A Complete Guide to the 1031 Like-Kind Exchange for Real Estate Investors

A 1031 like-kind exchange lets a real estate investor sell one investment property and reinvest the proceeds into another without paying capital gains taxes at the time of the sale. The tax is deferred, not erased, which gives investors a way to keep more capital working as they move from one property to the next. Named after Section 1031 of the Internal Revenue Code, this strategy has been part of U.S. tax law for over a century and remains one of the most widely used tools in real estate investing.

Universal Pacific 1031 Exchange has 35+ years of experience in helping real estate investors successfully navigate 1031 exchanges while preserving capital gains and supporting long-term investment growth. We assist clients through every stage of the exchange process, from preparing documentation to meeting IRS timelines. Contact us for a free consultation today.

This guide walks through how the exchange works, the IRS rules and deadlines that govern it, what property qualifies, and the mistakes that cost investors their tax deferral.

Introduction to the 1031 Like-Kind Exchange

A 1031 like-kind exchange is a tax-deferral mechanism written into Section 1031 of the Internal Revenue Code. When an investor sells an investment or business property and would normally owe capital gains tax on the profit, Section 1031 allows that tax to be postponed if the proceeds are reinvested into another qualifying property.

The purpose is straightforward. An investor who sells a rental property outright might lose a large share of the sale proceeds to federal and state capital gains taxes plus depreciation recapture. That smaller pool of money limits what they can buy next. A 1031 exchange keeps the full amount of equity invested in real estate, so the investor can move into a larger property, a different market, or a better-performing asset without the tax bill interrupting the process.

It helps to be precise about one point. A 1031 exchange defers capital gains taxes. It does not eliminate them. The deferred tax stays attached to the new property and becomes due if the investor eventually sells without completing another exchange.

History and Evolution

The like-kind exchange provision first entered the U.S. tax code through the Revenue Act of 1921. For decades, it applied to a broad set of assets, from real estate to equipment to other business property. Two changes shaped the modern version. In 1984, Congress codified the strict timelines that govern delayed exchanges, the 45-day identification period, and the 180-day exchange period that investors still work with today.

Then the Tax Cuts and Jobs Act, effective January 1, 2018, narrowed Section 1031 so that it applies only to exchanges of real property. Personal property and intangible property, such as equipment, vehicles, artwork, and partnership interests, no longer qualify. For real estate investors, the rules they follow now are the product of those two amendments.

Understanding 1031 Like-Kind Exchange Basics

A few terms come up repeatedly, and understanding them early makes the rest of the process easier to follow. The relinquished property is the property the investor sells. The replacement property is the property the investor buys to complete the exchange. Both must be held for business or investment purposes.

A qualified intermediary, often called a QI or exchange facilitator, is an independent third party that holds the sale proceeds between transactions and handles the exchange documentation. The investor is not allowed to take possession of the funds at any point. If they do, the exchange fails, and the gain becomes taxable. The QI cannot be the investor’s agent, attorney, accountant, or anyone else with a recent fiduciary relationship to them.

Boot is any cash or non-like-kind property the investor receives in the exchange. If an investor sells a property for $500,000 and buys a replacement for $450,000, the $50,000 difference is boot, and it is taxable. Boot also shows up when the investor reduces their mortgage debt in the exchange. Understanding boot is one of the more practical parts of planning an exchange well.

Benefits of a 1031 Like-Kind Exchange

The headline benefit is tax deferral on capital gains. By postponing the tax, an investor keeps their full equity invested and compounding rather than handing a portion to the IRS at each sale. There are other advantages that follow from that. An investor can use an exchange to diversify, trading a single large property for several smaller ones in different markets, or to consolidate, combining several properties into one.

An exchange can also improve cash flow, for example, by moving out of raw land that produces no income and into a leased commercial building that does. Some investors use repeated exchanges over many years as an estate planning strategy, because heirs who inherit the property may receive a stepped-up basis. The benefits are real, but they depend entirely on following the IRS rules correctly. A single missed deadline or a misstep with the proceeds can turn a tax-deferred exchange into a fully taxable sale.

