What to Consider When Evaluating 1031 Exchange Properties

Most investors come to us with the same problem: too many potential properties on the table and a 45-day clock already ticking. Knowing what to consider when evaluating 1031 exchange properties before identification day is the difference between a successful exchange and an expensive mistake. Picking the wrong replacement property can wipe out the tax savings you were chasing in the first place. The questions that follow are the same ones we walk through with our clients at the desk.

At Universal Pacific 1031 Exchange, we have spent years guiding investors through replacement property selection, qualified intermediary coordination, and the technical requirements of the Internal Revenue Code. Our team supports investors across multifamily, retail, industrial, and net lease deals, and we have seen which evaluation habits separate a clean closing from a busted exchange. If you want a second set of eyes on a 1031 exchange you are planning, schedule a no-pressure consultation with our advisors.

This article explores what a 1031 exchange means, key factors to consider when evaluating properties for a 1031 exchange, and best practices for a successful like-kind transaction.

Understanding 1031 Exchange Basics

Named after Section 1031 of the Internal Revenue Code, a 1031 exchange allows a taxpayer to sell a relinquished property held for investment or productive use in a trade or business and reinvest the exchange proceeds into a new property of like kind.

This allows them to defer capital gains taxes that would otherwise be owed at the sale. The mechanism does not erase the taxable gain; it pushes it forward, letting the investor recycle equity that would have been paid out as tax. Used over decades, that compounding effect can meaningfully grow net worth.

Both the relinquished property and the replacement property must be real property held for investment purposes or business use. Primary residences, vacation homes used mostly for personal use, and inventory held by dealers do not qualify, and personal property has been outside Section 1031 since the 2017 tax law overhaul.

Like-kind exchanges between real estate assets are interpreted broadly: an apartment building can be swapped for raw land, a retail strip, or an industrial warehouse, as long as both sides are real estate held for investment. The fair market value of the new property should equal or exceed that of the relinquished property to defer the full taxable gain. Any other property considered must meet the same held-for-investment standard.

Tax Implications of 1031 Exchange

The tax implications of a 1031 exchange shape almost every evaluation decision you will make. Understanding how the IRS treats your exchange proceeds, your taxable gain, and your basis carryover lets you weigh candidate properties on real after-tax economics rather than headline price.

Maximizing Tax Benefits

To capture the full benefit of tax deferral, the investor needs to reinvest all of the exchange proceeds and acquire a replacement property of equal or greater value. Any reduction in debt must be offset by new debt or new cash on the replacement; unreplaced debt is treated as debt-relief boot. Any cash pulled out at closing is also boot (taxable proceeds you keep instead of reinvesting).

Net equity left behind, meaning equity not put back into the new property, also triggers a tax liability proportional to what was not reinvested. A $500,000 debt-replacement miss on a $2 million gain at a combined federal-plus-state rate near 30 percent can generate $150,000 of unintended capital gains tax exposure. Many investors miss this on the first pass and end up paying capital gains taxes they assumed had been deferred.

Understanding Capital Gains Tax

Sell an investment property outside a 1031, and the IRS taxes the capital gain plus depreciation recapture (the recovery of past depreciation deductions, generally taxed at up to 25 percent for real property). Stacked with federal, state, and Medicare surtaxes, the combined hit can approach a third of the gain.

A Ling and Petrova study summarized by the Federation of Exchange Accommodators found that the eventual tax recovery on deferred 1031 exchanges generates billions of dollars in federal revenue, evidence that the deferral is far from a giveaway: the government recovers the income later, often on a larger basis. For an investor weighing whether to exchange or simply sell, the comparison is the after-tax dollars available to reinvest now versus the deferred tax owed later.

