Complete Guide to 1031 Rules for Universal Pacific Investors

While a 1031 exchange can be a profitable tool for real estate investors, the IRS regulations governing these exchanges are strict, and a single missed deadline can turn a tax-deferred exchange into a fully taxable sale. Because of this, investors need to understand the basic rules before starting the process.

Knowing what properties qualify, how the timelines work, and what steps must be followed can help prevent costly mistakes. With proper planning and the right support, a 1031 exchange can help investors grow their real estate portfolio while delaying capital gains taxes.

Universal Pacific 1031 Exchange has helped thousands of real estate investors, both experienced and new to the process, effectively navigate the rules and timelines involved in a successful 1031 exchange. We’ll guide you through the process step-by-step, helping you avoid mistakes that could result in tax consequences. Contact us today to get started.

This guide explains the key 1031 exchange rules investors need to understand before they begin a deferred exchange.

What Is a 1031 Exchange

A 1031 exchange is a tax-deferred transaction defined under code section 1031 of the Internal Revenue Code. It allows a taxpayer to swap one investment property for another and defer the capital gains taxes that would normally be owed on the sale.

The like-kind exchange provision first entered the U.S. tax code through the Revenue Act of 1921, where it covered a broad range of business and investment property. Like-kind exchanges have evolved through two main amendments since then. In 1984, Congress codified the strict timelines that still govern delayed exchanges, the 45-day identification period, and the 180-day exchange period. The Tax Cuts and Jobs Act, effective January 1, 2018, then limited Section 1031 to real property only. Personal property, equipment, vehicles, artwork, and partnership interests no longer qualify.

For real estate, the rule remains broad. Almost any real property held for productive use in a trade or business or for investment can be exchanged for almost any other real property held for the same purposes. An apartment building can be exchanged for raw land, a strip mall for an industrial warehouse, and so on, as long as both properties qualify under the rules.

