and talk with your tax advisor and a qualified intermediary before you start. The right preparation is what turns a tight timeline into a successful exchange.

Universal Pacific 1031 Exchange provides qualified intermediary services that keep your transaction compliant and your capital gains taxes deferred. Our team will review your timeline, your properties, and your goals, then handle the documentation and deadlines that protect your deferral. Contact us today to discuss your specific exchange and take the first step toward deferring taxes and protecting your real estate investment.

Frequently Asked Questions (FAQs)

This section provides answers to common questions about rental property tax deferral: 1031 exchange in the same year.

What Is a 1031 Exchange?

A 1031 exchange is a swap of one investment property for another that lets you defer capital gains taxes under IRC Section 1031. The IRS treats it as a continued investment instead of a sale. It applies only to real property held for business or investment, not to a personal residence.

What Are the Requirements for a Rental Property Tax Deferral 1031 Exchange in the Same Year?

You must exchange like-kind property held for investment, use a qualified intermediary, identify replacement properties within 45 days, and close within 180 days. Both the sale and the purchase can fall in the same year. To defer the full tax, the replacement property should cost as much as or more than the property you sold, and you cannot take any of the proceeds.

Can I Defer Taxes on a Rental Property Through a 1031 Exchange in the Same Year of Sale?

Yes. A same-year exchange is allowed and is the most common type. You sell the rental property and buy the replacement property within the same calendar year, and the capital gains taxes are deferred. Remember that the tax is deferred, not eliminated, and it comes due if you later sell without another exchange.

What Are the Potential Risks of a 1031 Exchange?

The main risks are missing a deadline, identifying property incorrectly, or touching the exchange funds, any of which can make the gain taxable. There is also market risk, since the 45-day clock can pressure you into a weak purchase. Working with an experienced, qualified intermediary reduces the compliance risks.

What Are the Timelines to Complete a 1031 Exchange in the Same Year?

You must identify replacement properties within 45 days of selling the relinquished property and close within 180 days. Both deadlines run from the same closing date and cannot be extended for ordinary delays. For a late-year sale, file a tax return extension so the 180-day window is not cut short by your filing date.

How Can Universal Pacific Assist With a Same-Year 1031 Exchange?

Universal Pacific serves as your qualified intermediary, the role the IRS requires for a valid exchange. The team holds the exchange funds, prepares the documents, and tracks your 45-day and 180-day deadlines so the deferral stays intact. That support is where most same-year exchanges are won, because it removes the errors that make a sale taxable.

How Does a 1031 Exchange Affect Long-Term Investment Strategy?

A 1031 exchange lets investors move equity from one property to another without losing value to taxes at each step. Over time, this can build a larger portfolio than selling and paying tax along the way. Some investors keep deferring through repeated exchanges and pass the properties to heirs, who may receive a stepped-up basis.

This article is for general informational purposes only and does not constitute tax or legal advice. A qualified intermediary handles and documents a 1031 exchange but does not provide tax or legal advice. IRS rules, Revenue Procedures, and tax rates can change, and every exchange depends on its own facts. Consult a licensed tax professional before starting an exchange.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise is invaluable for complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise is invaluable for complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.