IRS Regulations and Compliance

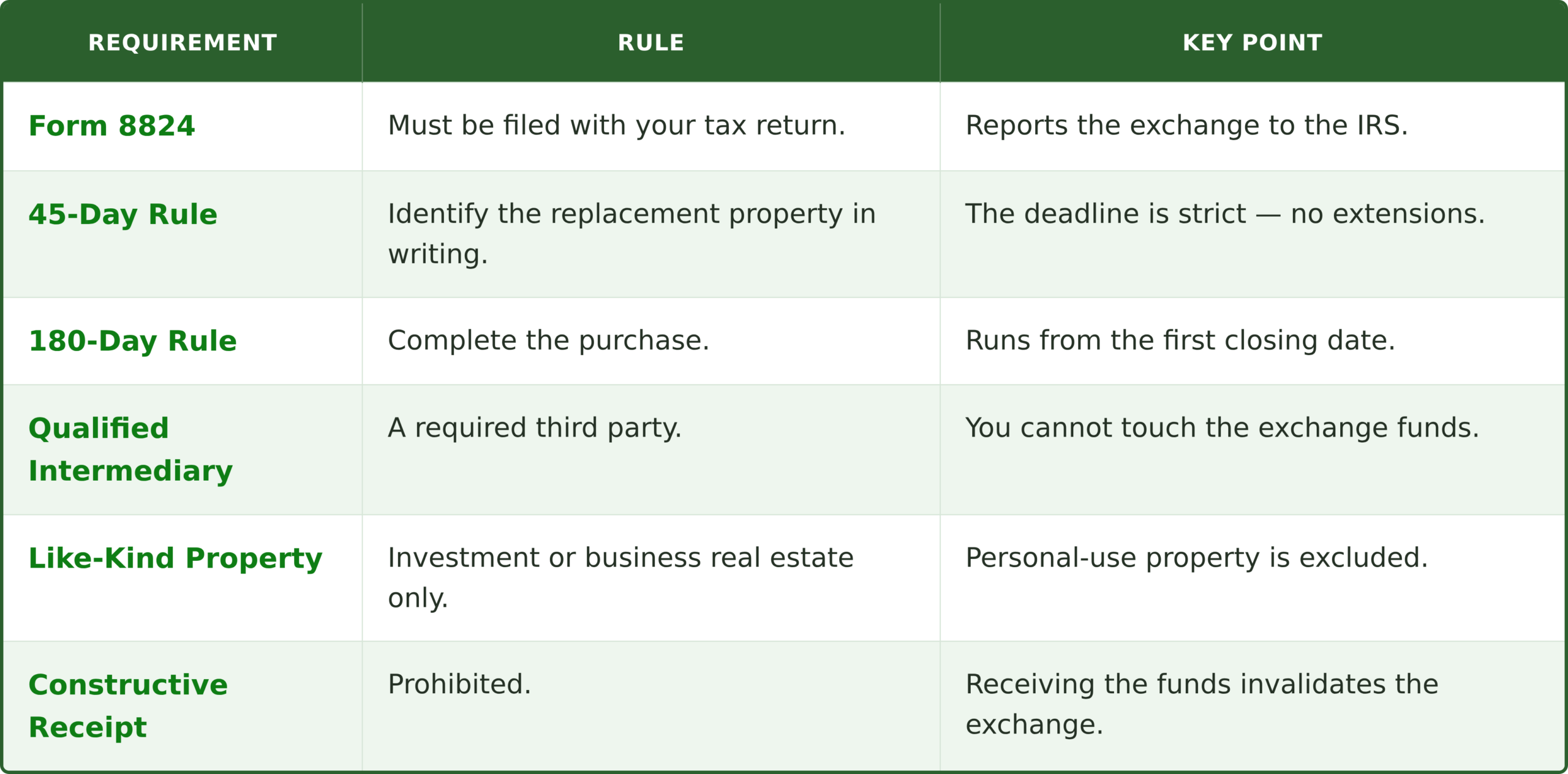

The IRS requires the exchange to be reported on Form 8824 (the Like-Kind Exchanges form) for the tax year of the relinquished sale, and the rules around constructive receipt are strict. Constructive receipt means the IRS treats you as having received the cash the moment you can access it, even if you do not touch it. If you, the taxpayer, take possession of any exchange funds, even briefly, the exchange typically fails.

A qualified intermediary holds the proceeds between sale and purchase to satisfy the qualified intermediary safe harbor at Treas. Reg. 1.1031(k)-1(g)(4), a set of conditions that prevent the IRS from treating you as having received the cash. The disqualified-person rule at Treas. Reg. 1.1031(k)-1(k) bars anyone who has acted as your attorney, CPA, real estate agent, broker, or employee within the prior two years from serving as your QI.

