Maximize Your Savings with a 1031 Exchange for Capital Gains

A 1031 exchange lets real estate investors sell investment property and roll the exchange proceeds into a like-kind property without paying capital gains taxes at the time of the sale. Done correctly, the capital gains and the depreciation recapture both stay deferred, and the full value of the equity keeps working in the next deal.

However, as beneficial as this tool is, it comes with strict IRS rules, deadlines, and structural requirements that leave little room for error. A missed deadline, an improperly identified replacement property, or the receipt of cash at the wrong stage of the transaction can cause the exchange to fail and trigger an unexpected tax bill.

For over 30 years, Universal Pacific 1031 Exchange has assisted real estate investors, business owners, attorneys, accountants, and real estate professionals in structuring successful 1031 exchanges. We work closely with all parties involved to facilitate a smooth process from start to finish. Contact us today to start an exchange.

This guide highlights 1031 exchanges, tax implications and their benefits, a step-by-step walkthrough of executing a successful exchange, and common mistakes to avoid when performing a like-kind exchange.

Understanding 1031 Exchange and Capital Gains Tax

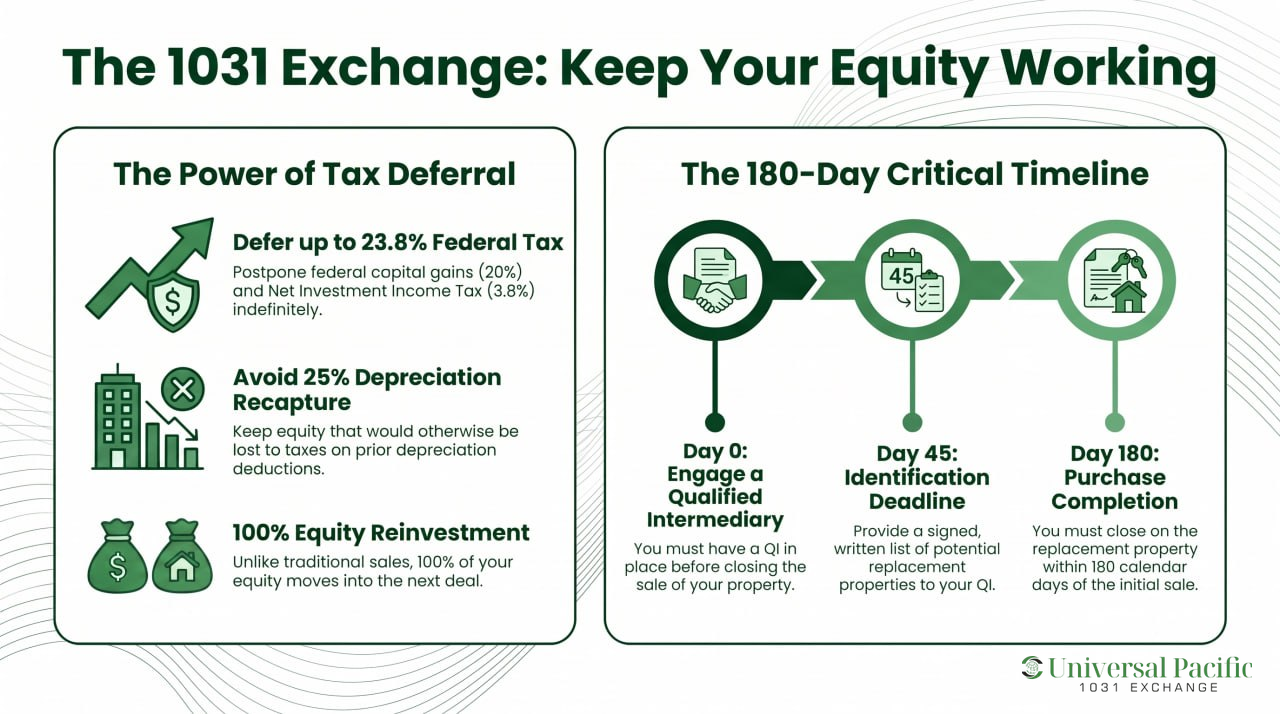

Capital gains taxes apply when you sell real estate for more than your adjusted basis in the property. For property held more than a year, long-term capital gains are taxed at 0, 15, or 20 percent at the federal level as of 2026, depending on taxable income, and an additional 3.8 percent net investment income tax can apply to high-income investors. State capital gains taxes stack on top, and California taxes capital gains as ordinary income.