How a 1031 Like-Kind Exchange Works

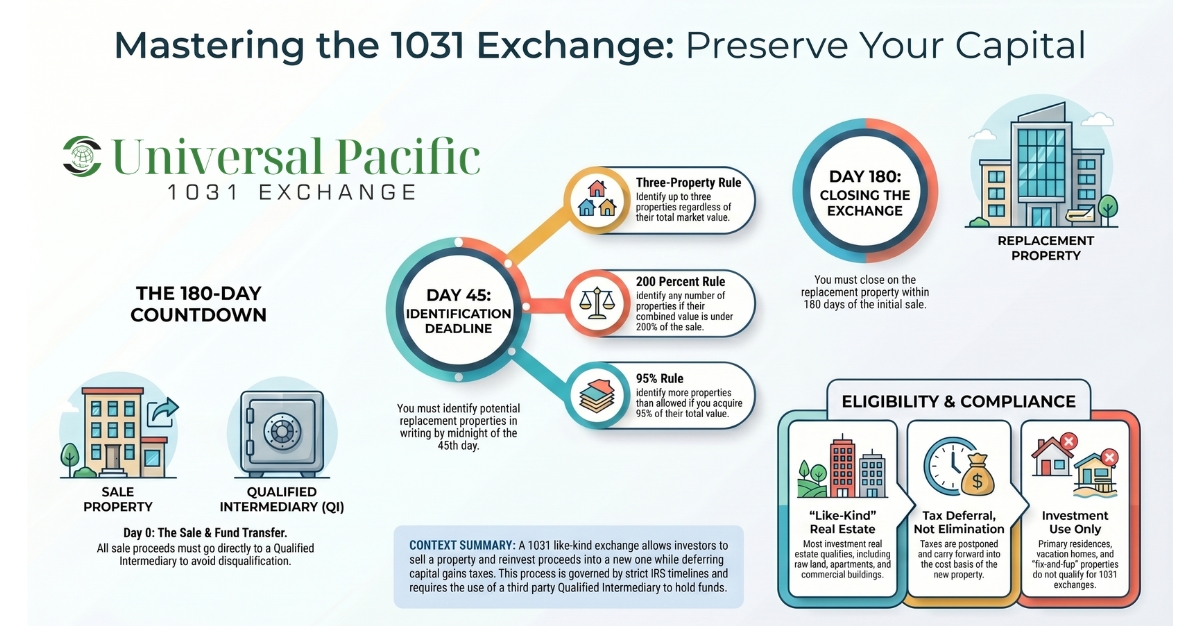

The most common structure is the delayed exchange, and it follows a clear sequence.

- The investor sells the relinquished property, and the proceeds go directly to a qualified intermediary rather than to the investor.

- Within 45 days of that sale, the investor identifies potential replacement properties in writing, signed and delivered to the qualified intermediary.

- Within 180 days of the sale, the investor must close on one or more of the identified replacement properties, using the funds held by the intermediary.

The 45-day and 180-day windows run at the same time, not back to back. The 180-day clock starts on the day the old property sells, so identifying the property slowly eats into the time available to close. Both deadlines are firm. The IRS does not extend them even when the 45th or 180th day lands on a weekend or a federal holiday. There is one more limit worth knowing: the exchange must also be completed by the due date of the investor’s tax return for that year, including extensions, if that date comes before the 180th day.

A short timeline example makes this concrete. An investor sells a rental property on March 1. They have until April 15 to identify replacement properties in writing, and until August 28, the 180th day, to close on the purchase. If they wait until day 44 to identify property, they have given themselves only 136 days to negotiate, finance, and close, which is a tight window in most markets.