Careful planning around documentation, identification notices, and closing statements is what keeps the exchange clean and the tax deferral intact. Below is a simple table of the IRS 1031 exchange compliance rules:

Planning for a 1031 Exchange

Strong outcomes in a 1031 exchange almost always trace back to planning that began before the relinquished property hit the market. The investors who scramble in week three of the identification window are usually the ones who end up with a marginal replacement they would not otherwise have bought.

Strategic Planning Steps

Start by clarifying the long-term investment strategy behind the exchange. Are you consolidating ten smaller rentals into one institutional asset, diversifying out of one geography, trading management-heavy property for triple-net leases, or repositioning into a different property type?

Then pull together your team, which can include a real estate broker who understands exchange timelines, a CPA who has handled multiple Form 8824 filings, and a financial advisor who can model the after-tax outcome of each candidate. Get pre-approval on financing early, because lenders typically need extra time on exchange transactions. Begin identifying replacement property candidates before you list the relinquished property whenever possible.

Role of a Qualified Intermediary

The qualified intermediary plays a crucial role in every delayed exchange. Pick the wrong QI and the exchange dies. The QI prepares the exchange documents, takes assignment of the sale and purchase contracts, holds the exchange proceeds, and disburses funds at closing of the new property.

Choosing a QI is itself a due diligence exercise: review their bonding, segregated account practices, errors and omissions coverage, Federation of Exchange Accommodators membership, and track record. We coordinate directly with the intermediary on every transaction to keep documentation aligned across counterparties.