Real estate also carries a second layer of tax on prior depreciation deductions. When you sell a depreciated property in a taxable sale, the unrecaptured Section 1250 gain is taxed at a federal rate of up to 25 percent. Investors who have owned a building for many years often face a recapture bill that rivals or exceeds the capital gains bill itself.

A 1031 exchange defers both. By exchanging one investment property for a like-kind property of equal or greater value through a qualified intermediary, the investor postpones the capital gains taxes and the depreciation recapture. The old basis carries into the new property, so the tax is deferred rather than erased, and it becomes due only if the investor later sells without another exchange. The practical benefit is significant. Preserving capital for reinvestment, supporting portfolio diversification, and compounding gains across decades all become possible when the IRS is not pulling a quarter of the equity out at every sale.

Key Differences Between 1031 Exchange and Traditional Sales

A traditional sale and a 1031 exchange look similar from the outside, but the tax consequences and the investment outcomes are very different. The table below summarizes the key contrasts for real estate investors deciding which path fits.

| Topic | Traditional Sale | 1031 Exchange |

|---|---|---|

| Tax treatment | Capital gains and depreciation recapture are due in the year of sale | Both are deferred when the like-kind exchange is properly structured |

| Use of proceeds | Free to use for any purpose, including personal use | Sale proceeds must flow through a qualified intermediary and into the replacement property |

| Property eligibility | No restriction | Real property held for investment purposes or use in a trade or business |

| Timing | No deadline | 45-day identification and 180-day exchange completion rules apply |

| Typical outcome | Full equity reduced by tax, less capital available to reinvest | Full equity available for reinvestment, with tax liability postponed |

For most real estate holdings, the exchange path keeps more capital working. For investors who genuinely want to exit the asset class or who need cash for personal use, the traditional sale is simpler. The choice usually comes down to whether the goal is to compound the portfolio or to cash out.

Step-By-Step Guide to 1031 Exchange

A successful exchange follows a clear sequence. Each step is governed by IRS regulations, and a misstep at any stage can disqualify the entire transaction.

Step 1: Determine Eligibility

The relinquished property and the new property must both be real property held for investment purposes or business property used in a trade or business. Since the Tax Cuts and Jobs Act took effect in 2018, the Jobs Act limited Section 1031 to real estate, so personal property and partnership interests no longer qualify. Like-kind here means properties of the same nature or character, not the same grade or quality.

Real estate properties that do qualify include rental houses, commercial property, office buildings, apartment buildings, raw land, vacant land, and many mixed-use assets. A primary residence does not qualify, and a beach house used for personal use generally does not qualify unless it meets the fair rental safe harbor under Revenue Procedure 2008-16. Property descriptions should reflect actual investment use, and a real estate attorney can confirm edge cases.

Step 2: Identify Replacement Property

Within 45 calendar days of the closing on the relinquished property, the investor must identify potential replacement properties in writing and deliver the identification to the qualified intermediary. Three identification rules are the most common. The three-property rule (identify up to three properties regardless of value).

The 200 percent rule (identify more than three properties as long as combined fair market value does not exceed 200 percent of the relinquished property’s fair market value). The 95 percent exception used in over-identified pools. Identify multiple properties when possible, because backup options matter when a deal falls through. Once the identified properties are submitted, the investor can only acquire from that list.

Step 3: Engage a Qualified Intermediary

A qualified intermediary must be in place before the relinquished property closes. The investor cannot touch the exchange funds at any point, even briefly. The qualified intermediary holds the sale proceeds in a segregated account, prepares the exchange agreement and assignment documents, and transfers the funds to acquire the replacement property.