Key 1031 Exchange Rules

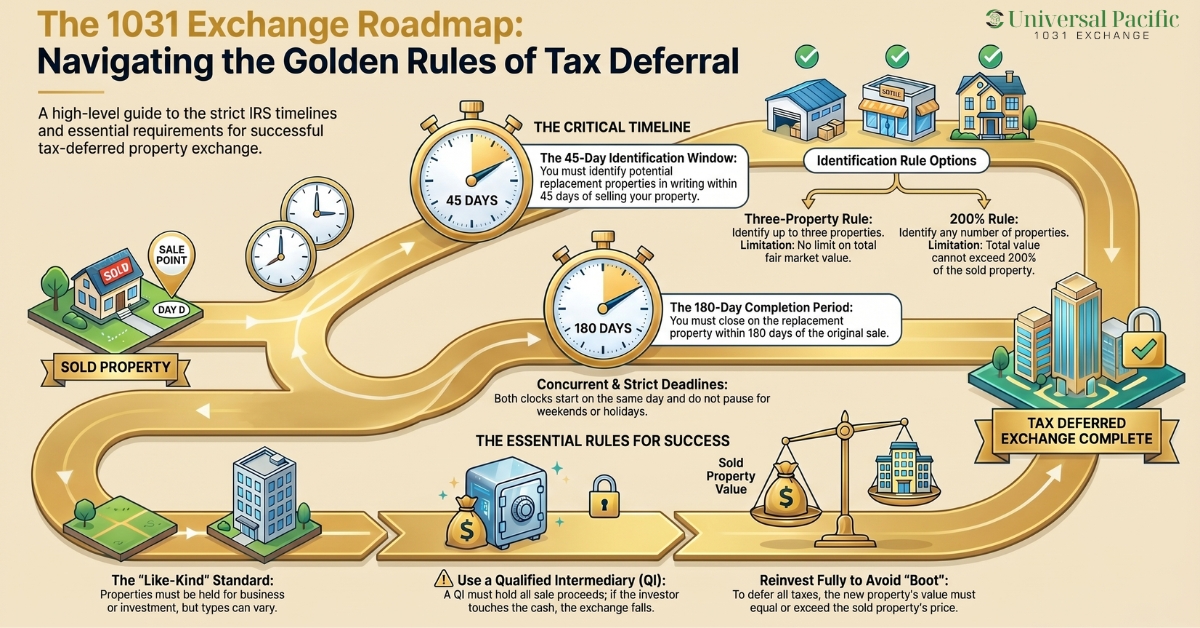

First, both properties must be like-kind. This means that they both must be held for business or for investment purposes. Real property held primarily for sale, such as a developer’s inventory or a house bought to flip, does not qualify. Neither primary residences nor vacation homes are used mainly for personal use. Real property in the United States is not like-kind to real property outside the United States, and the rule does not allow a U.S. property to be exchanged for foreign property.

Second, the IRS timelines are usually strict. When the taxpayer sells the relinquished property, the 45-day identification clock begins. From that same sale date, the investor has 180 days to close on one or more of the identified replacement properties. It is important to note that these two deadlines are not separate; instead, they run concurrently. The IRS does not extend either deadline for weekends or holidays. The exchange also has to wrap up by the due date of the taxpayer’s tax return for the year of the sale, including extensions, if that date comes before the 180th day.

Third, a qualified intermediary is required for any deferred exchange. The intermediary holds the sale proceeds, prepares the exchange agreement, and handles the legal paperwork. The taxpayer cannot take possession of the funds at any point, since the moment those funds touch the investor’s hands, the exchange fails, and the gain becomes taxable. The qualified intermediary also cannot be the investor’s attorney, accountant, or any party with a recent fiduciary relationship to the investor.

There are also rules for how many potential replacement properties the taxpayer can identify. The three-property rule lets the investor identify up to three properties, regardless of their fair market value. The 200% rule lets the investor identify more than three, as long as the combined fair market value of the identified properties does not exceed 200% of the fair market value of the relinquished property.

Benefits of 1031 Exchanges

The major benefit of the 1031 rules is the deferral itself. Deferring taxes through an exchange keeps the investor’s full equity working in real estate rather than shrinking with every sale. That larger pool of capital can compound over decades of holding and exchanging. The deferral generally extends to state income tax purposes as well, although the treatment varies by state.

The deferral also covers depreciation recapture, which often catches investors by surprise. When the eventual sale occurs without another exchange, the depreciation taken on the chain of properties carries forward and is taxed at ordinary rates. While the exchange continues, that liability is paused.

A 1031 exchange gives an investor the flexibility to move into a higher-value property without losing equity to taxes. A small rental can become an apartment building. A single asset can become several. Multiple properties acquired over time can be consolidated into one larger holding. The exchange does not strictly require the replacement property to be of equal or greater value than the original property.

However, if the investor wants to defer the full tax bill, the replacement property’s purchase price should equal or exceed the relinquished property’s sale price, and the investor should reinvest all of the sale proceeds. A shortfall in either creates “boot,” which is the portion of the transaction that becomes taxable.

For investors thinking long-term, repeated exchanges can shift the portfolio toward better markets, better tenants, or better cash flow, all while keeping the tax obligation paused. Many real estate investors use this structure as part of a multi-decade investment plan.

Used well, the 1031 rules support a strategic approach to wealth management that goes beyond any single transaction. Investors can diversify across geographies, consolidate to reduce management burden, or shift into property types that match their stage in life. Some investors use a series of like-kind exchanges to position assets for an eventual step-up in basis at death, which can wipe out the deferred capital gains entirely for heirs.

Step-by-step guide to 1031 Exchanges

Executing a successful 1031 exchange can be complex, especially for first-timers. Below is a step-by-step process on how to perform a seamless 1031 transaction.

Step 1: Preparation and Planning

A successful 1031 exchange starts before the relinquished property is even listed for sale. The investor should think through the tax consequences of selling, the type of replacement property they want, the financing they will need, and the timeline they can realistically meet. The first practical step is selecting a qualified intermediary.