When identifying replacement properties, investors usually rely on one of three rules. The three-property rule allows the investor to identify up to three properties regardless of their value. The 200 percent rule allows the investor to identify more than three properties, as long as their combined fair market value does not exceed 200 percent of the relinquished property’s value. The 95% rule applies when an investor identifies replacement properties that exceed the IRS identification limits. To keep the exchange valid, the investor must acquire at least 95% of the total value of all identified properties.

Qualified Like-Kind Property Explained

The term “like-kind” is broader than most investors expect. The IRS defines like-kind property as property of the same nature or character, even if it differs in grade or quality. For real estate, this means almost any real property held for investment or business purposes can be exchanged for almost any other.

An investor can exchange raw land for an apartment building, a single-family rental for a share in a commercial property, or an industrial warehouse for a retail strip center. The properties do not have to be the same type, the same size, or in the same state. What matters is that both the relinquished property and the replacement property are held for productive use in a trade or business or for investment.

Some property does not qualify. A primary residence does not qualify, because it is not held for investment. A vacation home used mainly for personal enjoyment generally does not qualify. Property held primarily for sale, such as a developer’s inventory or a house bought to flip, does not qualify. Stocks, bonds, partnership interests, and other securities are excluded. And real property located in the United States is not like-kind to real property located outside the United States, so a domestic property cannot be exchanged for a foreign one.

Types of Exchanges

Most investors use a delayed exchange, but Section 1031 supports several structures. The right one depends on timing and on whether the investor needs to acquire the replacement property before selling the old one. The table below summarizes the four main types. Each is explained in more detail in the paragraphs that follow.

| Exchange type | How it works | Best suited for |

|---|---|---|

| Simultaneous | The relinquished and replacement properties close on the same day | Rare today; straightforward swaps |

| Delayed | The investor sells first, then buys within the 45- and 180-day windows | The most common structure for most investors |

| Reverse | The investor acquires the replacement property before selling the relinquished one | Investors who find the right property before the sale closes |

| Improvement | Exchange funds are used to build on or improve the replacement property | Investors whose target property needs construction to match the value |

A simultaneous exchange closes both transactions on the same day. It was the original form of the like-kind exchange, but it is uncommon now because coordinating two closings perfectly is difficult.

A delayed exchange is the structure described in the section above. The investor sells first and then has 45 days to identify and 180 days to close on the replacement property. This is what most people mean when they talk about a 1031 exchange. A reverse exchange flips the order. The investor acquires the replacement property before selling the relinquished one.

Because IRS rules do not allow an investor to hold title to both properties at once during an exchange, an exchange accommodation titleholder holds one of the properties temporarily. Reverse exchanges are more complex and more expensive, but they help investors who find the right replacement property before their sale is finalized.

An improvement exchange, sometimes called a construction or build-to-suit exchange, allows the investor to use exchange funds to make improvements to the replacement property. This is useful when the target property is worth less than the relinquished property, and the investor wants to put the difference toward construction rather than receiving it as a taxable boot.

Common Misconceptions

Several myths cause investors trouble. One is the belief that the properties have to be nearly identical. They do not. The “like-kind” standard for real estate is wide, and grade or quality does not matter.

Another is the idea that a 1031 exchange makes the gain tax-free. It does not. The exchange defers the tax, and the deferred amount carries forward into the replacement property.

A third is the assumption that the investor can hold the sale proceeds for a short time before reinvesting. They cannot. The moment the investor has access to the funds, the exchange is disqualified. This is the reason a qualified intermediary is not optional in a delayed exchange.

A fourth is the belief that any property the investor owns can be exchanged. A primary residence, a fix-and-flip, and a foreign property all fall outside Section 1031.

Step-By-Step Guide to Reporting a Like-Kind Exchange

The exchange process doesn’t end after the replacement property has been sold. The transaction must also be reported correctly to avoid complications. Below is a step-by-step process for reporting a 1031 exchange.

Step 1: IRS Form 8824

Every 1031 exchange must be reported to the IRS on Form 8824, Like-Kind Exchanges, filed with the investor’s federal income tax return for the year the relinquished property was transferred. Form 8824 asks for the description of the relinquished and replacement properties, the dates the relinquished property was sold, and the replacement property was identified and received.