Step 4: Close on the Replacement Property

Closing on the replacement property must occur within 180 days of the relinquished property’s sale. To defer all tax, the purchase price should be equal or greater in value than the property sold, and any cash or debt relief retained by the investor becomes taxable boot. Closing costs paid from exchange funds are generally allowed, though some closing costs may create boot if they are not standard transactional expenses.

Step 5: Report the Exchange on IRS Form 8824

The investor reports the exchange on Form 8824 with the federal tax return for the year of the sale. The form lists the properties involved, the dates, the values, and the deferred gain. Late reporting or missing documentation can trigger an audit, which is why working with a tax professional and a qualified intermediary together pays off.

Time Limits and Critical Deadlines

The 45-day identification window and the 180-day exchange period run at the same time, not back to back. Both are calendar days. The IRS does not extend them for weekends, holidays, or routine business delays. The only meaningful exceptions are federally declared disasters under Revenue Procedure 2018-58.

A subtle but important point for late-year sales: the 180-day deadline is the earlier of 180 calendar days or the due date of the federal tax return for the year of the sale, including extensions. Investors who sell in the fourth quarter often need to file Form 4868 to preserve the full 180-day window. Missing either deadline ends the deferral and converts the sale to a taxable event.

Role of a Qualified Intermediary

The qualified intermediary is the linchpin of the exchange. Section 1031 requires the investor to avoid actual and constructive receipt of the sale proceeds, and the qualified intermediary safe harbor under the regulations is the cleanest way to meet that requirement. The intermediary acquires the relinquished property and the replacement property from the investor, holds the exchange funds, and assigns the rights into the closing transactions.

Choosing a qualified intermediary is a serious decision. Look for written exchange agreements, segregated qualified escrow accounts, transparent fees, errors and omissions insurance, and operational depth. A weak intermediary can put the entire deferral at risk, including the rare scenario of an intermediary insolvency that traps client funds. Universal Pacific has been chosen by real estate investors for our depth on documents, deadlines, and compliance, and we communicate clearly at every step of the exchange process.

Common Exchange Structures

Most exchanges are delayed, but two other structures handle situations a simple delayed exchange cannot.

Delayed Exchange

In a delayed exchange (sometimes called a forward exchange or Starker exchange), the investor sells the relinquished property first and acquires the replacement property within 180 days. This is the standard structure and the one most investors use.

Reverse Exchange

In a reverse exchange, the investor acquires the replacement property before selling the relinquished property. An exchange accommodation titleholder holds title under the framework set in IRS Revenue Procedure 2000-37. Reverse exchanges are useful when the perfect replacement is available now, but the relinquished property has not sold yet. They are more complex and more expensive, and they still must close within 180 days.

Improvement Exchange

An improvement exchange lets the investor apply exchange funds to construct improvements on the replacement property before taking title. This structure helps when the available replacement asset is worth less than the relinquished property but can be built up to match value within the 180-day window.

Boot, Related Parties, and Common Mistakes that Invalidate Exchanges

Even strong exchanges fail when small details are mishandled. The mistakes below are the ones we see most often.

First, taking actual or constructive receipt of sale proceeds can derail an exchange. Even a brief detour into the investor’s personal account converts the sale to a taxable event. Likewise, receiving cash boot can create unexpected tax liability. Any cash left over after the purchase is taxable, even inside a valid exchange.

Similarly, receiving mortgage boot can trigger taxes. If the debt on the replacement property is less than the debt on the relinquished property, the debt difference is treated as taxable boot unless offset by additional cash invested. In addition, improper or late identification can invalidate an exchange. Vague property descriptions or identifications delivered after day 45 are rejected.

Another common mistake is missing the deadlines. The 45-day and 180-day timelines are strict. Likewise, mixing investment with personal use can create problems. A rental property converted to a primary residence too quickly after the exchange can lose qualification.