The QI will be involved from the moment the relinquished property is sold, so the investor wants to choose one with strong compliance practices and clear insurance coverage. Cost matters, but it is rarely the right place to economize, since the QI is holding the investor’s money for months. The investor should also speak with a tax professional before listing the property, because the tax consequences of an exchange can interact with depreciation, prior carryovers, and state rules in ways that affect strategy.

Step 2: Identifying Like-Kind Properties

Once the relinquished property is sold, the 45-day identification clock begins. Within that window, the investor must identify the potential replacement properties in writing, sign the identification, and deliver it to the qualified intermediary. The identification has to describe each property clearly enough that there is no question what is being identified, usually by street address or legal description.

A practical tip: start the property search before the relinquished property is sold. The 45-day window is shorter than most investors expect, and finding the right replacement property quickly is the part of the process that derails the most exchanges. Investors who treat the search as an emergency after closing rarely find good options. Those who line up two or three candidates ahead of time give themselves room to negotiate and walk away.

The like-kind standard for real estate is broad, so the search does not have to be limited to identical properties. An investor selling a single-family rental can buy an apartment building, a commercial property, or undeveloped land held for investment, as long as the replacement property is held for productive use in a trade or business or for investment.

Step 3: Executing the Exchange

After identification, the investor has the remainder of the 180-day window to close on one or more of the identified properties. The qualified intermediary uses the held exchange funds to purchase the replacement property in the investor’s name, which completes the exchange process.

A few common pitfalls cause exchanges to fail at this stage. Receiving cash or other property that is not like-kind creates boot, which is taxable. Reducing the mortgage balance in the exchange without offsetting the difference with new cash creates a form of boot as well, since the IRS treats debt relief similarly to receiving cash. Buying a property of lesser value than the relinquished property creates boot equal to the shortfall.

Working with a tax professional through closing prevents these errors. Universal Pacific coordinates with the investor’s accountant, attorney, and real estate agents through the exchange to keep the transaction structured for full tax deferral, not partial deferral. The firm also documents the exchange in the records the investor uses to complete IRS Form 8824, which is the form the exchanged property must be reported on with the income tax return for that tax year.

Common Questions and Misconceptions

There are many misconceptions surrounding 1031 exchanges, especially when it comes to timelines, property eligibility, and tax deferral rules. Below are common answers and clarity to common questions and conceptions about 1031 exchanges.

What Are the Time Limits for a 1031 Exchange

The two most important time limits are the 45-day identification period and the 180-day exchange period. Both run from the sale date of the relinquished property. The 45-day rule requires the investor to identify potential replacement properties in writing within 45 days, and the 180-day rule requires the investor to close on the identified replacement property within 180 days. Missing either deadline ends the tax-deferred status of the transaction, and the gain on the sale becomes taxable in the year of the sale.

Investors sometimes assume these deadlines can be extended for unusual circumstances. They generally cannot. The IRS does not pause the clock for weekends, federal holidays, or even for the practical difficulties of finding the right property. A few narrow exceptions exist for federally declared disaster areas, but they should not be relied on as planning tools.

Can You Use a 1031 Exchange on Your Primary Residence

No. Primary residences do not qualify for a 1031 exchange because they are not held for productive use in a trade or business or for investment. A vacation home used primarily for personal purposes generally does not qualify either, although a vacation home that has been rented out and treated as an investment property may qualify if the personal use was minimal and the rental was genuine.

Homeowners selling a primary residence have a different tool available, the Section 121 exclusion, which allows up to $250,000 of gain on a primary residence to be excluded from tax, or up to $500,000 for married couples filing jointly, subject to ownership and use requirements. This is a separate provision from Section 1031, and it can be used by sellers who do not want or qualify for an exchange.

A related misconception is that a 1031 exchange is tax-free. It is not. The exchange is tax-deferred, and the deferred gain stays attached to the replacement property, becoming taxable when that property is eventually sold without another exchange.