It also asks for the financial details used to calculate realized gain, recognized gain, any boot, and the basis of the new property. The recognized gain is the portion, if any, that is taxable in the current year, usually because the investor received boot.

The deferred gain reduces the cost basis of the replacement property, which is why accurate figures on this form matter for years to come. Because the calculations involve adjusted basis, depreciation, and boot, most investors complete Form 8824 with the help of a tax professional. Errors on this form are a common reason exchanges draw IRS attention.

Step 2: Record keeping and documentation

A 1031 exchange creates a paper trail that an investor needs to keep for the life of the replacement property and beyond. Essential documents include the closing statements for both the relinquished and replacement properties, the written identification notice sent within the 45-day window, the exchange agreement with the qualified intermediary, and records of the intermediary’s handling of the funds.

Investors should also keep records that support the business or investment use of both properties, such as leases, rental income records, and tax returns showing the property as an investment. If the IRS questions whether a property was truly held for investment, this documentation is the answer. Thorough record keeping is not just good practice. It is the difference between a clean exchange and a disqualified one if the return is ever examined.

Step 3: Potential challenges and solutions

A few problems often come up. Missing the 45-day identification deadline is the most common, and there is no fix once it passes, so the solution is to begin searching for replacement property before the relinquished property even closes. Receiving boot unexpectedly is another, often because of mortgage differences between the two properties, and careful planning of the debt on each side prevents it.

Depreciation recapture catches some investors by surprise, because the depreciation taken on the relinquished property carries forward and affects the tax owed when the chain of exchanges finally ends. Choosing the wrong qualified intermediary is a quieter risk. The QI holds the investor’s money, sometimes for months, and the industry is lightly regulated.

An intermediary with proper insurance, segregated accounts, and a documented compliance process protects the investor in a way that a bargain provider may not. This is where working with an experienced firm changes the outcome. A knowledgeable, qualified intermediary keeps the deadlines visible, structures the transaction to avoid accidental boot, and documents every step so the exchange holds up under review.

Why choose Universal Pacific

Universal Pacific 1031 Exchange is a qualified intermediary firm with more than 35+ years of CPA-supervised 1031 exchange experience overseeing 1031 tax-deferred exchanges. Over that time, the firm has handled exchanges across every real estate asset class, from multifamily portfolios and land development to industrial and retail transactions.

What sets a qualified intermediary apart is not marketing; it is the safeguards behind the money it holds. Universal Pacific keeps client funds in segregated accounts, carries $2 million in errors and omissions insurance, and uses multi-layered authorization controls on every transaction. Compliance work is handled in-house rather than outsourced, and every exchange is reviewed and documented by licensed tax professionals.

Universal Pacific provides end-to-end support on 1031 exchanges. That includes holding the sale proceeds as the qualified intermediary, preparing the exchange documentation, tracking the 45-day and 180-day deadlines, and coordinating with the investor’s own attorney, accountant, and real estate agents through closing.

The firm works on the full range of exchange structures, including straightforward delayed exchanges and the more demanding reverse and improvement exchanges. For investors moving multiple properties at once or working against a tight closing schedule, that experience with complex, deadline-driven transactions matters.

It is worth being clear about roles. A qualified intermediary handles and documents the exchange. It does not replace the investor’s own tax advisor or attorney. Universal Pacific works alongside those professionals so that the exchange itself is structured and recorded correctly.

Engage a Qualified Intermediary Today

A 1031 like-kind exchange is one of the most effective tools available to real estate investors who want to preserve equity and keep building their portfolios. The strategy works only when the IRS rules are followed exactly, from the 45-day and 180-day deadlines to the proper use of a qualified intermediary and the accurate reporting on Form 8824.

Used well, an exchange defers capital gains taxes and lets an investor move into stronger assets without losing momentum to a tax bill. Because the rules are strict and the cost of a mistake is the full tax liability, every investor should speak with a qualified intermediary and a tax professional before starting an exchange.