Timing Considerations

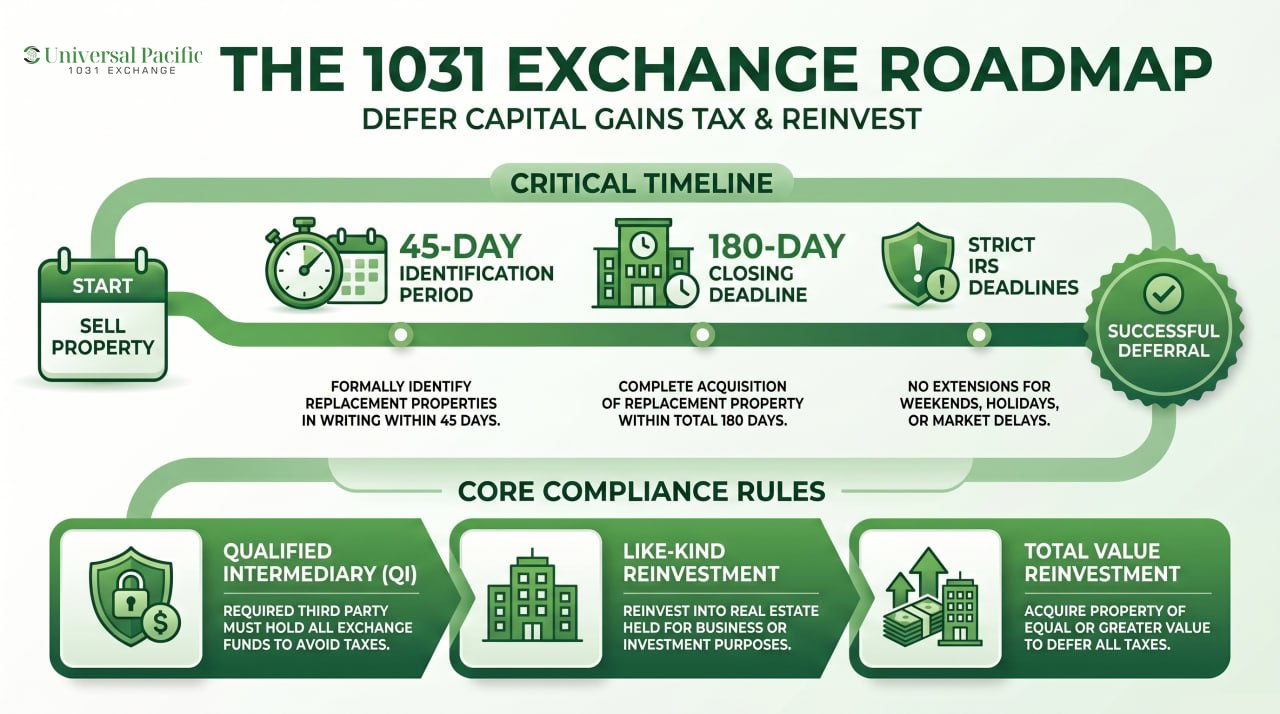

The two hard deadlines are 45 days to identify replacement properties and 180 days to complete acquisition, both running from the closing of the relinquished sale. There are no extensions for weekends, holidays, or storms in most cases, although Revenue Procedure 2018-58 grants relief in federally declared disaster zones. Under IRC Section 1031(a)(3)(B), the 180-day clock is actually the earlier of 180 days or the due date of your federal tax return for the year of the sale.

If your return is due before day 180, the IRS shortens the window to that due date unless you file a timely extension to preserve the full 180 days. However, note that the IRS does not give extensions except in the event of a federally declared disaster. Like Justin Bergman would say, “Timing and structure are everything in a 1031 exchange. Missing either one can turn a strong investment plan into a taxable event.” Timing also affects financing rate locks, inspection periods, and seller responsiveness; build a calendar that backs out from day 180.

Best Practices for 1031 Exchange

A successful exchange is rarely about one heroic decision. It is about applying a consistent evaluation framework to every candidate that crosses the screen.

Property Evaluation Criteria

When evaluating a replacement property, consider the after-tax cash flow, underwriting assumptions for rent growth and expense inflation, and whether the property type aligns with your overall investment strategy. You should also review the lease rollover schedule, ownership structure requirements, deferred maintenance needs, and how the property’s fair market rent compares to the current in-place rent. Consider an investor who is selling a fully depreciated apartment building and considering two replacements: a value-add apartment complex and a single-tenant net lease retail asset.

The apartment offers higher upside but heavier management; the net lease offers passive income but less rent growth. Neither is wrong, but the evaluation has to align with the investor’s net worth, cash needs, and risk tolerance. Confirm that title, survey, environmental, and rent roll diligence can realistically complete inside the exchange window. Have two candidate replacements on the table? Share the addresses with our team, and we will walk through the after-tax comparison with you.

Analyzing Market Trends

Evaluate where the local submarket sits in its cycle. The Federal Reserve’s commercial real estate price index showed prices down roughly 7 percent year over year through April 2025 before signs of stabilization appeared later in the year, with cap rates across sectors having widened 150 to 200 basis points since 2022 according to recent CBRE Cap Rate Survey data.

Markets that overshot during the low-rate era may still be repricing, while certain sun-belt industrial and necessity retail markets have already reset. Look at absorption, vacancy, new supply, and rent growth trends rather than relying on a single broker pro forma.

Risk Management in 1031 Exchanges

Risks in a 1031 exchange stretch beyond the property itself. A failed identification, a delayed closing on the relinquished sale, a financing fall-through, or an undiscovered title issue can each blow up the exchange. Build in backup identification options. The three identification rules under Treas. Reg. 1.1031(k)-1(c)(4) provide investors with several options for identifying replacement properties.

Under the three-property rule, you may identify up to three replacement properties regardless of their total value. Under the 200% rule, you may identify any number of properties as long as their combined value does not exceed 200% of the relinquished property’s sale price, while the 95% rule allows you to identify any number of properties if you ultimately acquire at least 95% of the total identified value.

Keep accounting fees, legal fees, and inspection budgets reserved, and pressure-test each candidate against a conservative downside case. The cost of carrying a marginal property for ten years is usually greater than the cost of paying capital gains taxes on a clean sale. If your identification window opens in the next 60 days, schedule a pre-identification strategy call so backup options are ready.

Location and Market Trends

Location and broader market trends often decide whether the replacement property compounds your wealth or merely shelters your tax bill.