Rules for Identifying Replacement Properties

A 1031 exchange does not limit the investor to one replacement property. An investor can identify and acquire multiple properties as long as they follow the identification rules. The three-property rule lets the investor identify up to three properties regardless of value. The 200% rule allows more than three properties to be identified, as long as their combined fair market value does not exceed 200% of the fair market value of the relinquished property.

Investors should be careful about exchanges with related parties. An exchange between related parties can be subject to a two-year holding requirement, after which selling either property within that window can disqualify the original exchange and trigger the deferred tax. Capital improvements made to the replacement property during the exchange can also be incorporated under an improvement exchange structure, but they must be planned for in advance with the qualified intermediary and structured correctly to count toward the exchange value.

Working With Universal Pacific on Your 1031 Exchange

The 1031 rules reward careful planning and punish small mistakes. Most failed exchanges are not the result of one big problem but of several small ones, a deadline missed by a day, a boot calculation overlooked, or an identification letter that was not specific enough. Working with an experienced, qualified intermediary is how investors who understand the rules turn that understanding into a clean transaction.

Universal Pacific is built for that kind of detail-heavy work. The firm has handled exchanges across every real estate asset class for more than three decades, with a focus on complex reverse and improvement exchanges where coordination across the parties involved matters most. Exchange funds are kept in segregated accounts, the firm carries $2 million in errors and omissions insurance, and every transaction is reviewed in-house by licensed tax professionals before closing.

If you are considering a 1031 exchange, the next step is to speak with a qualified intermediary and a tax professional before you list your property. Contact us to start an exchange today.

Frequently Asked Questions

Below are questions people are frequently asking about 1031 exchange rules and their respective answers.

What Is a 1031 Exchange

A 1031 exchange is a tax-deferred transaction under Section 1031 of the Internal Revenue Code. It lets a taxpayer sell an investment or business property and reinvest the sale proceeds in a like-kind replacement property without recognizing the gain for income tax purposes in that tax year. The deferred tax follows the investor into the new property and stays paused for as long as the chain of exchanges continues.

What Are the Basic Rules for a 1031 Exchange

Both the relinquished and replacement properties must be held for productive use in a trade or business or for investment. The properties must be like-kind, which, for real estate, is read broadly. The investor must identify potential replacement properties within 45 days of the sale and close on one within 180 days. The exchange must use a qualified intermediary, since the taxpayer cannot take possession of the exchange funds at any point during the exchange process.

Can Personal Property Be Exchanged in a 1031 Exchange

No. Since the Tax Cuts and Jobs Act took effect on January 1, 2018, Section 1031 applies only to real property held for productive use in a trade or business or for investment purposes. Personal property and intangible property, such as equipment, vehicles, artwork, partnership interests, and stocks, no longer qualify.

Are There Time Limits for Identifying Replacement Properties in a 1031 Exchange

Yes. The investor has 45 days from the sale of the relinquished property to identify potential replacement properties in writing, and 180 days from that same sale date to close on the purchase of the identified property. Both deadlines are firm and cannot be extended for weekends or holidays. The exchange must also be completed by the due date of the investor’s tax return for the year of the sale, including extensions, if that date is earlier.

What Are the Benefits of a 1031 Exchange?

The biggest benefit is deferring the capital gains taxes, which keeps the investor’s full equity working in real estate rather than draining a portion to tax with every sale. Investors can also use the exchange to consolidate or diversify their portfolio, move into properties acquired with stronger cash flow, or position assets for long-term wealth management. Used over many years, repeated exchanges can support significant growth that a series of taxable sales would not allow.

Disclaimer: This article is for general educational purposes and does not constitute tax or legal advice. A qualified intermediary handles and documents a 1031 exchange but does not provide tax or legal advice. IRS rules can change, and every transaction depends on its own facts. Investors should consult a licensed tax professional before starting an exchange.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise is invaluable for complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise is invaluable for complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.