If you are considering a 1031 exchange, Universal Pacific 1031 Exchange can guide you through the process and help you keep your transaction compliant from the first day to the last. To learn more or to begin a transaction, visit Universal Pacific’s start an Exchange page or call the firm at (424) 469-8111. For the official rules, the Internal Revenue Service publishes guidance on like-kind exchanges and the Instructions for Form 8824 at irs.gov.

Frequently asked questions

Below are answers to common questions about a 1031 like-kind exchange.

What Is a 1031 Like-kind Exchange?

A 1031 like-kind exchange is a tax-deferred transaction under Section 1031 of the Internal Revenue Code. It allows an investor to sell an investment or business property and reinvest the proceeds into another qualifying property without paying capital gains taxes at the time of the sale. The tax is deferred, not eliminated, and carries forward into the replacement property.

How Does a 1031 Like-kind Exchange Benefit Investors?

The main benefit is that an investor keeps their full equity invested instead of losing a portion to capital gains taxes and depreciation recapture at each sale. That larger pool of capital can be used to acquire a more valuable property, diversify across markets, consolidate holdings, or improve cash flow. Over time, repeated exchanges can also support an estate planning strategy.

How Does a 1031 Like-kind Exchange Work?

In the most common structure, the delayed exchange, the investor sells the relinquished property and the proceeds go to a qualified intermediary. The investor then has 45 days to identify replacement properties in writing and 180 days from the sale to close on the purchase. The investor cannot touch the proceeds at any point, or the exchange is disqualified.

What Are the Rules for a 1031 Like-kind Exchange?

Both properties must be held for business or investment use, the exchange must use a qualified intermediary, the 45-day identification and 180-day completion deadlines must be met, and the exchange must be reported on IRS Form 8824. Since 2018, only real property qualifies, and U.S. property cannot be exchanged for foreign property.

What Types of Properties Qualify for a 1031 Like-kind Exchange?

Real property held for investment or business use qualifies, including rental homes, apartment buildings, commercial buildings, industrial property, retail centers, and raw land held for investment. Primary residences, vacation homes used mainly for personal purposes, fix-and-flip property held for resale, and securities such as stocks and partnership interests do not qualify.

Are there Time Restrictions for Completing a 1031 Exchange?

Yes, and they are strict. The investor must identify potential replacement properties within 45 days of selling the relinquished property and must close on the replacement property within 180 days of that sale. The deadlines run at the same time, cannot be extended for weekends or holidays, and are also capped by the due date of the investor’s tax return, including extensions, if that date is earlier.

How Can Universal Pacific Assist with a 1031 Exchange?

Universal Pacific 1031 Exchange is the qualified intermediary on the exchange. It holds the sale proceeds, prepares the exchange documentation, tracks the IRS deadlines, and coordinates with the investor’s attorney, accountant, and agents through closing. With more than 35+ years of CPA-supervised 1031 exchange experience and a focus on complex reverse and improvement exchanges, the firm helps investors keep their transactions compliant and properly documented.

Disclaimer: This article is for general educational purposes and does not constitute tax or legal advice. A qualified intermediary handles and documents a 1031 exchange but does not provide tax or legal advice. IRS rules change, and every transaction depends on its own facts. Consult a licensed tax professional and a qualified intermediary before starting an exchange.

Editorial Policy

All articles are reviewed for accuracy by licensed tax professionals and sourced from official government publications. Read our Editorial Policy →

About The Author

![]() Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.

Michael Bergman is a California licensed CPA and Real Estate Broker with over 35+ years of CPA-supervised 1031 exchange experience in commercial real estate. Specializing in 1031 tax-deferred exchanges and financial oversight, his expertise covers complex real estate transactions. Michael’s unique blend of financial acumen and real estate knowledge positions him as a trusted advisor in the industry, offering sound advice and strategic insights for successful property management and investment.