Furthermore, related parties without proper structure present additional risks. Section 1031(f) imposes a two-year holding period and other restrictions on exchanges with related parties such as a family member, a controlled entity, or other property owned by parties involved in the transaction. As a result, improperly structured related-party transactions can be unwound by the IRS.

Finally, cashing out a partnership interest can jeopardize tax deferral. The partnership entity, not the individual partners, must do the exchange. In addition, partnership interests themselves do not qualify since 2018.

Fortunately, a short consultation before closing usually catches these issues. Therefore, Universal Pacific reviews the structure of every exchange to flag boot, related-party concerns, and identification problems early.

Recent Updates to 1031 Exchange Rules

At the federal level, Section 1031 remains fully intact in 2026. The One Big Beautiful Bill, signed into law on July 4, 2025, considered but did not change Section 1031, and the like-kind exchange provisions were preserved as part of the final legislation. The TCJA limitation to real property remains permanent, and personal property still does not qualify.

State-level rules continue to evolve. In California, AB 1611 took effect on January 1, 2026, and prohibits corporations that own 50 or more single-family homes from using 1031 exchanges to defer capital gains taxes on those property types. Most real estate investors are not affected by this rule, but large institutional holders need to plan around it. Investors in any state should also watch for changes to state-level capital gains conformity, which can affect total tax due even when the federal exchange is fully compliant.

Potential Changes on the Horizon

Section 1031 has faced periodic proposals to cap or limit deferral, including the Biden administration’s earlier proposal to cap deferred gain at $500,000 per taxpayer. None of those proposals became law. The current political environment leaves the section stable, but investors planning multi-year strategies should monitor federal and state legislative developments and consult their tax advisor before relying on a future 1031 structure.

Maximizing Gains with Universal Pacific’s Strategy

Universal Pacific approaches each exchange as a strategic transaction, not a checklist. The team starts by aligning the timing of the relinquished and replacement closings, then maps the identification options against the investor’s broader real estate holdings.

Where a single replacement does not match the value, we plan multiple properties identified under the three-property or 200 percent rule. Where the value is off, we evaluate whether an improvement exchange can bridge the gap. The result is an exchange built to maximize the deferred capital gains while staying squarely within the Internal Revenue Service regulations.

For example, an investor selling an apartment building worth $3 million can identify three potential replacement properties: a smaller apartment building, an office building, and a parcel of vacant land. If the apartment building closes first at $2 million, the investor still has room to acquire the office building at $1 million within the 180-day window and defer the full gain. Without careful planning, the same investor might over-concentrate in one asset or miss a deadline.

Diversifying Your Portfolio

A 1031 exchange is one of the strongest tools for diversifying real estate portfolios because it lets investors trade out of a single asset class without losing equity to tax. An investor exiting a single rental house can move equity into a small commercial property and a parcel of raw land, spreading risk and improving cash flow.

An investor concentrated in one market can rebalance into a different metro. Diversification through exchanges preserves the tax deferral while shifting the underlying exposure. A practical approach: identify two or three lucrative properties in different property types or geographic markets. Use the three-property rule to keep flexibility, and aim for replacements where rental income and projected appreciation are both reasonable.

Utilizing Tax-Deferred Exchanges for Growth

A tax-deferred strategy compounds. Every time an investor exchanges rather than sells, the equity that would have gone to capital gains and depreciation recapture stays invested. Over a decade or more, that compounding can double the portfolio value compared with a path of taxable sales.

Some investors hold replacement properties for years, then exchange again into larger or higher-quality assets, and eventually pass the portfolio to heirs, who may receive a stepped-up basis. The combination of repeated exchanges and the step-up at death is one of the most powerful long-term wealth strategies available to real estate investors.

The strategy depends on disciplined execution. Each exchange must comply with the time limits, the qualified intermediary requirement, the identification rules, and the boot rules. A long-term plan that ignores any of those rules unwinds quickly. According to Michael Bergman, “The true advantage of a 1031 exchange is not just tax deferral, but the ability to keep your full equity working and growing in your next investment.” Universal Pacific helps investors execute the discipline year after year.