Importance of Location in Property Selection

Location drives demand, financing availability, exit liquidity, and tenant quality. An investor moving exchange proceeds into a tertiary market may capture a higher initial yield but accept thinner buyer pools at exit. Consider an example where two retail centers trade at the same cap rate, one in a growing suburban corridor and one in a flat rural town.

The suburban asset will likely outperform on appreciation and refinancing optionality, even though the day-one cash yield is identical. Look at population growth, household income, employment diversification, and the local regulatory environment when ranking candidates.

Is It Time to Start Your 1031 Exchange Strategy?

Evaluating a 1031 exchange replacement candidate well comes down to clarity on strategy, discipline on diligence, and respect for the timeline. Capital gains taxes deferred should fund a better long-term position, not paper over a marginal property. Compliance with the Internal Revenue Code, careful coordination with a qualified intermediary, and honest evaluation of market trends together protect both the tax deferral and the underlying investment.

Universal Pacific 1031 Exchange helps investors think through these factors before identification day so the exchange supports the broader portfolio rather than constraining it. Our team advises clients through replacement property selection, exchange structuring, and qualified intermediary coordination on a regular basis. If you have a 1031 exchange on the horizon, reach out to initiate a transaction.

FAQs on 1031 Exchanges

Below are answers to common questions about what to consider when evaluating exchange properties.

What Is a 1031 Exchange?

A 1031 exchange is a transaction allowed by the Internal Revenue Code that lets an investor sell real property held for investment or business use and reinvest the proceeds into a like-kind replacement property while deferring capital gains taxes. It is not a tax elimination; it is a deferral that can be repeated across many investors’ careers.

What Are the Potential Tax Benefits of a 1031 Exchange?

The headline benefit is the ability to defer capital gains taxes and depreciation recapture that would otherwise be triggered at the sale. The ability to defer tax lets the investor keep more equity working in the next property. Used across multiple exchanges, this compounding effect can lift net worth materially compared with a series of taxable sales. The deferred tax becomes due upon a final taxable sale or, in some estate scenarios, can step up at death.

How Does the Timing of a 1031 Exchange Impact the Process?

Timing is the single most unforgiving element of the exchange process. The taxpayer has 45 calendar days from the closing of the relinquished property to identify candidate replacement properties in writing, and 180 calendar days to complete the acquisition. Missed deadlines cannot be cured. Build the exchange calendar before you sign the listing agreement and align broker, lender, attorney, and QI on those dates.

What Types of Properties Qualify for a 1031 Exchange?

Any real estate held for investment purposes or used in a trade or business can qualify, including apartment buildings, office, retail, industrial, raw land, certain leasehold interests of 30 years or more, and tenant-in-common interests. Personal use property such as a primary home or vacation home does not qualify, and personal property has been excluded since 2018. Certain exchanges involving Delaware Statutory Trust (DST) interests, a fractional interest in institutional real estate, can also qualify as like kind under IRS Revenue Ruling 2004-86. Reverse exchanges, where the investor acquires the replacement before selling the relinquished property using an exchange accommodation titleholder, are also allowed under Revenue Procedure 2000-37.

How Important Is Due Diligence When Selecting 1031 Exchange Properties?

Due diligence is non-negotiable on a compressed timeline. The taxpayer must verify title, environmental condition, lease rolls, tenant credit, capital expenditure needs, zoning, and financing terms inside the 45-day identification window. Professional advisors who already know your file can move faster than a team brought on at the eleventh hour. Skipping inspection to make a deadline is how an exchange ends up worse than paying the tax.

How Can an Investor Maximize the Benefits of a 1031 Exchange?

Reinvest all exchange proceeds and replace debt dollar for dollar, align the new property with a defined long-term investment strategy, lean on a qualified intermediary and experienced legal, tax, and brokerage counsel, and build a written evaluation framework before you start touring. The investors who get the most out of Section 1031 treat it as a long-running portfolio strategy rather than a one-off tax move.

The content above is provided for general informational purposes only and does not constitute legal, tax, or investment advice. Tax outcomes from a 1031 exchange depend on the specific facts of each transaction and the application of current IRS regulations. Universal Pacific does not provide legal or tax opinions, and reading this content does not create a client relationship. Consult a qualified tax advisor and licensed attorney before initiating any 1031 exchange.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.