Are You Ready to Structure a 1031 Exchange?

A 1031 exchange is one of the most effective tools real estate investors have for deferring capital gains taxes and keeping equity working in the portfolio. Success depends on the basics: real property held for investment, a qualified intermediary in place before closing, replacement property of equal or greater value, written identification within 45 days, and closing within 180 days.

Recent legislation has preserved Section 1031 at the federal level, and the strategy remains a foundation of long-term real estate investing. Because the rules are strict and tax laws can change, work with your tax advisor and a qualified intermediary from the start.

If you are planning to sell real estate investment property and want to keep the capital gains tax deferred, the time to engage a qualified intermediary is before you close. At Universal Pacific 1031 Exchange, our team will review your timeline, the properties involved, and your investment strategies, then handle the documentation and deadlines that protect the deferral. Contact us today to discuss your specific exchange and take the next step toward preserving your real estate portfolio.

Frequently Asked Questions (FAQ)

This section provides answers to common questions about 1031 exchange capital gains.

What Are the Time Limits for a 1031 Exchange?

You have 45 calendar days from the closing of the relinquished property to identify replacement properties in writing, and 180 calendar days to close on the replacement. Both deadlines run from the same starting date. They are not extended for weekends or holidays, and the only routine exception is federally declared disaster relief.

Can I Use a 1031 Exchange to Defer Capital Gains on Investment Properties?

Yes. The core purpose of a 1031 exchange is to defer capital gains taxes on the sale of investment property, as long as the replacement is like-kind real property of equal or greater value, you use a qualified intermediary, and you meet the deadlines. Personal residences and property held for personal use do not qualify.

What Are the Rules for Identifying Replacement Properties?

The identification must be in writing, signed by you, and delivered to the qualified intermediary by day 45. Use one of the three identification rules: the three-property rule (any three regardless of value), the 200 percent rule (more than three as long as combined fair market value is under 200 percent of the relinquished property), or the 95 percent exception. Each identified property needs a clear description such as a street address or legal description.

What Is a 1031 Exchange?

A 1031 exchange, also known as a like-kind exchange, lets a real estate investor sell one investment property and acquire another like-kind property while deferring the capital gains tax and depreciation recapture that a traditional sale would trigger. It is named after Section 1031 of the Internal Revenue Code.

How Does a 1031 Exchange Help with Capital Gains Taxes?

By rolling the sale proceeds into a replacement property through a qualified intermediary, the investor postpones the federal capital gains tax (up to 20 percent plus a possible 3.8 percent NIIT), the unrecaptured Section 1250 depreciation recapture (up to 25 percent), and any state capital gains tax. The deferred amounts carry into the basis of the new property and become due only on a later taxable sale.

What Types of Properties Qualify for a 1031 Exchange?

Real property held for investment or business use qualifies, including rental houses, apartment buildings, commercial property, office buildings, vacant land, and raw land. Personal property and partnership interests do not qualify after the TCJA. A primary residence and a beach house used mostly for personal use also do not qualify, though a vacation property that meets the fair rental safe harbor in Revenue Procedure 2008-16 can qualify.

How Can Universal Pacific Assist with a 1031 Exchange?

Universal Pacific serves as your qualified intermediary across delayed, reverse, and improvement exchanges. The team holds the exchange funds in segregated accounts, prepares the exchange agreement and assignment documents, tracks the 45-day and 180-day deadlines, and coordinates with your tax professional, real estate attorney, and real estate agents to keep the transaction compliant. The role is procedural, and each exchange still depends on your own tax and legal advisors for personalized strategy.

This article is for general informational purposes only and does not constitute tax or legal advice. A qualified intermediary handles and documents a 1031 exchange but does not provide tax or legal advice. IRS regulations, Revenue Procedures, and tax rates can change, and every exchange depends on its own facts. Consult a licensed tax professional before starting an exchange.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.